Go back to Blog

Jennifer Edidiong

Marketing

12 min read

Share to

5 Red Flags in Fraud Detection for African Fintechs

Fraud detection in Africa remains one of the major challenges fintechs face today. The growing scale of fraud detection failures in African fintech has cost the industry billions, with financial institutions in Nigeria alone losing ₦52.26 billion to fraud in 2024.

Fintechs like Flutterwave lost ₦11 billion to a security breach caused by smurfing fraud earlier in 2024, while traditional banks, such as Wema, lost ₦685 million to fraud and forgery the previous year.

In a report by Techpoint, Oluwasegun Ojumola, Senior Fraud Analyst at PiggyVest, emphasized that fintechs must strengthen fraud detection and prevention strategies to identify risk signals before they escalate. Even the most advanced fintech fraud detection tools can't help if your team misses key patterns.

This guide highlights five red flags African fintechs often miss in fraud detection and how to close those gaps before they lead to costly breaches.

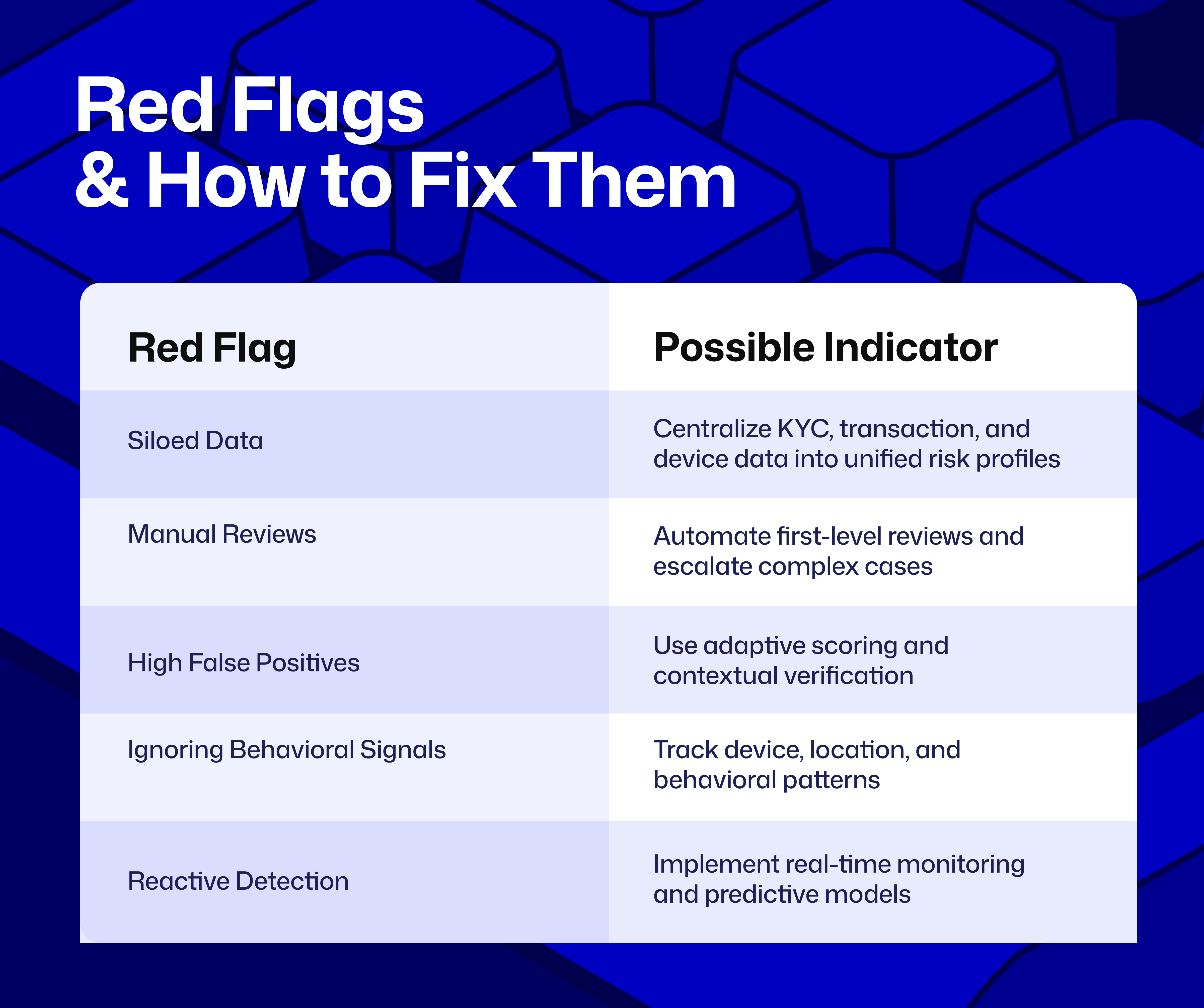

Red Flag #1: Siloed User Data

One red flag your fintech likely faces is scattered data across different systems. Your KYC checks might be handled by one provider, while transaction histories and device fingerprints are handled by another. That means your risk team has to jump between dashboards just to understand a single user.

Example: A fraudster uses a stolen BVN to open an account. Your KYC tool verifies it and approves the user. Within hours, they link multiple bank accounts under different names. Your transaction system flags the unusual pattern, but since it isn’t connected to your KYC data, no alert is triggered. By the time your team notices, the money is gone.

The Real Cost:

- Delayed detection: Fraud is discovered days later, when the money is already gone.

- Missed patterns: Repeat offenders slip through because each tool only shows part of the story.

- Wasted resources: Your team spends hours manually cross-checking data instead of investigating real threats.

The more scattered your data, the easier it is for fraudsters to bypass your systems and the harder it becomes for your fraud team to stop them in time.

Related: Fraud detection for fintechs: Tools & processes

Red Flag #2: Manual Fraud Reviews

Another red flag your fintech likely faces is relying too heavily on manual fraud reviews. Your risk or compliance team spends hours combing through spreadsheets, reviewing flagged transactions, and trying to connect dots across user profiles. By the time a suspicious case is confirmed, the fraudulent transaction has already gone through.

Example: A fraudster moves stolen funds through multiple small transactions over the weekend. Since your team only reviews flagged activity during work hours, those transfers clear before anyone notices. By Monday morning, all that's left are audit trails and a customer complaint.

The Real Cost:

- Slower response: Your team detects fraud after funds are already gone, not while it’s happening.

- Team fatigue: Your fraud analysts spend hours sorting false alerts instead of focusing on real risks.

- Inconsistent outcomes: Each reviewer applies different standards, which makes it easy to miss critical threats.

- Regulatory pressure: Delayed reporting puts your fintech under scrutiny from regulators, who demand faster detection.

Manual reviews remain common across African fintechs, creating a wide security gap for fraudsters to exploit.

Related: How to choose a transaction monitoring tool for your Fintech in Africa

Red Flag #3: High False Positives

African fintechs also deal with a high rate of false positives. When your fraud rules are overly strict or outdated, legitimate users get flagged as suspicious. According to a McKinsey report on fraud risks, nearly 90% of fraud alerts in digital banking could be false positives.

Example: A verified customer tries to make a simple transfer or apply for a loan, but your system blocks the transaction because it detects a potential risk. The BVN checks out, the ID matches, yet the activity gets flagged due to an outdated rule. The user tries again, same result. Before long, they move their transactions elsewhere.

The Real Cost:

- Customer frustration: Legitimate users abandon your platform after repeated verification errors or blocked transactions.

- Lost revenue: Every wrongly flagged transaction means lost fees, loans, or sales opportunities.

- Team inefficiency: Your fraud team spends valuable time reviewing clean cases instead of investigating real fraud.

- Brand damage: Users start associating your fintech with stress and friction instead of trust and convenience.

When your fraud controls lock out the right users while real threats slip through, your fintech is losing both customers and credibility.

Red Flag #4: Ignoring Behavioral and Contextual Signals

Another common blind spot in African fintechs is focusing only on static identifiers like BVNs or ID numbers while ignoring how your users actually behave. You might see a verified user and assume everything is fine, but if that same BVN is being used across multiple devices or geolocations within minutes, it’s a strong sign of potential fraud.

Example: A fraudster logs in using a stolen BVN from Lagos, then immediately makes transfers from Abuja and Accra using the same credentials. Your KYC system sees a verified BVN and lets it pass, while your transaction monitoring doesn’t connect the unusual patterns. By the time your fraud team notices, the money has already moved through multiple accounts.

The Real Cost:

- Delayed detection: Suspicious behavior goes unnoticed until it escalates, leaving your fintech exposed.

- Missed fraud patterns: Cross-device or cross-location activity isn’t linked, so repeat offenders slip through your system.

- Increased losses: Fraudsters exploit gaps between static checks and dynamic behavior, draining funds before your team can react.

Without behavioral signals, your fraud detection is blind to how users actually act and fraudsters exploit that blindness every single day.

Also see: How Fraud detection works for banks in Africa

Red Flag #5: Reactive Instead of Predictive Fraud Detection

Finally, many African fintechs react to fraud only after it happens instead of anticipating it. You might detect suspicious activity through chargebacks or customer complaints, but by then, the fraudulent transactions have already affected your users and your balance sheet.

Example: A fraudster opens 8 accounts using stolen credentials and tests your system with ₦5,000 transfers. Your team only notices after 3 customers file chargebacks. By then, ₦400,000 has moved through your platform. When you eventually investigate, the fraud has already spread, and your resources are tied up figuring out what went wrong instead of stopping it in real time.

The Real Cost:

- Delayed response: Fraud is discovered after it’s already impacted your customers and your balance sheet.

- Financial losses: Small incidents quickly accumulate into significant losses across accounts.

- Reputational damage: Customers lose trust when fraud isn’t stopped before it hits them, slowing adoption and engagement.

For your fintech, relying on reactive detection means fraudsters will always move faster than your risk team, making financial losses inevitable.

How African Fintechs Can Strengthen Fraud Detection

Now that you've seen the red flags that can slip through your fraud detection and prevention system, here's how you can proactively prevent them and keep your fintech secure in Africa:

Centralize Your Risk Data

Bring all KYC, transaction, and device signals into one platform so your team has a complete view of user activity. Start by integrating your identity verification APIs and monitoring logs into a unified dashboard. This reduces manual cross-checks and helps you identify linked accounts more quickly.

2. Automate Fraud Detection

Set up automated alerts for unusual transactions or behaviors so suspicious activity is flagged instantly. Build rule engines that trigger alerts based on thresholds like multiple failed login attempts, rapid account linking, or unusual transaction amounts. This ensures your team acts in real time rather than waiting for manual reviews.

3. Reduce False Positives

Use adaptive risk scoring and machine learning models to adjust thresholds based on transaction trends, user behavior, and regional patterns. Instead of rigid rules that flag every anomaly, implement dynamic scoring that learns from your platform's real data. This minimizes the number of falsely flagged users while still detecting fraudulent activity.

4. Incorporate Behavioral Signals

Track dynamic activity such as device changes, geolocation shifts, and transaction patterns alongside static identifiers. Set up monitoring for cross-device activity, IP address changes, and unusual login times that don't match typical user behavior. Behavioral insights catch fraud that traditional KYC alone might miss.

5. Move to Predictive Fraud Detection

Shift from reviewing fraud only after incidents happen to anticipating risky activity before it escalates. Implement continuous monitoring systems that flag small anomalies like testing transactions or coordinated account openings early. By acting ahead of fraudsters, your analysts can protect users and reduce operational strain.

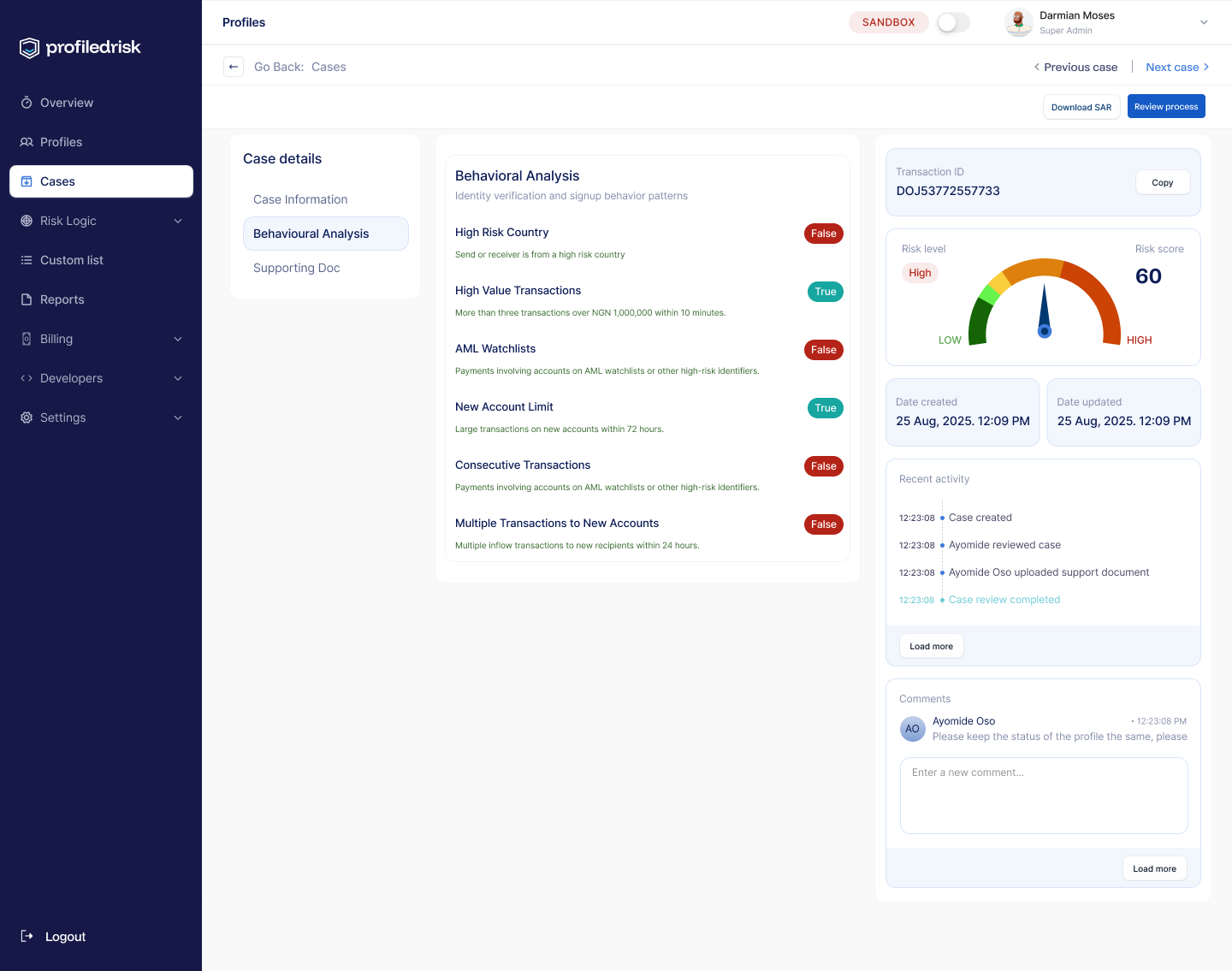

Dojah's Unified Fraud Detection Solution: Profiled Risk

At Dojah, we’ve seen how African fintechs struggle to connect fragmented data signals across identity verification, transactions, and device activity. Profiled Risk was built to solve that problem, giving your team a single source of truth for detecting, assessing, and preventing fraud in real time.

Here's what it enables you to do:

- Centralize all user signals in one profile: Bring together KYC data, transaction patterns, and device fingerprints in one unified profile. No more switching between dashboards or cross-checking CSVs. Profiled Risk consolidates signals from your identity provider, banking APIs, and behavioral analytics tools so you can see every user’s complete journey at a glance.

- Automate alerts and workflows: Set up automated triggers that flag suspicious activities, from multiple failed logins and unusual transaction bursts to device or location mismatches. Profiled Risk sends real-time alerts so your fraud team can act before losses occur, not after.

- Reduce false positives: Outdated, rigid fraud rules block legitimate customers and frustrate users. Profiled Risk applies adaptive risk scoring and contextual intelligence to differentiate between genuine behavior and potential threats, helping you reduce friction while catching real fraud faster.

- Monitor behavior in real time: Fraud doesn’t happen in isolation; it happens in patterns. Profiled Risk tracks user behavior across devices, geolocations, and accounts, surfacing anomalies that your traditional systems miss. This gives you deeper visibility into risky activity before it scales.

- Predict and Prevent Future Losses: Move beyond reactive fraud monitoring. Profiled Risk learns from past incidents and live transaction data to anticipate threats early. This predictive intelligence helps your team stay ahead of emerging fraud tactics and protect your platform at scale.

- AI/ML to detect hidden fraud patterns: Profiled Risk uses machine learning models to analyze user behavior, transaction trends, and historical data in real time. This helps your team spot emerging fraud risks early and take action before they escalate.

By consolidating fraud signals and providing actionable insights, Profiled Risk enables your team to respond to potential threats more quickly and prevent losses before they occur.

Helping African Fintechs Strengthen Fraud Detection

Effective fraud prevention isn’t about adding more tools; it’s about connecting the ones you already have. Profiled Risk helps African fintechs unify fragmented signals, close security gaps, and detect coordinated fraud before it causes real damage

With one consolidated platform, your risk and compliance teams gain:

- Full visibility into every customer’s identity and activity.

- Smarter automation that reduces manual reviews and team fatigue.

- Lower false positives, keeping genuine users verified and active.

- Real-time insights that empower faster, data-driven decisions.

Get early access to Profiled Risk and start turning identity, behavioral, and transactional data into actionable intelligence for fraud detection across Africa.

Frequently Asked Questions on Red Flags in Fraud Detection for African Fintechs

1. What are the most common red flags in African fintech fraud detection?

Siloed data, manual reviews, high false positives, ignoring behavioral signals, and reactive monitoring are common red flags. Spotting these early prevents costly losses.

2. How do fintechs reduce false positives in fraud detection?

Adaptive risk scoring and machine learning help flag only real threats. This keeps genuine users moving while catching fraud.

3. Why is centralizing risk data important for fintech fraud prevention?

Centralized KYC, transaction, and device data gives a full view of user activity. It helps spot linked accounts and coordinated fraud faster.

4. How can predictive fraud detection benefit African fintechs?

Predictive systems flags risky activity before it grows. This prevents losses and eases your team’s workload.

5. What role do behavioral and contextual signals play in fraud prevention?

Tracking device changes, geolocation, and transaction patterns uncovers fraud that static checks miss. Teams can act faster and smarter.

6. How can automation improve fraud detection in fintechs?

Automation flags suspicious activity instantly and makes reviews easier. Your team can focus on real threats instead of safe transactions.

Start using Dojah for all your business needs