Go back to Blog

Jennifer Edidiong

Marketing

11 min read

Share to

Transaction Monitoring: Processes, Tools & Challenges

Transactions are the heartbeat of financial services, powering everything from payments and lending to investments and e-commerce. Each movement of money represents trust between businesses and their customers. Yet with fraud on the rise, that trust is constantly at risk.

What happens when suspicious transactions slip through unnoticed?

With the rising rate of fraud, reports show that businesses with active monitoring systems detect anomalies 58% faster and cut losses by nearly 33%. This proves how critical real-time monitoring is as fraud tactics evolve across fintech, banking, and digital platforms.

Without a robust transaction monitoring system, your business risks not only financial losses but also reputational damage and regulatory penalties.

In this article, I’ll walk you through how transaction monitoring works, the challenges you may face, and the key features to consider when choosing the right tool for your business.

What is Transaction Monitoring?

Transaction monitoring is the process of reviewing customer transactions to spot unusual or suspicious activity. Instead of looking at one payment in isolation, it continuously tracks behavior over time, such as spending patterns, transaction speed, or fund movements, to catch risks before they become bigger problems.

This goes beyond basic fraud checks. A simple fraud check might flag a stolen card or block a single high-value transfer. Transaction monitoring, on the other hand, looks at the bigger picture. For example, if a customer suddenly starts making multiple $9,900 transfers just under the reporting threshold, the system can flag it as a potential money laundering activity.

Types: Real-Time vs. Post-Event Monitoring

There are two main types of transaction monitoring that businesses use to review and track financial activity:

Real-Time Monitoring

This reviews each transaction as it happens. If something looks suspicious, the system can pause or block it immediately. For example, a digital wallet can stop a transfer if the user’s behavior suddenly shifts, such as sending funds from a new location at an unusual time. It is powerful for fast-moving fintechs but can be resource-intensive to run.

Post-Event (Batch) Monitoring

This reviews transactions in groups, such as hourly or daily. It is easier to implement and useful for spotting trends or generating compliance reports. The drawback is timing, since by the time suspicious activity is flagged, the transaction may have already gone through.

Most fintechs and financial institutions use a mix of both. Real-time monitoring helps stop threats instantly, while post-event monitoring provides a broader view and deeper insights over time.

Why is Transaction Monitoring Important?

Here are some key reasons why transaction monitoring is important for your bank, fintech, or any digital business that deals with financial transactions:

Compliance with AML and KYC regulations

Transaction monitoring acts as your built-in compliance tool. It helps you meet anti-money laundering (AML) and know-your-customer (KYC) requirements by continuously checking that customer activity matches their profile. Without it, you risk fines, penalties, or even losing your license in regulated markets.

2. Fraud detection and prevention

Think of transaction monitoring as your early warning system against fraud. It tracks unusual behavior, such as rapid deposits or transfers that don’t fit normal patterns, and alerts you before losses occur. This keeps your customers safe while protecting your reputation as a trustworthy platform.

3. Risk management for financial businesses

Monitoring works like a radar for your business, helping you spot risks early and respond before they escalate. By flagging suspicious behaviors, you can reduce the chance of money laundering or other financial crimes affecting your platform, making it easier to maintain smooth, uninterrupted operations.

4. Customer trust and business growth

Transaction monitoring reassures users, partners, and regulators that your platform is safe. When customers feel protected, they are more likely to transact more, stay loyal, and recommend your service. For fintechs and startups, it can also ease fundraising, as investors value compliance-ready businesses.

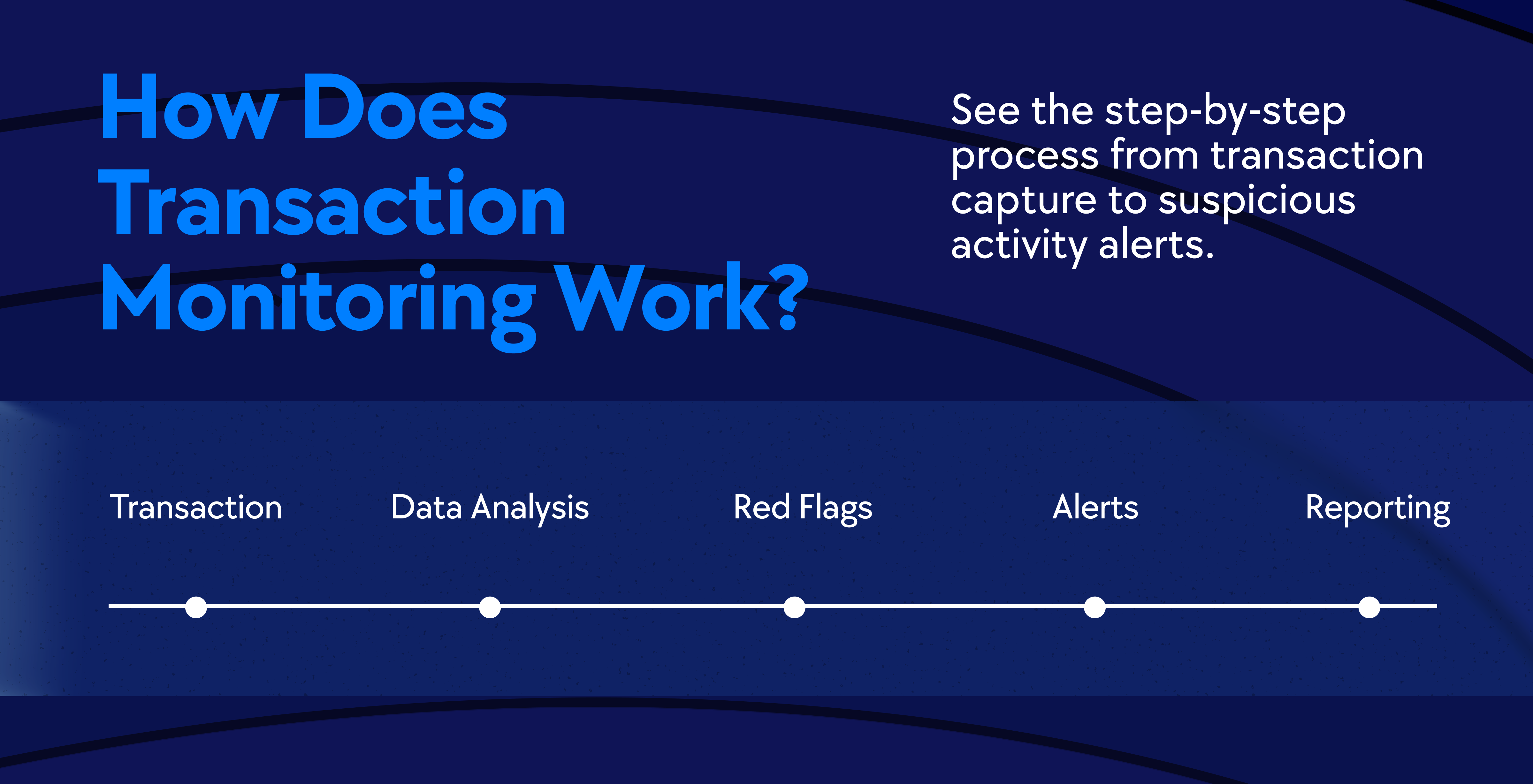

How Transaction Monitoring Works

Transaction monitoring involves some key steps to track activity and spot suspicious behavior. These include:

1. Data Collection

Everything starts with collecting the right data. Your system retrieves information from transaction records, user profiles, device details, and geolocation. Having complete data strengthens your ability to detect unusual activity, while modern tools enrich it in real time so you’re not relying on outdated information.

2. Pattern Recognition and Anomaly Detection

Once the data is in, the system begins identifying patterns. Normal spending or behavior trends are recognized, while unusual activity is flagged. This is where advanced analytics and machine learning step in, quickly adapting to new tactics so fraudsters don’t catch you off guard.

3. Risk Scoring

Every transaction is then assigned a risk score. This score is based on factors like historical activity, preset rules, and predictive analytics. A higher score signals a greater likelihood of fraud. Risk scoring helps you prioritize which activities need review without slowing down legitimate transactions.

4. Real-Time Alerts and Action

Your transaction monitoring system runs continuously, sending instant alerts when suspicious behavior is detected. Depending on your setup, it can automatically block risky transactions, request additional customer verification, or notify your compliance team.

Key Features of Effective Transaction Monitoring Software

When considering a transaction monitoring tool for your business, certain features can make all the difference. Here are the key capabilities to look out for:

Real-Time Alerts

This feature scans each transaction as it happens and flags suspicious activity immediately. For example, if a customer suddenly initiates multiple high-value transfers, your system can alert you or pause the transaction before any risk materializes. Real-time alerts help you act quickly and protect both your business and customers.

2. Customizable Rules and Thresholds

Every business is unique, and your transaction monitoring system should reflect that. You can set specific rules or thresholds, like flagging transactions above a certain amount or from certain locations. This ensures you’re catching the activity that matters most to your platform.

3. AI and Machine Learning Analytics

AI and machine learning help your system detect patterns beyond simple rules. It analyzes hundreds of signals and learns normal behavior, spotting subtle anomalies that might otherwise slip through. Over time, your monitoring becomes smarter and more accurate.

4. Regulatory Reporting

An efficient transaction monitoring tool helps you stay compliant with AML and KYC regulations. It can generate reports for regulators or internal audits, making it easier to prove that your platform meets legal requirements. This reduces the risk of fines or penalties.

4. Seamless Integration with Existing Systems

Your transaction monitoring software should connect smoothly with the systems you already use, such as KYC checks and payment processors. This reduces interruptions and speeds up implementation, letting you focus on running your business without technical hurdles.

Challenges in Transaction Monitoring

There are several challenges you may face while implementing transaction monitoring for your business. Understanding them can help you plan better and choose the right solutions. They include:

High False Positives

Sometimes legitimate transactions are flagged as suspicious, frustrating customers and slowing operations. High false positive rates mean your compliance team spends time reviewing alerts that aren’t risky. Over 95% of bank transaction alerts can be false positives, showing why optimizing monitoring is essential.

2. Evolving Fraud Tactics

Fraudsters are always adapting, finding ways around traditional monitoring. Your system needs to be flexible and quick to catch new fraud patterns without constant manual updates. Keeping ahead is a challenge, especially as payment methods and digital services evolve rapidly

3. Compliance Complexity Across Regions

Operating in multiple countries adds another layer of complexity. Each region has its own AML and KYC regulations, and ensuring compliance everywhere can be difficult. Differences in reporting requirements, customer data standards, and legal expectations mean you need reliable processes and consistent oversight

4. Scalability Issues

As your customer base grows, transaction volumes increase. Many monitoring tools struggle to keep up, which can lead to slower checks, delayed alerts, and missed risks. Ensuring your system scales effectively is crucial for smooth operations and protecting your business.

5. Data Integration Hurdles

Transaction monitoring works best with a complete view of customer activity, including KYC data, behavior patterns, and payment histories. Combining data from multiple sources can be difficult if systems don’t communicate smoothly, which can reduce visibility and limit monitoring effectiveness

Dojah’s Transaction Monitoring Solution

The challenges above highlight the need for a reliable monitoring system. Dojah’s EasyDetect brings fraud prevention and transaction monitoring in an all-in-one solution. Here, you get:

1. Accuracy you can trust

With Dojah, you get access to 99.9% data and verification accuracy, so you can trust every decision made. Our system ensures that your alerts are based on reliable, clean data rather than guesswork. This means your compliance team can focus on real risks instead of wasting time on harmless alerts.

2. Real-time detection

Speed matters when it comes to fraud prevention. Dojah’s EasyDetect works in real time, giving you immediate results the moment a transaction is reviewed. With a high detection speed, your team never has to worry about delays that could expose your business to risk.

3. Flexible rule management

Every business has unique compliance needs, which is why our system is built to be flexible. You can easily adjust and create rules to fit your specific use cases, whether that’s detecting high-risk payments, repeated suspicious activity, or region-specific risks. This flexibility gives you control without needing to rebuild processes from scratch.

4. Pre-built flow templates

Our pre-built flow templates are designed to make fraud monitoring easier from day one. These templates cover common use cases, so your team can start monitoring right away without spending time building workflows from scratch. Built with fraud managers in mind, they simplify onboarding and keep daily operations more efficient.

5. Seamless integration with identity verification

Transaction monitoring doesn’t work in isolation. Our solution integrates directly with KYC and other identity verification tools, ensuring you get a complete view of your customers and their activities. This combined approach strengthens fraud detection and delivers better results across the board.

6. Unique reporting system

Staying compliant requires accurate reporting, and our system is built to make that easier. It helps you prepare government-required documents such as Suspicious Transaction Reports (STRs) with less effort. With accurate data ready when you need it, your team can save time and confidently stay on top of regulatory obligations.

Prevent Fraud and Stay Ahead with Dojah

Transaction monitoring is essential for protecting your business, customers, and revenue. With the right systems in place, you can quickly spot unusual activity, reduce fraud risks, and stay compliant with regulations. Taking action early helps you prevent fraudsters from exploiting vulnerabilities.

Dojah’s EasyDetect offers real-time transaction monitoring, automated alerts, and advanced risk detection. This allows your business to stay protected while focusing on growth.

Our solution is fast, reliable, and trusted by leading businesses across Africa.

👉 Book a demo today to see how Dojah works for your business

Frequently Asked Questions on Transaction Monitoring

How does transaction monitoring work?

It tracks transactions in real time, analyzing patterns and anomalies. Suspicious activity is flagged instantly so your team can respond before losses occur.

Which industries benefit from transaction monitoring?

Fintechs, banks, e-commerce platforms, payment processors, and digital service providers all rely on it. Any business handling financial transactions can use it to detect fraud and manage risk.

What are the best transaction monitoring tools for businesses?

The best tools combine real-time monitoring, customizable rules, and AI-driven analytics. They should be accurate, easy to integrate, and scalable for compliance and risk management.

Which technology does transaction monitoring use?

AI, machine learning, and data analytics detect unusual patterns. Integration with KYC, payment systems, and behavioral data ensures timely and accurate alerts.

How can businesses detect suspicious transactions effectively?

By continuously monitoring transactions, setting thresholds for unusual behavior, and using automated alerts. This ensures quick responses while minimizing false positives.

How can Dojah help with transaction monitoring?

Dojah’s EasyDetect monitors transactions in real time, flags anomalies, and integrates with identity verification tools. It protects your business while keeping legitimate customer activity smooth.

Start using Dojah for all your business needs