Go back to Blog

Jennifer Edidiong

Marketing

11 min read

Share to

How to Detect Smurfing Transactions: AML Tips for Fintechs

Imagine this: One day, you notice small, repeated transactions flowing through your fintech platform. The amounts seem harmless, the senders look legitimate, and everything appears routine at first glance.

It might not seem alarming at first, but behind those deposits could lie something more serious: a coordinated scheme designed to bypass your platform’s monitoring system. According to Investopedia, this hidden activity, known as smurfing, has cost banks and fintechs millions of dollars in financial losses and compliance penalties worldwide.

As a founder, compliance lead, or risk officer, understanding how these patterns form and knowing what to look for is key to protecting your business.

In this article, you’ll learn:

- What smurfing is and how it works

- Why it’s often missed or hard to detect

- Practical steps to identify smurfing in your fintech or banking platform

By the end, you’ll know how to recognize hidden transaction behaviors that signal money laundering and keep your platform protected against emerging fraud schemes.

What Is Smurfing in AML?

Smurfing, also called structuring, is when large sums of money are broken into smaller, seemingly normal transactions to avoid AML reporting thresholds. This makes it hard for banks or fintechs to spot suspicious activity because each deposit or transfer appears routine on its own.

For example, a Nigerian customer on your bank or fintech platform might deposit ₦900,000 several times instead of a single ₦5 million payment to stay under the ₦1 million CBN reporting limit. To your system, each transaction seems ordinary, but combined, they can hide significant illicit activity.

Smurfing enables money laundering, terrorist financing, and regulatory breaches. Although illegal under FATF and CBN AML/CFT rules, it is difficult to trace because the activity is spread across multiple small transactions.

Related: AML software for banks & fintechs

Common Patterns of Smurfing Transactions in Practice (Scenario-Based)

To break this down practically, let’s follow Rachel, a returning user on LumenPay (a fictional fintech), and see how smurfing can unfold step by step.

Step 1: Multiple small deposits over short periods

Rachel deposits ₦900,000 each day for five days instead of one ₦4.5 million payment. Each deposit sits just under the ₦1 million CBN reporting threshold, so on the surface it looks ordinary. Together these daily deposits form a larger sum that hides in plain sight, making it harder for your system to detect suspicious activity. From the backend, it may appear as routine deposits with nothing triggering immediate concern.

Step 2: Layering through multiple accounts or digital wallets

Next, Rachel moves portions of the funds between accounts she controls on LumenPay and a couple of external wallets. Each transfer seems legitimate on its own, but the repeated bouncing across accounts creates layers that obscure the original source. Without account and device linking analytics, these movements remain invisible, appearing as ordinary inter-account activity.

Step 3: Using mule accounts to fragment funds

Rachel then uses mule accounts, third-party profiles that receive and forward portions of the money. Each mule may look like a genuine user with normal activity, and Rachel even uses a few friends as additional mules. This fragmentation spreads the risk across multiple accounts and makes manual detection far more difficult.

Step 4: Cross-border smurfing via remittances or crypto

At this stage Rachel converts some funds to crypto or sends them through remittances to foreign accounts, moving money from LumenPay to other platforms or exchanges. These transfers blend with legitimate activity and mask the flow. Once funds cross platforms or borders, visibility drops and tracing becomes harder

Step 5: Ripple effect — small flows creating a large exit

Over time Rachel’s deposits, layering, mule fragmentation, and cross-border moves culminate in a single outflow of about ₦4 million. Each ripple looked minor on its own, but together they enabled a major transfer. Detecting this cumulative effect early through frequency analysis and account linking is key to stopping the exit before it occurs.

See: Processes of AML transaction monitoring rules

Why Smurfing Is Difficult to Detect in AML Monitoring

In most cases, smurfing isn’t easily detectable and can blend into everyday financial activity. Here’s why:

1. Criminals adapt patterns to look normal

Fraudsters continually adjust their behavior to evade detection. They may alter transaction times, amounts, or destinations just enough to appear legitimate. These subtle variations make it difficult for detection systems to identify consistent suspicious trends.

2. Traditional rule-based systems often miss subtle patterns

Many AML tools still rely on static thresholds, flagging only when a transaction exceeds a fixed amount. Smurfing exploits this by splitting funds into multiple smaller transfers. Without advanced analytics or machine learning, these scattered movements appear harmless in isolation.

3. Lack of visibility across accounts and institutions

Smurfing networks often move money across multiple banks, fintechs, or digital wallets. When data is siloed across different systems, it becomes nearly impossible to detect related activity or trace how a single user or group structures funds across platforms.

4. Limited contextual and behavioral monitoring

Most compliance systems track numbers, not context. They can’t easily detect when a user’s behavior suddenly changes; for example, a student account making frequent deposits or multiple users sending money to one beneficiary. Without behavioral profiling, these shifts easily look like regular activity.

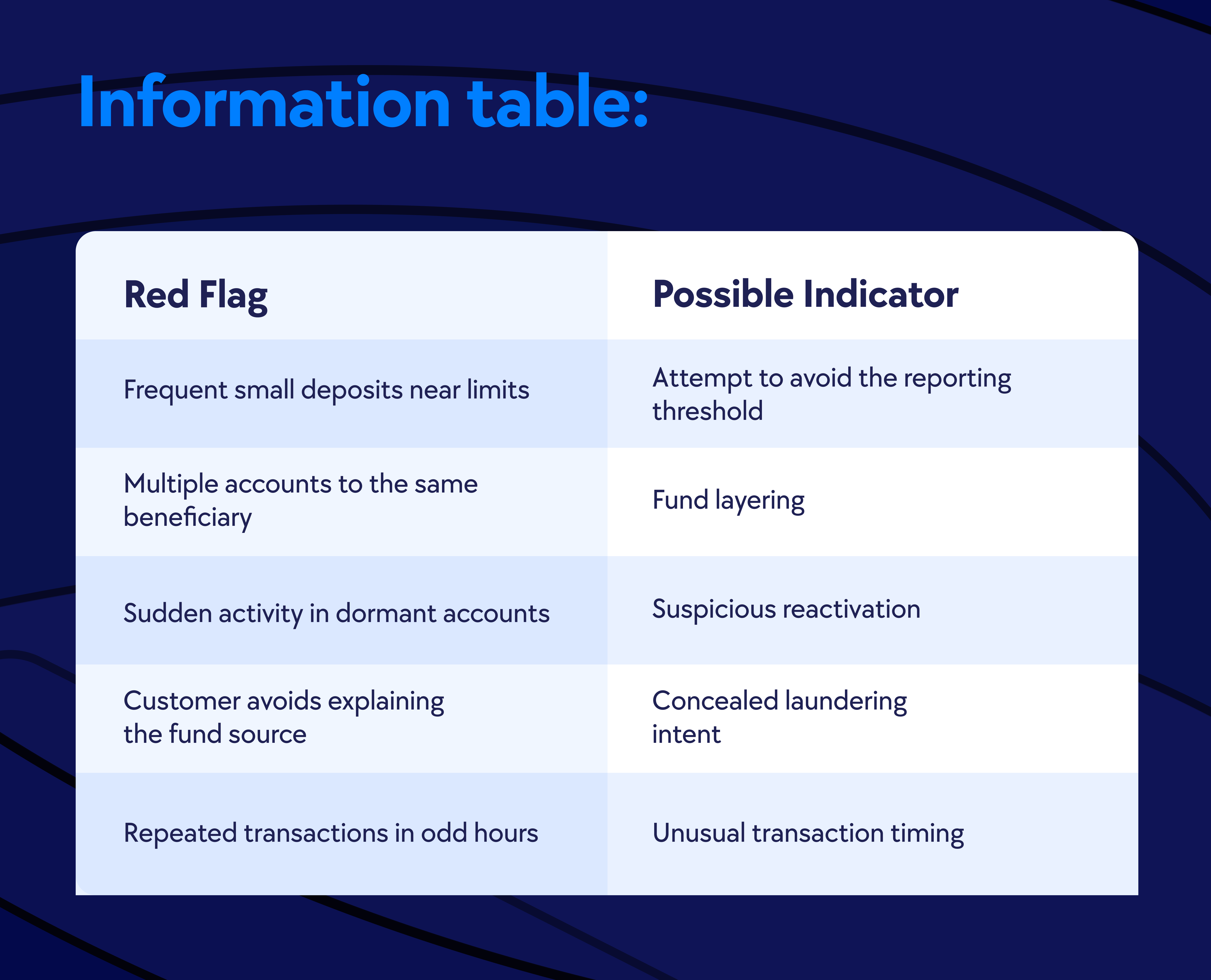

Common Red Flags in Detecting Smurfing

Despite these challenges, certain behaviors can still serve as early warning signs of smurfing, such as:

- Frequent small deposits just below reporting limits: users may repeatedly send ₦950,000 or $9,000 to stay under AML thresholds.

- Sudden transaction surges in previously inactive accounts: dormant users suddenly start moving large sums or making daily deposits.

- Multiple accounts sending or receiving to the same destination: often a sign of mule accounts funneling funds to a central wallet.

- Customers who cannot clearly explain their source of funds: vague justifications or inconsistent statements during KYC or follow-up reviews.

Repetitive transactions across odd hours or high-risk regions: activity patterns that don’t align with typical customer behavior or location.

Also see: KYC vs KYB for AML Compliance

How to Detect Smurfing Transactions: Practical Steps Using Dojah’s EasyDetect

Despite the challenges in detecting smurfing, you can prevent it with the right system. Let’s go back to the earlier story of Lumenpay, where Rachel tried to move funds in small batches. Here’s how you can use Dojah’s unified fraud solution, EasyDetect to identify and stop smurfing in this scenario:

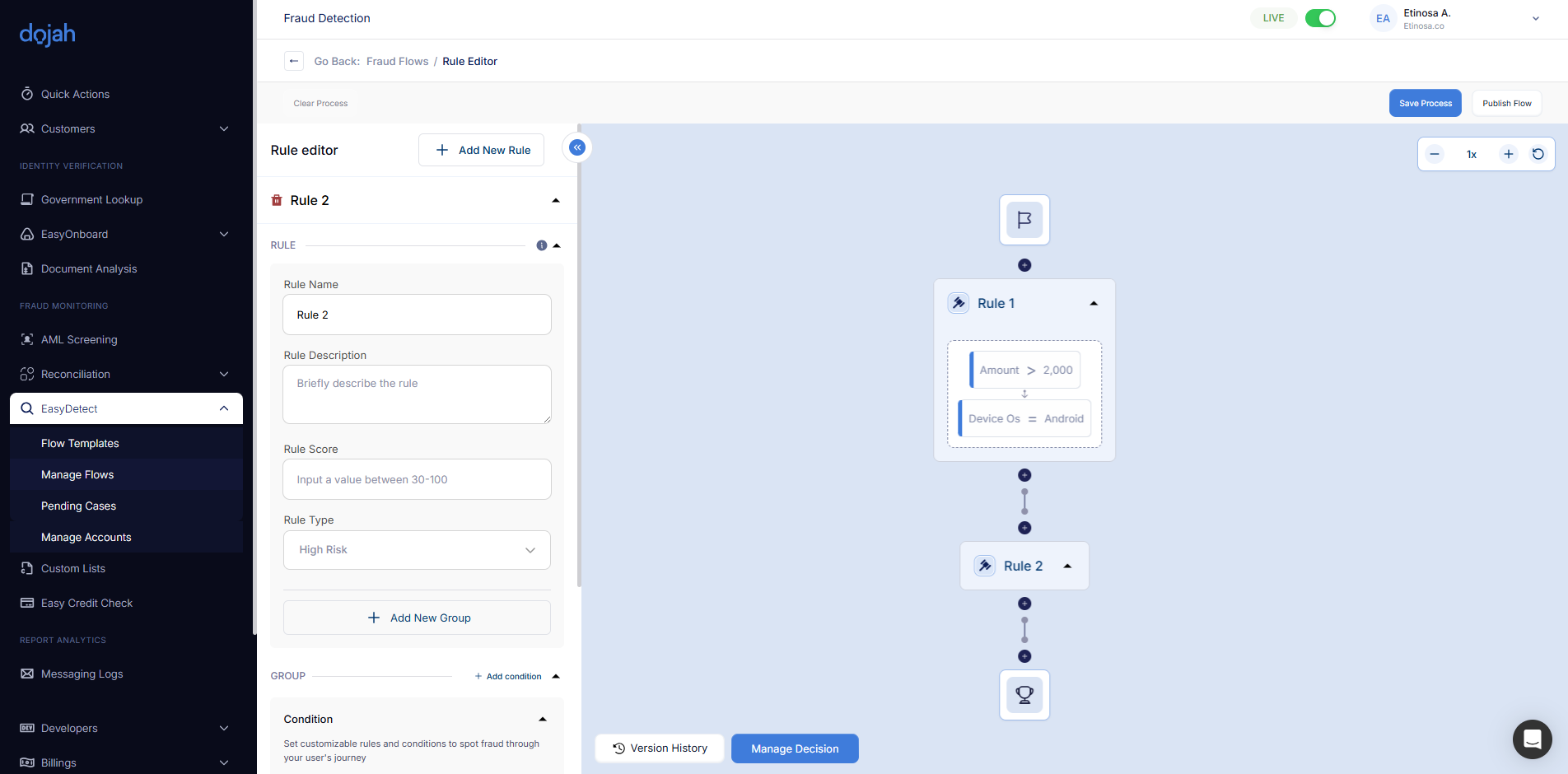

1. Set transaction threshold alerts

Traditional systems only flag transfers above a fixed amount. EasyDetect lets you set flexible thresholds that detect repeated deposits near reporting limits. If Rachel sends ₦950,000 five times in a day, the system links those deposits and triggers a smart alert early. You can easily adjust thresholds to match your compliance needs or regional limits.

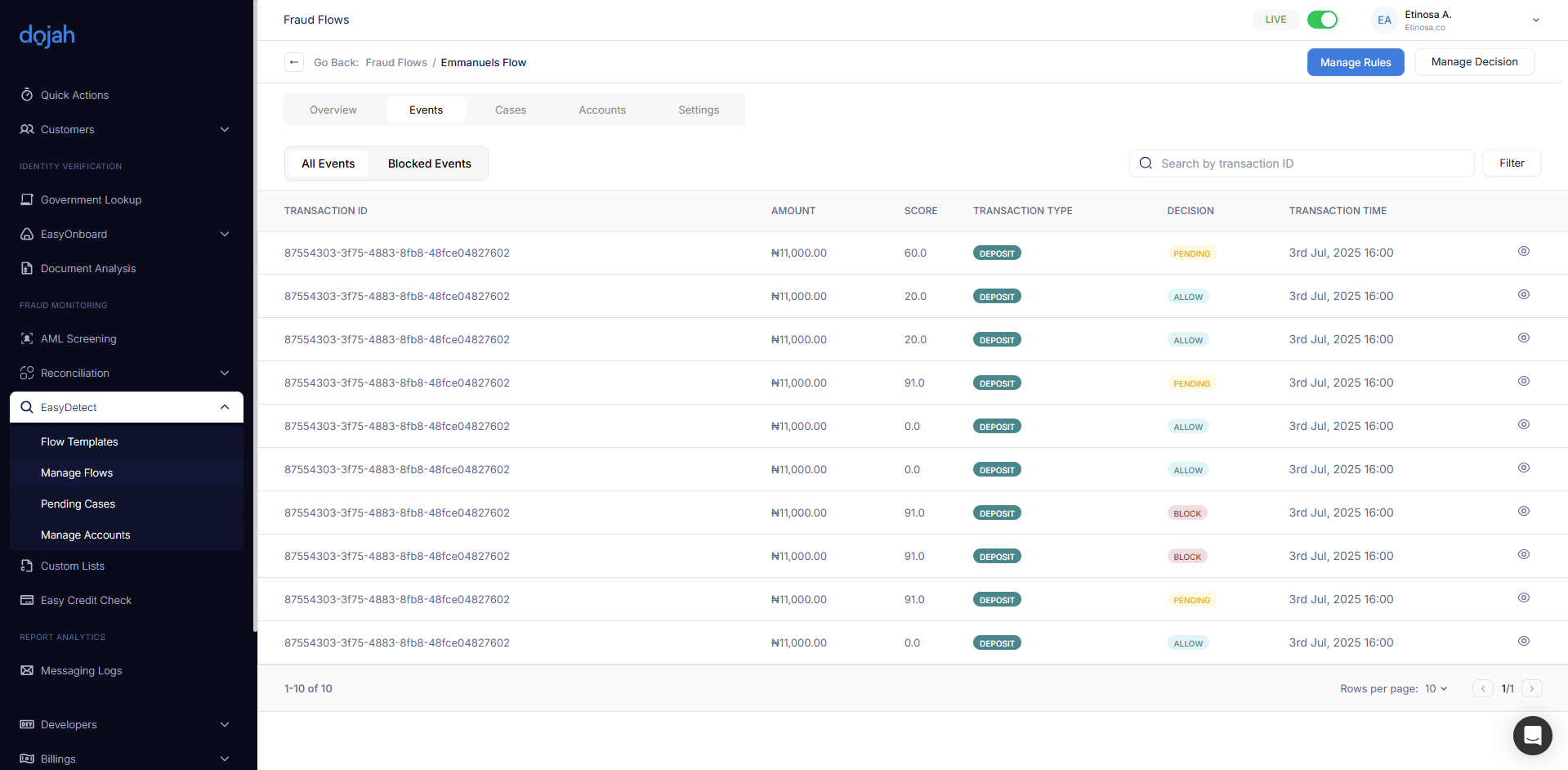

2. Monitor transaction frequency and velocity

Smurfing happens fast. EasyDetect’s KYT analytics track how often and how quickly money moves, spotting sudden spikes that break normal patterns. Rachel’s repeated back-to-back deposits within an hour would instantly stand out as abnormal and be flagged for review.

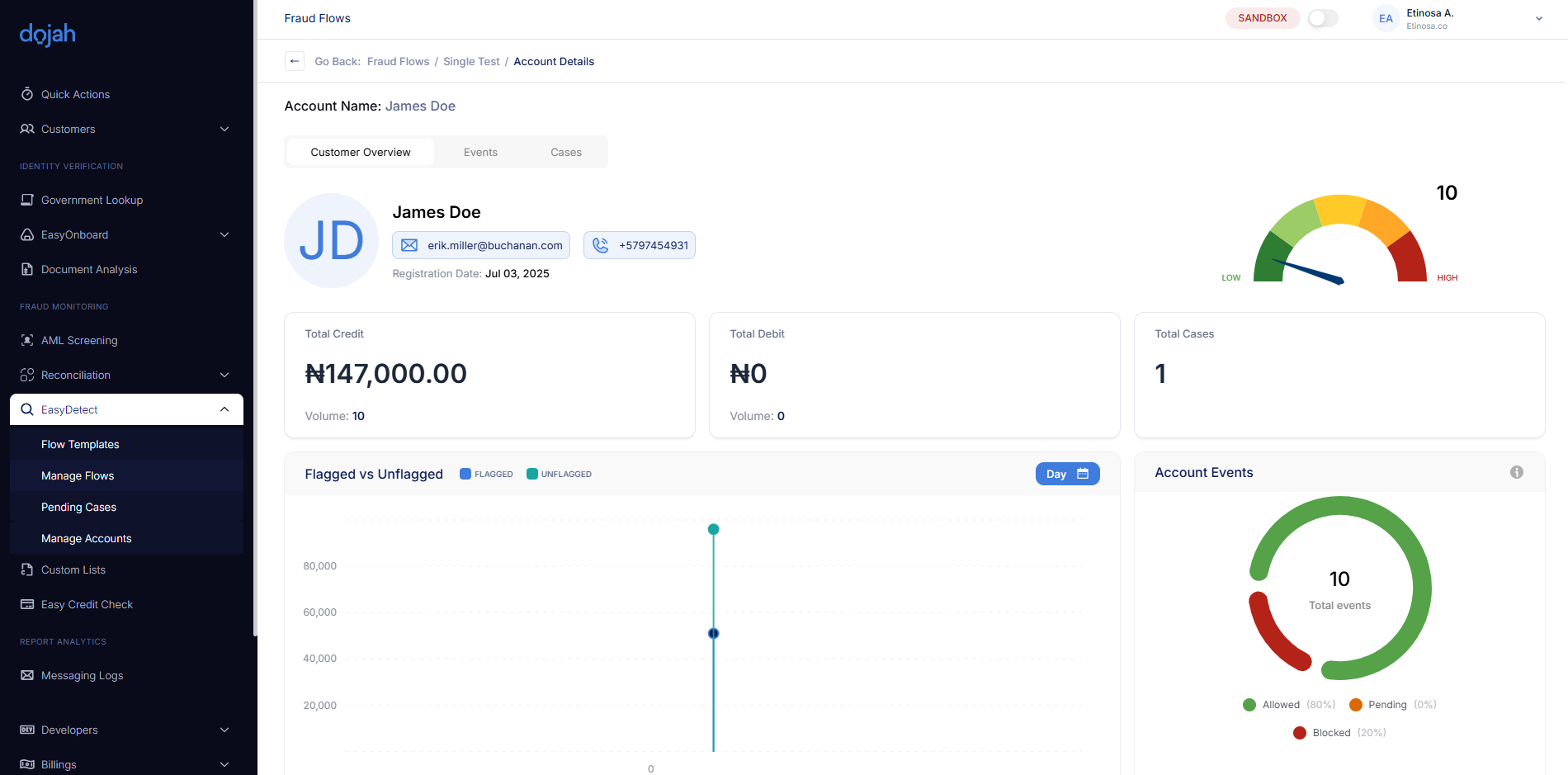

3. Use behavioral profiling

Most tools track raw data, not behavior. EasyDetect learns each customer’s usual activity and flags anything that deviates. When a once-inactive account suddenly becomes very active, it’s highlighted for review. Rachel’s quiet account suddenly making daily deposits would trigger a behavioral alert with context, helping your team act faster and more accurately.

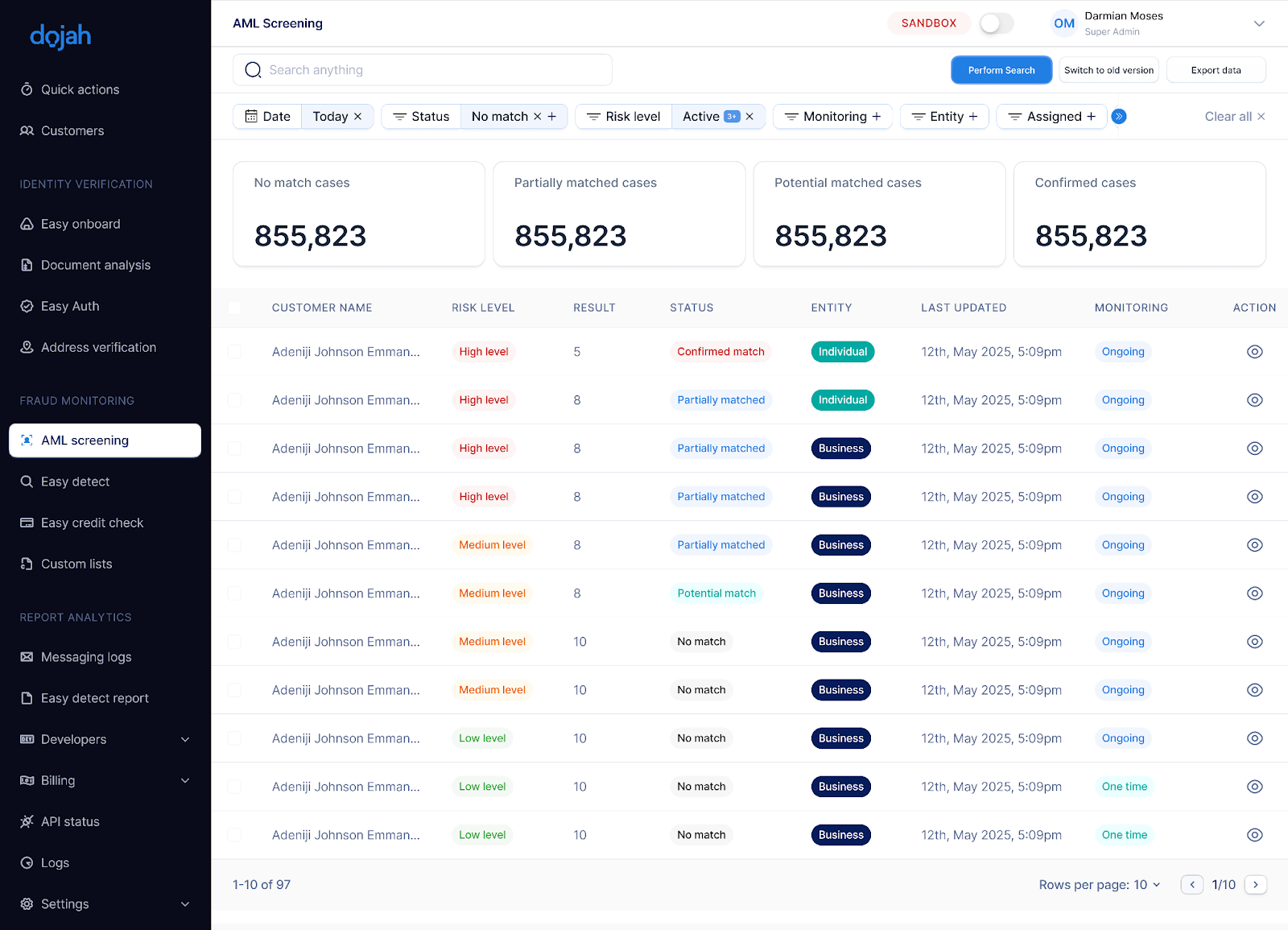

4. Link related accounts and devices

Smurfing networks often use several accounts, wallets, or platforms. EasyDetect connects transactions through shared devices, IPs, or user details to reveal hidden relationships. If Rachel and her associates used different accounts to fund the same wallet, the system would flag it as a connected network.

5. Apply AI and machine learning pattern recognition

Fraudsters constantly change their methods. EasyDetect’s AI analyzes transaction histories to uncover subtle structuring patterns. Even if Rachel alters her timing or amount, the system detects the shift and updates in real time, staying ahead of evolving tactics.

6. Continuous monitoring beyond onboarding

KYC only covers the start of a customer’s journey, but smurfing often begins later. EasyDetect keeps monitoring transactions in real time, alerting your team when behavior changes. Even after Rachel passed verification, her later attempts to layer funds would still be caught.

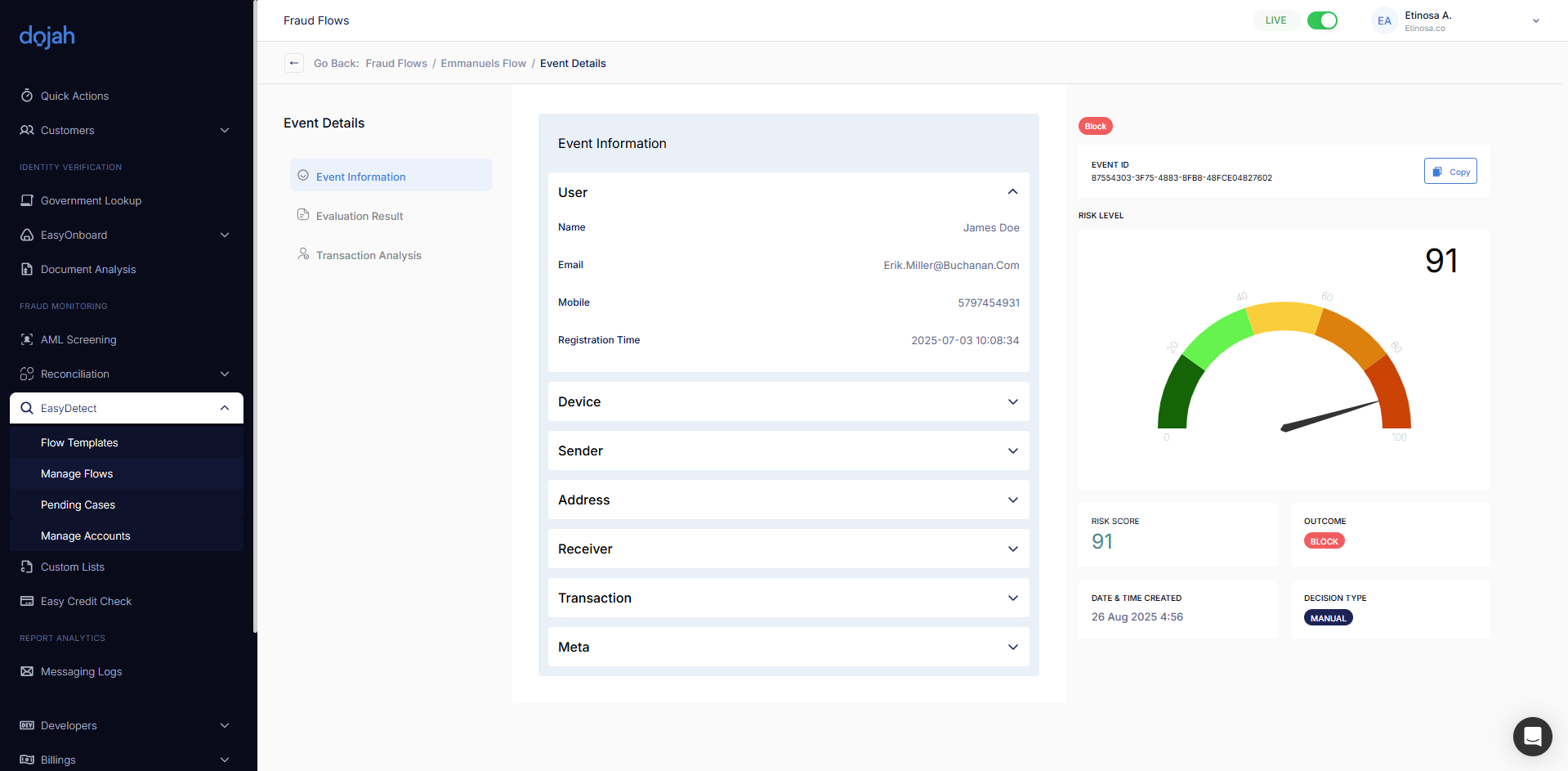

7. Automate suspicious activity reporting

When suspicious activity appears, EasyDetect automates the next step. It compiles transaction details, timestamps, and risk insights into ready Suspicious Activity Reports (SARs). When Rachel’s repeated deposits were detected, the system logged the pattern automatically, saving hours of manual reporting and helping the team escalate faster.

Following these steps, just like LumenPay, your fintech or bank can move beyond reactive alerts to proactive fraud prevention and detect suspicious behavior before it turns into a costly compliance breach.

Safeguard Your Fintech Against Smurfing Fraud

For fintechs and banks, missing early signs of smurfing can lead to serious regulatory penalties, revenue loss, and damaged trust. The longer it goes unnoticed, the harder it becomes to trace and contain. That’s why early detection is not just a compliance requirement; it’s a business safeguard.

With Dojah’s EasyDetect, you can identify unusual activity in real time, link related transactions across accounts, and automate alerts before risks escalate. The system gives your compliance team the visibility and speed to act early and keep your platform secure.

Trusted by over 500 businesses across Africa, Dojah helps fintechs, payment platforms, and digital banks stay proactive and prevent fraud before it happens.

Book a demo today to see how EasyDetect strengthens your AML defense and keeps your platform one step ahead.

FAQs on Smurfing Transactions

1. How does smurfing affect my fintech or bank?

Smurfing can expose your platform to money laundering risks, regulatory penalties, and reputational damage if undetected. It also increases compliance workload as auditors investigate unusual transaction trails.

2. Why is smurfing difficult to detect?

Because each transaction looks normal in isolation. Criminals spread deposits across accounts and vary the timing or amount, making it hard for rule-based AML systems to flag patterns.

3. Can smurfing occur through crypto or digital assets?

Yes. Launderers often convert funds into crypto or stablecoins to fragment and move money faster across borders, bypassing traditional AML limits.

4. What are early signs of smurfing I should look out for?

Watch for repeated deposits just below reporting thresholds, sudden activity in dormant accounts, or multiple users sending money to the same wallet or account.

5. How can I stop smurfing early?

Use transaction monitoring tools that track frequency, behavior, and account connections — not just amounts. Real-time KYT analytics like Dojah’s EasyDetect help spot these hidden links before large sums exit your system.

6. Are there tools that detect smurfing automatically?

Yes. Modern AML solutions use AI and behavioral analytics to uncover suspicious transaction networks. Tools like EasyDetect go beyond rule-based alerts to detect, link, and report smurfing activity automatically.

Start using Dojah for all your business needs