Go back to Blog

Chioma Ugwa

Marketing

8 min read

Share to

Fake Account Detection in Africa: How to Block Fraudsters at Signup

Most fake accounts don’t break your KYC. They pass it.

Fake accounts continue to slip past KYC checks, even on platforms with strong identity verification. On the surface, IDs are valid, emails exist, and phone numbers check out. But behind the scenes, these accounts are already poised to exploit your system. Left unchecked, they can commit fraud and even erode trust across your user base.

In African fintech markets, this risk is amplified. It’s common to see multiple accounts tied to a single device, reused phone numbers across wallets, or coordinated signup attempts from the same network trying to bypass onboarding controls.

The core problem is simple: identity verification alone isn’t enough, especially given the limitations of KYC systems in detecting intent. KYC confirms who someone is, but it doesn’t reveal whether the account is genuine, automated, or part of a coordinated fraud ring.

To protect your platform, you need to look beyond the ID and focus on signals, behaviors, and patterns that reveal each signup’s true intent. This article breaks down how to detect these risk signals and prevent fake signups on your platform.

Why Fake Accounts Still Get Through KYC

Even thorough KYC systems can be bypassed because fraudsters have evolved. The accounts they create aren’t always fully fake; they’re engineered to pass standard checks. Two common approaches are synthetic identities and stolen identities:

Synthetic identities combine real and fake information to create accounts that look legitimate. For instance, a fraudster might take a real phone number, mix it with a fabricated name and ID, and open an account. Because KYC validates individual data points rather than the combination, these accounts often pass verification without triggering alarms. In markets like Nigeria, this can involve misuse of BVN or NIN-linked data, where real identifiers are combined with fabricated details to create accounts that pass verification but are controlled by fraudsters.

Stolen identities are another loophole. Fraudsters use real personal information, sometimes from leaks or previous breaches, to create accounts under someone else’s name. From the system’s perspective, the ID is valid, the email is active, and the phone number works, so KYC clears the account. Only when suspicious activity appears, like unusual transactions or device mismatches, often after onboarding, do these accounts reveal themselves through patterns associated with post-onboarding fraud.

In both cases, the insight is clear: KYC shows who the user claims to be, not whether the account is trustworthy. Platforms need additional signals and behavioral checks to expose fake signups before they impact the system.

The Different Types of Fake Accounts

Not all fake accounts are the same. Some are automated, some are carefully crafted to blend in, and others operate in coordinated groups. Understanding the main types helps teams spot patterns and prioritize detection efforts.

- Bots: Automated accounts created to perform actions at scale. They often register in batches and mimic normal behavior at first, exploiting referral programs, spamming systems, or inflating metrics. Fast activity, repeated actions, or identical behavior across accounts usually exposes them.

- Synthetic users: Accounts built by combining real and fake information to appear legitimate. Unlike bots, they act normally for weeks, sometimes for months, before executing fraud. Standard KYC often won’t catch them because they look human.

- Fraud rings: Coordinated groups of fake accounts controlled by one operator. They collaborate to bypass protections, move funds, or manipulate promotions. Detection requires spotting shared devices, repeated patterns, or similar behaviors across multiple accounts. Some of these fraud rings operate across regions in West Africa, coordinating account creation, transactions, and withdrawals across multiple platforms to avoid detection.

Signals That Reveal Fake Accounts

Detecting fake accounts requires looking beyond identity. Signals from devices, contact info, network, and user behavior reveal accounts that have passed KYC but aren’t legitimate.

- Device fingerprinting: Tracks hardware, browser, and network details. Multiple accounts from the same device or inconsistent fingerprints signal automation or account sharing.This is especially important in African markets where shared devices are common, for example, multiple users operating from a single smartphone. Detection systems need to distinguish between legitimate shared usage and coordinated fraud activity.

- Phone and email reputation: Measures trustworthiness based on history and prior use. Disposable emails, reused phone numbers, or contacts linked to past fraud indicate risky accounts.

- IP intelligence: Monitors the location, type, and behavior of network addresses. Multiple accounts from the same IP in a short period, or logins from unusual locations, suggest attempts to bypass restrictions or hide fraud.

- Behavioral inconsistencies: Compares user interactions to normal patterns. Rapid form submissions, unusual click sequences, or abnormal transactions often reveal fake accounts acting differently than legitimate users.

Combining Signals for Accurate Detection

Detecting fake accounts with a single signal rarely works. A single data point can be misleading, and focusing on a single metric often leads to false positives, frustrating real users. The most effective approach is layered detection, which combines multiple signals to provide a comprehensive view of account risk.

- Layered approach: Each signal—device, email/phone, IP, behavior—tells part of the story. When considered together, anomalies become clearer. For example, a disposable email alone might not trigger a block, but combined with a reused device and unusual login patterns, the risk is obvious. Layered detection improves accuracy and catches fraud that single checks would miss.

- Reducing false positives: While catching fake accounts is critical, overzealous detection can disrupt legitimate users. Combining signals helps balance security with user experience. Platforms can set thresholds where risk scores trigger further verification rather than outright blocking, ensuring the system is protective without being restrictive.

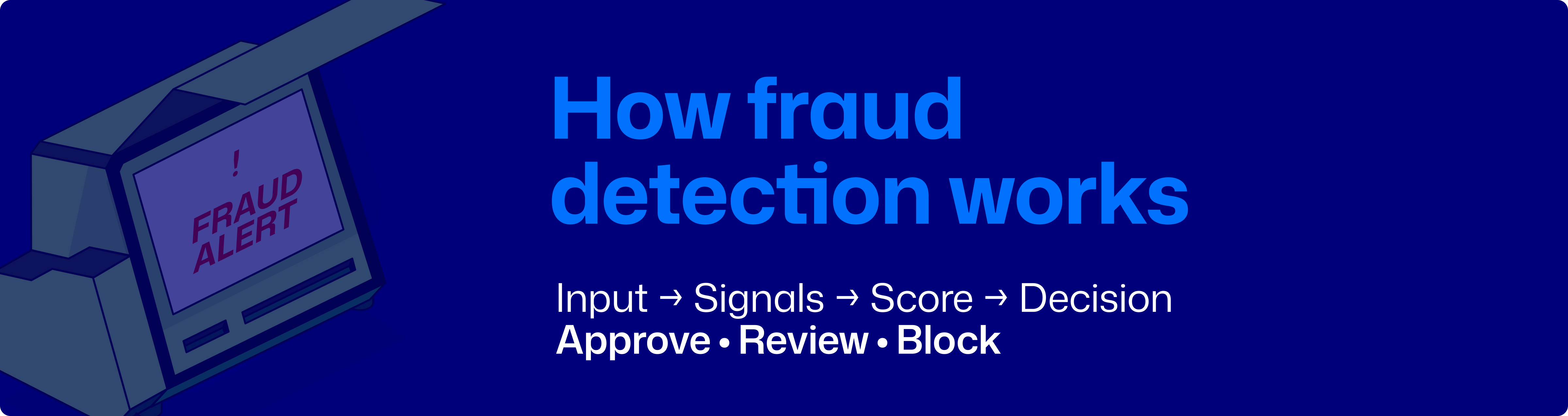

Building a Signup Fraud Detection Flow

A strong fraud detection system doesn’t rely on a single check. It combines identity, signals, and behavior into a structured decision-making flow.

A typical flow looks like this:

- Input collection: When a user signs up, the system captures their details, device info, IP, and behavioral patterns. This initial stage gathers all the data needed for evaluation without delaying onboarding.

- Signal analysis: Each collected signal is assessed for anomalies. The system checks for reused devices, suspicious emails or phone numbers, unusual locations, and behavioral inconsistencies. Individually, these may seem minor, but together they reveal potential fraud.

- Risk scoring: Signals are combined to assign a risk score to the account. Higher scores indicate a stronger suspicion. This quantitative approach allows teams to prioritize investigations and trigger automated actions only when necessary.

- Decision: Based on the score, the platform either approves the signup, requests additional verification, or blocks the account. This ensures legitimate users are not unnecessarily delayed while keeping fraudulent accounts out.

This layered flow is what separates basic verification systems from true fraud and risk infrastructure. To implement this in practice, fintechs need infrastructure that connects identity, device, and behavioural signals into a single risk system.

Profiled Risk by Dojah is designed for this exact purpose, combining multiple data points into a real-time risk score so teams can detect suspicious patterns early and act before fraud occurs.

Prevent Fake Signups with Dojah

Fake accounts threaten platform security, user trust, and growth. Detecting them early, at signup, requires more than KYC; you need continuous monitoring of devices, behaviors, and signals to stay ahead of evolving fraud tactics.

Dojah ‘s Profiled Risk provides real-time monitoring and behavioral risk profiling, making it easier to detect bots, synthetic users, and coordinated fraud rings before they can exploit your platform. By combining identity, device, and behavioral insights into a single view, teams can make faster, smarter decisions while keeping legitimate users moving smoothly through onboarding.

For fintechs scaling quickly or dealing with high-risk signups, upgrading your fraud detection system is the next step. Dojah provides the tools to catch threats early, reduce false positives, and protect both your platform and your customers.

Ready to strengthen your signup flow and stop fake accounts before they impact your platform? Explore fraud detection signals with Dojah and see how multi-layer detection works in practice.

FAQs on Detecting and Preventing Fake Signups

- What is a fake account at signup?

A fake account is one created to exploit your platform, often using stolen or synthetic identities. These accounts can commit fraud, abuse promotions, or undermine user trust. - Why does KYC alone fail to stop fake accounts?

KYC verifies identity, but it doesn’t detect behavioral anomalies, device reuse, or coordinated fraud patterns. Fake accounts can pass KYC while preparing to exploit the system. - What signals reveal fake accounts?

Key signals include device fingerprinting, email/phone reputation, IP intelligence, and behavioral inconsistencies. Combined, these signals help detect suspicious signups early. - How can fintechs implement layered detection?

By combining multiple signals into a risk score, platforms can prioritize high-risk accounts, trigger additional verification, or block fraudulent users, all while minimizing friction for legitimate users. - How does Dojah’s Profiled Risk help prevent fake signups?

Profiled Risk collects device, identity, and behavioral signals in real time, assigning a risk score to each signup. This helps teams detect bots, synthetic users, and fraud rings before they impact the platform.

Start using Dojah for all your business needs