Go back to Blog

Jennifer Edidiong

Marketing

7 min read

Share to

Continuous Monitoring vs One-Time Checks: What African Fintechs Need in 2026

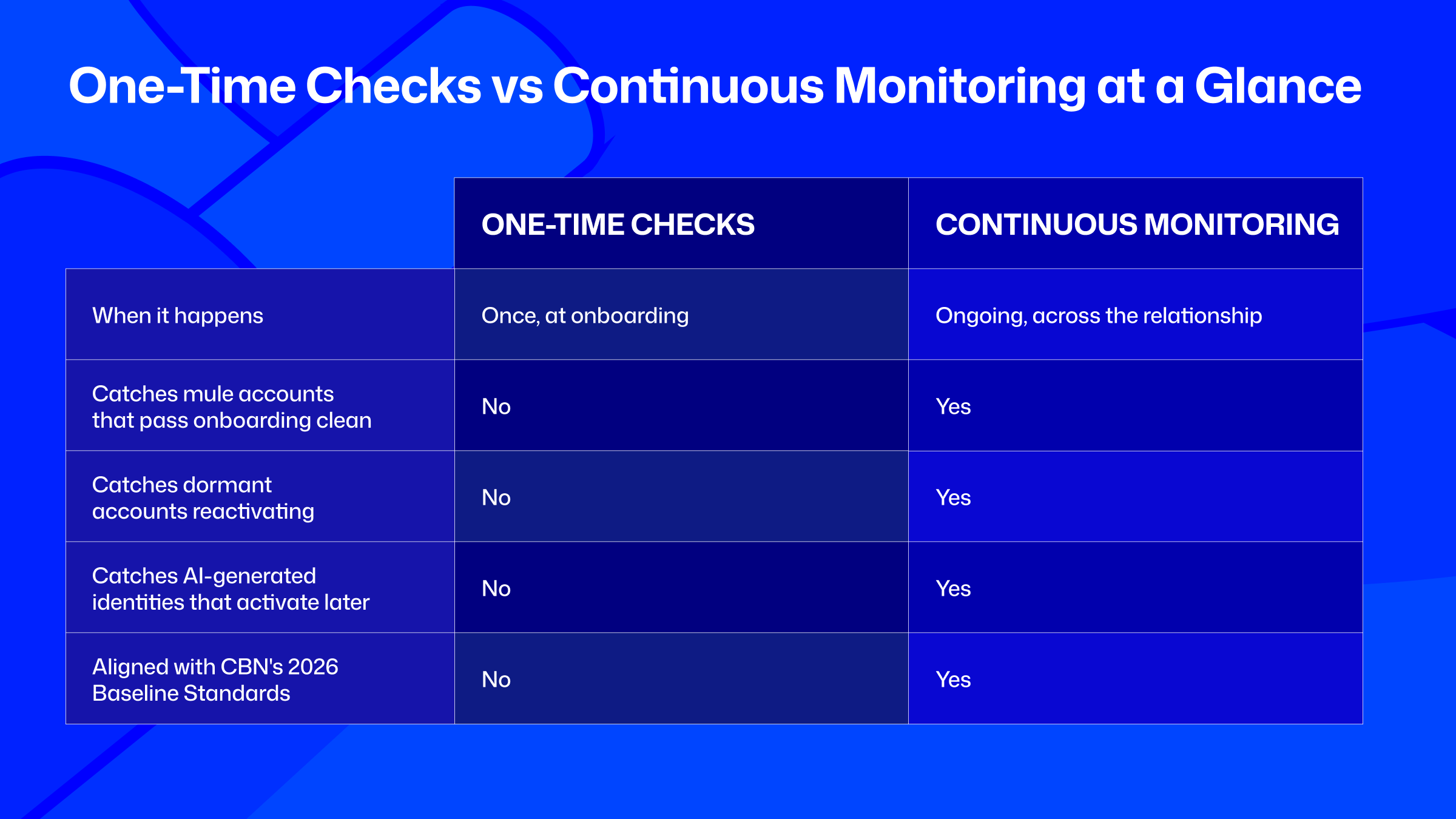

A one-time check confirms who a customer was on the day they signed up. Continuous monitoring tracks how that customer's behaviour, risk profile, and transaction patterns change over time. The distinction matters because many of the fraud and compliance risks institutions face today do not exist at onboarding; they emerge later.

Many African fintechs still rely primarily on the first approach, treating identity verification as a single milestone rather than an ongoing process. The challenge is that an account can appear completely legitimate when it is opened and only become high risk months later, leaving institutions with little visibility into what changed after onboarding.

This article explains the difference between continuous monitoring and one-time checks and what to prioritise when moving towards continuous monitoring.

What One-Time Checks Cover

A one-time check is exactly what it sounds like: identity verification performed once, usually during onboarding. It confirms your customer's identity before the account is opened.

These checks typically include:

- What it actually confirms: A one-time check typically includes government ID verification and a liveness or selfie match. Depending on your compliance process, it may also include sanctions or PEP screening. Together, these checks confirm the customer's identity before the account goes live.

- Why it was sufficient: When one-time checks became the standard, onboarding volumes were lower, and fraud was less coordinated than it is today. A strong check at onboarding was often enough to identify the risks that existed at that point. It provided a solid foundation for customer verification.

- What it implicitly assumes: Once you complete a one-time check, you are working from the identity and risk profile established at onboarding. The process is not designed to tell you when that risk changes later.

What Continuous Monitoring Actually Involves

Continuous monitoring does not replace the one-time check. It extends risk assessment across the customer relationship instead of stopping once onboarding is complete.

Continuous monitoring covers three main areas:

- Ongoing Behavioural Signals: Track behavioural signals such as device changes, login patterns, and location shifts over time. Looking at these changes together gives you a clearer picture of how customer activity evolves after onboarding.

- Transaction Pattern Analysis: Continuous monitoring compares transactions against each customer's established behaviour instead of relying only on static rules. For example, a sudden increase in transfer activity or a change in payment patterns can stand out, even when no individual transaction appears unusual on its own.

- Periodic and Event-Triggered Re-Verification: Revisit identity confidence and risk ratings instead of leaving them unchanged after onboarding. Re-verification can happen on a schedule or after events such as a dormant account becoming active again, a significant change in transaction behaviour, or a login from a new device or location.

This gives you visibility beyond onboarding, where one-time checks were never designed to operate and where many modern fraud patterns emerge.

Related: Transaction screening vs transaction monitoring for African fintechs

Why One-Time Checks Alone Aren't Sufficient

One-time checks confirm who your customer is at onboarding, but they cannot account for how risk changes afterward. That is why they are no longer enough on their own.

These are the specific scenarios where one-time checks fall short:

- Mule Accounts Pass Onboarding: The account holder is real, and the identity documents are genuine. The account may appear low risk during its first weeks or months. The fraud begins only after the account has already passed the one-time check.

- The Risk Emerges After Onboarding: One path is where an account holder later hands over their credentials through a scam or coercion. Another is the reactivation of an older account that has been inactive for a long period. Neither situation is visible during a one-time check because both happen after onboarding.

- AI-Generated Identities Extend the Same Gap: An AI-generated identity can pass document and liveness checks during onboarding. It may remain inactive or build a limited transaction history before becoming active later. If monitoring ends after onboarding, that change can go unnoticed.

- Regulation Now Reflects the Same Reality: On 10 March 2026, the CBN issued a circular introducing the Baseline Standards for Automated AML/CFT/CPF solutions. The standards move institutions away from periodic checks toward automated, continuous monitoring. They also require early warning systems for mule accounts and set phased compliance timelines.

One-time checks confirm who your customer is at onboarding, while continuous monitoring helps you understand how that risk changes over time.

What to Prioritise First When Moving Toward Continuous Monitoring

Moving from one-time checks to continuous monitoring does not have to happen all at once. Start with the areas that reduce risk most effectively.

Here's where to begin:

1. Start with Transaction Baselines

Start by establishing what normal transaction behaviour looks like for each customer after onboarding. This helps you identify meaningful changes over time instead of relying only on static rules. It also addresses the biggest gap, which emerges after the account is already active.

2. Prioritise Mule Account Detection

Make mule account detection an early priority. The CBN's 2026 Baseline Standards require institutions to implement early warning capabilities for mule accounts. Starting here helps you address a risk area that regulators now expect institutions to monitor continuously.

3. Connect Identity and Transaction Data

Assess transaction activity alongside verified identity data and onboarding risk information. This gives you the context needed to investigate alerts more effectively. It also reduces the manual effort required to piece information together from separate systems.

4. Build Toward the CBN Timeline

Treat continuous monitoring as a phased programme rather than a one-time project. The CBN requires implementation roadmaps by June 2026, with phased compliance extending into 2027 or 2028, depending on institution type. Starting early gives you more time to build the capabilities the standards require.

These priorities help you move from one-time verification to continuous risk monitoring, which is exactly the approach Dojah's Profiled Risk is built to support.

How Dojah's Profiled Risk Supports This Shift

Profiled Risk is built to close the monitoring gap by connecting identity verification with ongoing behavioural and transaction risk monitoring across the customer lifecycle.

- Risk profiles that update as behaviour changes. Profiled Risk tracks behavioural drift, dormant account reactivation, and transaction patterns that no longer match a customer's established profile, so emerging risks surface before they become larger investigations.

- Identity and transaction data in one place. Every risk signal is evaluated alongside the customer's verified identity, transaction history, and risk profile. Your team gets the full picture without switching between systems or pulling records manually.

- AI-powered risk intelligence and case management. An AI-powered dashboard brings risk insights into one view, while built-in case management helps fraud and compliance teams review alerts, collaborate on investigations, and maintain audit-ready records.

Profiled Risk helps you move from one-time verification to continuous monitoring by bringing identity, behaviour, and transaction risk together in one place.

Ready to make that shift? See how Profiled Risk helps your fintech stay ahead of risk after onboarding

Frequently Asked Questions on Continuous Monitoring vs One-Time Checks: What African Fintechs Need in 2026

1. What is the difference between continuous monitoring and one-time checks?

A one-time check verifies your customer's identity during onboarding. Continuous monitoring extends that assessment by tracking changes in behaviour, transaction patterns, and risk throughout the customer relationship.

2. Why are one-time checks no longer enough?

One-time checks confirm who your customer is at onboarding, but they cannot detect risks that emerge later, like mule accounts, dormant account reactivation, or AI-generated identities that only become active months after signup. That is why one-time verification alone is no longer enough.

3. How can fintechs implement continuous monitoring?

Start with transaction baselines, establishing what normal behaviour looks like for each customer after onboarding. Then connect identity and transaction data, so alerts carry the context your team needs to investigate them properly. Build from there toward full continuous monitoring over time.

Start using Dojah for all your business needs