Go back to Blog

Jennifer Edidiong

Marketing

11 min read

Share to

Fraud Detection in 2025: Processes, Tools & Best Practices

Fraud is one of the biggest threats facing businesses and consumers across Africa. Every year, the continent loses an estimated $88 billion to fraudulent activities, with industries like banking, fintech, and e-commerce feeling the biggest impact.

As online transactions continue to rise, fraudsters are becoming increasingly sophisticated in exploiting security gaps. Without a strong fraud detection strategy, your platform could face financial losses and a decline in customer trust.

In this article, we’ll break down how fraud detection works in 2025, the hurdles you might encounter, and how to pick the right tools to safeguard your platform.

What Does Fraud Detection Mean in 2025?

In present times, stopping fraud is no longer just about catching someone after the damage is done. With more advanced scams and digital threats on the rise, it’s about safeguarding your business from potential risks beforehand and meeting government AML regulations.

There are two main parts to this: fraud detection and fraud prevention.

Fraud detection is the process of identifying suspicious activity in real time or shortly after it occurs. This may happen when a customer’s location suddenly changes, their purchasing behavior shifts, or their account activity raises concerns. It is reactive, relying on tools and teams to quickly spot red flags and act on them.

Fraud prevention, on the other hand, is about reducing the risk of fraud before it happens. It focuses on putting the right policies, processes, and controls in place so you can get ahead of fraudulent activity on your platform. These are often guided by regular risk assessments that make it harder for fraud to occur at all.

Both fraud detection and prevention are key to building a stronger defense for your business against the growing risks of financial crime while helping you stay compliant.

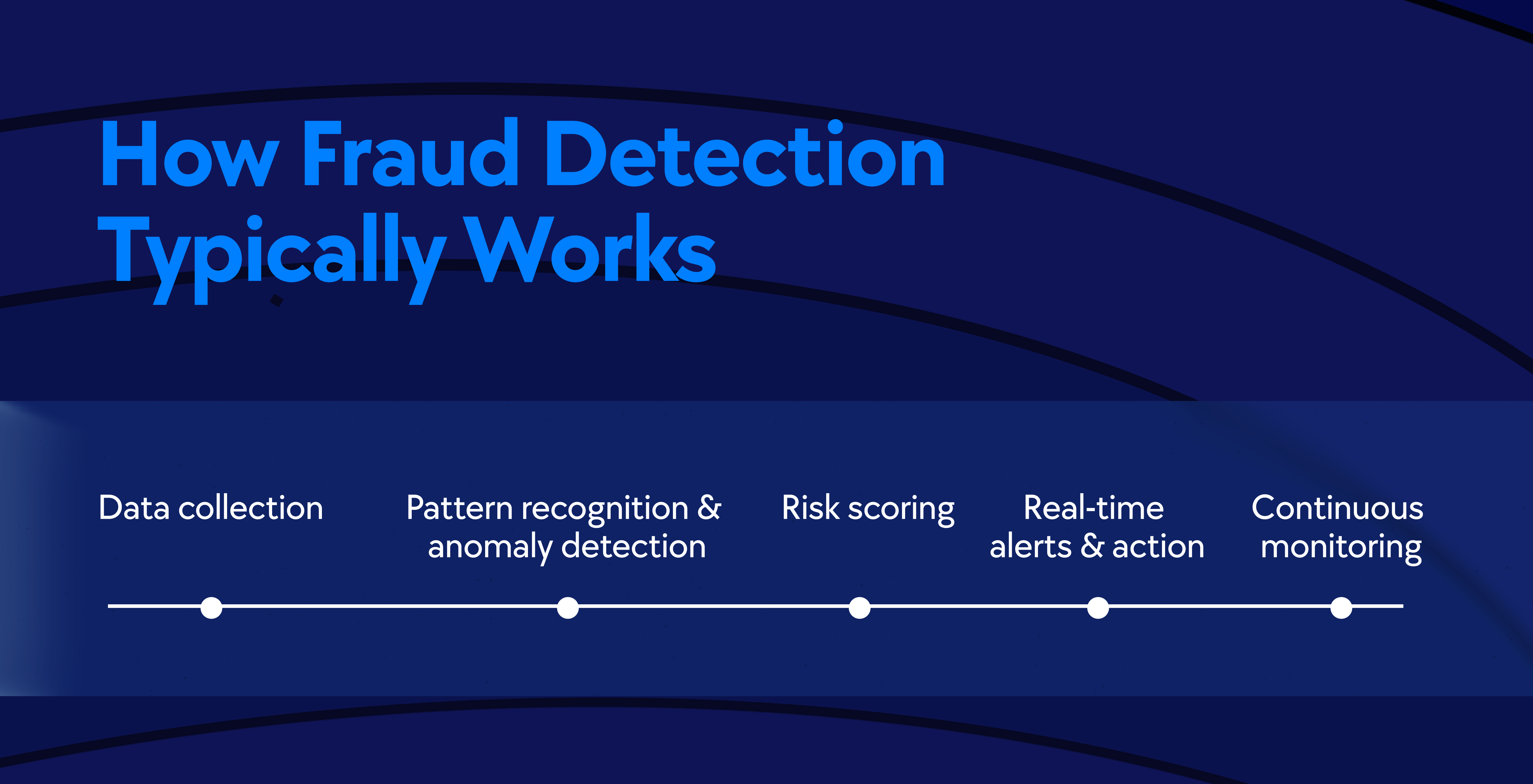

How Fraud Detection Typically Works

There are core processes usually involved in carrying out fraud detection practices. This includes:

1. Data Collection

Fraud detection starts with gathering data from multiple sources, such as transaction records, user behavior patterns, device details, and identifiers like IP addresses or geolocation. The more accurate and complete the data, the more effective the system will be. Modern tools collect and enrich this information in real-time so that suspicious activity can be flagged quickly.

2. Pattern Recognition and Anomaly Detection

Once collected, the data is reviewed for signs that stand out from normal activity. Pattern recognition identifies expected trends, while anomaly detection spots rare or unusual behavior. These techniques, powered by statistical analysis and machine learning, adapt quickly to new fraud tactics.

3. Risk Scoring

After patterns are analyzed, each transaction or activity is given a risk score based on rules, historical data, and predictive analytics. Higher scores signal a greater likelihood of fraud, helping your team decide how to respond. Real-time scoring ensures that these assessments remain accurate as new data comes in.

4. Real-Time Alerts and Action

Speed is crucial in fraud detection. Real-time monitoring systems continuously review incoming data, instantly flag suspicious activity, and can trigger actions like blocking transactions or requesting extra verification. The faster the response, the more damage you can prevent and the safer your platform remains.

The Technologies Behind Modern Fraud Detection

Effective fraud detection relies on advanced systems and processes to catch suspicious activity quickly. Here’s an overview of the most widely used technologies in fraud detection:

1. AI and Machine Learning

Artificial intelligence and machine learning analyze huge volumes of data in real time, learning and improving as new threats emerge. These systems can uncover hidden patterns and detect complex fraud attempts that traditional methods might miss. By processing transactions in milliseconds, AI-powered solutions reduce false positives and help you make faster, more accurate decisions for your business.

2. Rule-Based Detection Systems

Rule-based systems flag transactions that match set criteria, such as unusually high amounts, unfamiliar locations, or mismatched devices. They are straightforward and provide immediate results, making them a reliable first line of defense. These systems need regular updates to keep up with evolving fraud tactics and prevent excessive false positives.

3. Behavioral Biometrics

Behavioral biometrics is a security technology that analyzes unique human patterns, such as typing speed, swipe gestures, or even how a device is held. It runs silently in the background, continuously verifying identity without disrupting your users. This makes it highly effective for spotting account takeovers and automated fraud attempts on your platform.

4. Transaction Monitoring Systems

Transaction monitoring tools review financial transactions in real time, combining rules, pattern recognition, and AI to detect suspicious activity. They are crucial for both fraud prevention and regulatory compliance, helping your business quickly flag high-risk transactions. Alerts generated can trigger immediate reviews or reports to meet anti-money laundering (AML) requirements.

Example Workflows Using Fraud Detection Tools

Here are practical workflows showing how these technologies help detect and prevent fraud efficiently:

- Real-Time Transaction Risk Scoring

Transactions are scored instantly using historical behavior, geolocation, and device data. High-risk activity is flagged for review to reduce the chance of fraud. - New Account Activation Screening

When a user signs up, device trust, behavioral patterns, and identity data are evaluated. Suspicious signs trigger additional verification before full account access. - Behavioral Drift Alerts

Sudden changes in user behavior, like unusual logins or rapid transfers, prompt alerts. Transactions may be paused and reviewed to prevent misuse. - Identity-Focused High-Risk Actions

For sensitive actions, such as changing account settings, identity verification is enforced through biometric checks or document validation.

Practical Applications of Fraud Detection Across Industries

Fraud prevention tools are widely adopted across multiple industries to stop fraud and maintain compliance. These are some practical examples showing how fraud prevention works in different sectors:

Banking & Financial Services

Running a bank or fintech requires monitoring transaction patterns, device fingerprints, and geolocation to detect unusual activity, such as mule accounts or money-laundering attempts.

Suspicious transfers or repeated unusual behavior are flagged in real time, allowing your team to step in before any funds are misused. This reduces losses and keeps your operations aligned with regulatory requirements.

2. E-Commerce

For e-commerce platforms, fraud analytics can assess order value, transaction speed, device consistency, and past customer behavior to detect payment fraud and account abuse.

High-risk transactions are flagged automatically, while legitimate orders continue smoothly. This protects your revenue, reduces chargebacks, and ensures a seamless experience for genuine customers.

3. Lending & Credit Scoring

Operating a lending platform involves evaluating both traditional credit data and alternative indicators, such as spending habits, device behavior, and mobile usage.

The system can spot synthetic or stolen identities, preventing fraudulent loan applications. This allows your team to make faster, more accurate credit decisions while minimizing fraud-related defaults.

4. Identity Verification During Onboarding

Onboarding new users securely requires combining document checks, biometric face matching, and liveness detection with risk signals like device trust and IP reputation. These checks flag suspicious accounts before they gain full access.

This approach reduces identity fraud, boosts completion rates for real users, and ensures your onboarding process stays compliant with KYC regulations.

5. Cryptocurrency Exchanges

Managing a crypto exchange platform means dealing with high-value digital assets and the challenges of semi-anonymous transactions. Fraud prevention tools can help you monitor wallet activity, transaction patterns, and IP or device data to spot unusual transfers.

By flagging suspicious activity in real time, you protect your users, prevent asset loss, and stay aligned with anti-money laundering regulations.

Challenges & Limitations in Fraud Detection

There are several challenges you may face while implementing fraud detection for your business. They include:

High False Positive Rates and Alert Fatigue

In some cases, fraud detection systems can flag legitimate transactions as suspicious, frustrating your customers and slowing operations. Limited customer histories in Africa, such as first-time users in rural areas, can make these false positives more common. False positives can spike up to 90 percent in the banking industry, overwhelming your team and draining resources.

2. Data Privacy and Regulatory Compliance

Balancing effective fraud detection with evolving data protection laws like Nigeria’s NDPA, Kenya’s Data Protection Act, and South Africa’s POPIA can be challenging. You need enough user data to train and run your systems while remaining compliant. Inconsistent enforcement across countries can make this even harder if your business operates in multiple African markets.

3. Cross-Border Fraud Complexities

When you’re expanding into different countries, extra layers of complexity come into play. Differences in national ID databases, KYC standards, and telecom records make it harder to verify identities and monitor suspicious activity. Cross-border payment fraud is growing quickly, taking advantage of fast, anonymous transfers that are difficult to trace.

4. High Implementation and Maintenance Costs

AI-based fraud detection solutions require investment in infrastructure, skilled staff, and ongoing maintenance. Smaller fintechs, e-commerce platforms, and lending startups may find these costs limiting. You may also face added challenges sourcing and training the necessary talent, which can increase expenses.

5. Integration with Legacy Systems

Older core banking and operational systems can make integrating modern fraud detection tools tricky. Limited integration slows deployment, reduces real-time insights, and can delay automated responses to threats. This is especially common in Africa, where some institutions have yet to upgrade their infrastructure.

Choosing the Right Fraud Detection Solution

With the above challenges in mind, one important step is knowing how to choose the right fraud solution that fits your needs. Here are the key criteria to consider:

Seamless Integration

The solution should integrate smoothly with your existing systems and workflows. You want a tool that works with your platform without creating bottlenecks or requiring extensive technical work. Easy integration ensures faster deployment and minimal disruption to your daily operations.

2. Real-Time Capability

Your tool should be able to analyze transactions and user behavior instantly, so you can flag suspicious activity as it happens. Real-time monitoring helps you prevent fraud before it impacts your customers or your business. This capability is especially crucial for high-volume operations, where delays could result in significant losses.

3. Effectiveness and Low False Positives

Choose a solution that accurately identifies fraudulent activity while minimizing false positives. Too many false alarms can overwhelm your team and frustrate legitimate users. A precise tool ensures your resources are focused on real threats, improving efficiency and customer experience.

4. Compliance Support

Compliance is critical for your business, especially when operating across multiple regions. Your fraud detection tool should help you meet regulatory requirements like KYC, AML, and data protection laws without adding extra complexity. Staying compliant protects your reputation and avoids costly penalties.

5. Scalability and Flexibility

As your business grows, your fraud detection needs will evolve. Your solution should scale with transaction volumes, new user patterns, and emerging threats. Flexible tools allow you to adjust rules, models, and monitoring criteria without overhauling your system.

Prevent Fraud and Stay Ahead with Dojah

Fraud detection and prevention are crucial for safeguarding your business, customers, and revenue. By identifying threats early, you can minimize risks, protect users, and ensure compliance with regulations. It’s important to seek the right tools early, before fraudsters exploit vulnerabilities.

That’s where Dojah comes in.

Dojah offers an all-in-one fraud detection solution with real-time transaction monitoring, automated flagging of suspicious activities, and advanced detection to help you stay ahead on your platform.

Our system is fast, easy to integrate, and trusted by leading businesses across Africa.

👉 Book a demo to get started today.

Frequently Asked Questions About Fraud Detection

What is fraud detection?

Fraud detection is the process of identifying suspicious activity, transactions, or behaviors that may indicate fraudulent activity. It uses tools and techniques to flag potential risks before they cause harm.

How does AI detect fraud?

AI detects fraud by analyzing large volumes of data in real time, spotting unusual patterns or anomalies, and learning from historical cases to improve accuracy over time.

What is the difference between fraud detection and fraud prevention?

Fraud detection identifies and flags suspicious activity after it happens or while it is happening. Fraud prevention focuses on stopping fraudulent activity before it occurs.

How can Dojah help me detect fraud early?

Dojah provides real-time monitoring, AI-powered checks, and identity verification to help businesses catch fraud before it causes damage.

Start using Dojah for all your business needs