Go back to Blog

Jennifer Edidiong

Marketing

11 min read

Share to

KYC & CDD Compliance for Fintechs: A Complete Guide

For fast-growing fintechs, compliance can feel like a constant trade-off between user experience and regulation. A single missed verification step can delay onboarding or invite penalties that damage your reputation.

You’ve probably heard the terms KYC and CDD used so often that they almost sound identical. Many founders and compliance teams even use them interchangeably. But while both play a key role in preventing fraud, they solve different problems.

Think of it this way: KYC helps you confirm who your users are, while CDD helps you understand why they’re here and whether you can trust their activity over time. Getting that balance right can make all the difference between seamless onboarding and unexpected regulatory issues.

As your fintech grows and handles more transactions, knowing how to apply both effectively becomes essential for maintaining compliance and scaling with confidence.

In this guide, you’ll learn how KYC and CDD differ, why the distinction matters for your fintech’s compliance and growth, and how to implement both without slowing your onboarding process.

What Is KYC in Fintech?

KYC, or Know Your Customer, is the process of verifying a user’s identity before they gain access to your platform or product. It’s the first step in building trust with your users and ensuring you know exactly who you’re doing business with.

In simple terms, KYC helps you confirm that your customers are who they claim to be. This involves:

- ID verification: Checking your users’ national ID, passport, or driver’s license.

- Document checks: Validating uploaded documents for authenticity and accuracy.

- Liveness detection: Using facial recognition or selfie checks to confirm the person submitting documents is real and present.

- Address verification: Confirming a user’s residence through utility bills, bank statements, or other proof of address.

For fintechs, KYC isn’t optional. It’s a regulatory requirement under AML/CFT frameworks, guided by bodies such as the CBN and SEC, following FATF recommendations.

What Is Customer Due Diligence (CDD)?

While KYC focuses on who your users are, CDD goes a step further to understand what level of risk they pose to your fintech.

CDD involves assessing and monitoring a user’s risk profile after their identity has been verified. It helps you evaluate whether a customer might engage in suspicious or illegal activities, and what measures to take to prevent that.

A complete CDD process includes:

- Risk assessment: Evaluating a user’s source of funds, transaction history, geography, and business type.

- Ongoing monitoring: Continuously reviewing user activity to detect anomalies or red flags.

- Record keeping: Maintaining up-to-date customer profiles and activity logs for compliance audits.

Depending on the user’s risk level, there are different levels of due diligence you’ll need to apply:

- Simplified Due Diligence (SDD): For low-risk users such as small retail accounts or basic wallets.

- Standard CDD: For regular users who present moderate risk.

- Enhanced Due Diligence (EDD): For high-risk or politically exposed persons (PEPs) who require deeper background checks and closer monitoring.

In short, KYC verifies identity while CDD verifies intent, and both are essential for keeping your fintech secure and trusted by users and regulators alike.

Related: A complete guide on KYC vs KYB for fintechs

Why KYC & CDD Compliance Matter for Fintechs

Here’s why KYC and CDD compliance is essential for your fintech:

Prevent fraudsters and shell companies

Fraudsters and fake businesses are always looking for easy targets. Strong KYC and CDD processes ensure that only legitimate users and companies join your platform. For example, a lending platform can prevent loan fraud by verifying both personal and business identities before approval.

2. Stay compliant and avoid penalties

Regulatory bodies require fintechs to maintain strict KYC and AML practices. Hence, non-compliance could lead to fines or license suspensions. Effective KYC and CDD processes protect your fintech from legal or financial risks, especially when handling cross-border transactions.

3. Improve user trust and investor confidence

Users trust platforms that take compliance seriously because it shows you care about protecting their data and funds. The same goes for investors and partners, as it gives them confidence that your fintech is stable and well-managed. A strong compliance record also positions your brand ahead of competitors.

4. Enable cross-border scaling by being compliance-ready

Expanding across borders comes with varying regulatory expectations. If you’re a Nigerian fintech planning to enter new markets like Ghana or Kenya, standardized KYC and CDD systems help you meet local requirements faster and onboard customers seamlessly.

Also see: Choosing a transaction monitoring tool for your fintech

Key Steps to Achieve KYC & CDD Compliance in Fintech

Here are the key steps to help your fintech stay compliant, reduce fraud, and build a smooth onboarding experience:

Collect accurate customer data

The first step is collecting accurate details such as name, date of birth, and address from your users. This information forms the foundation of your KYC process. When data is properly captured from the start, it becomes easier to verify identities and assess risk later.

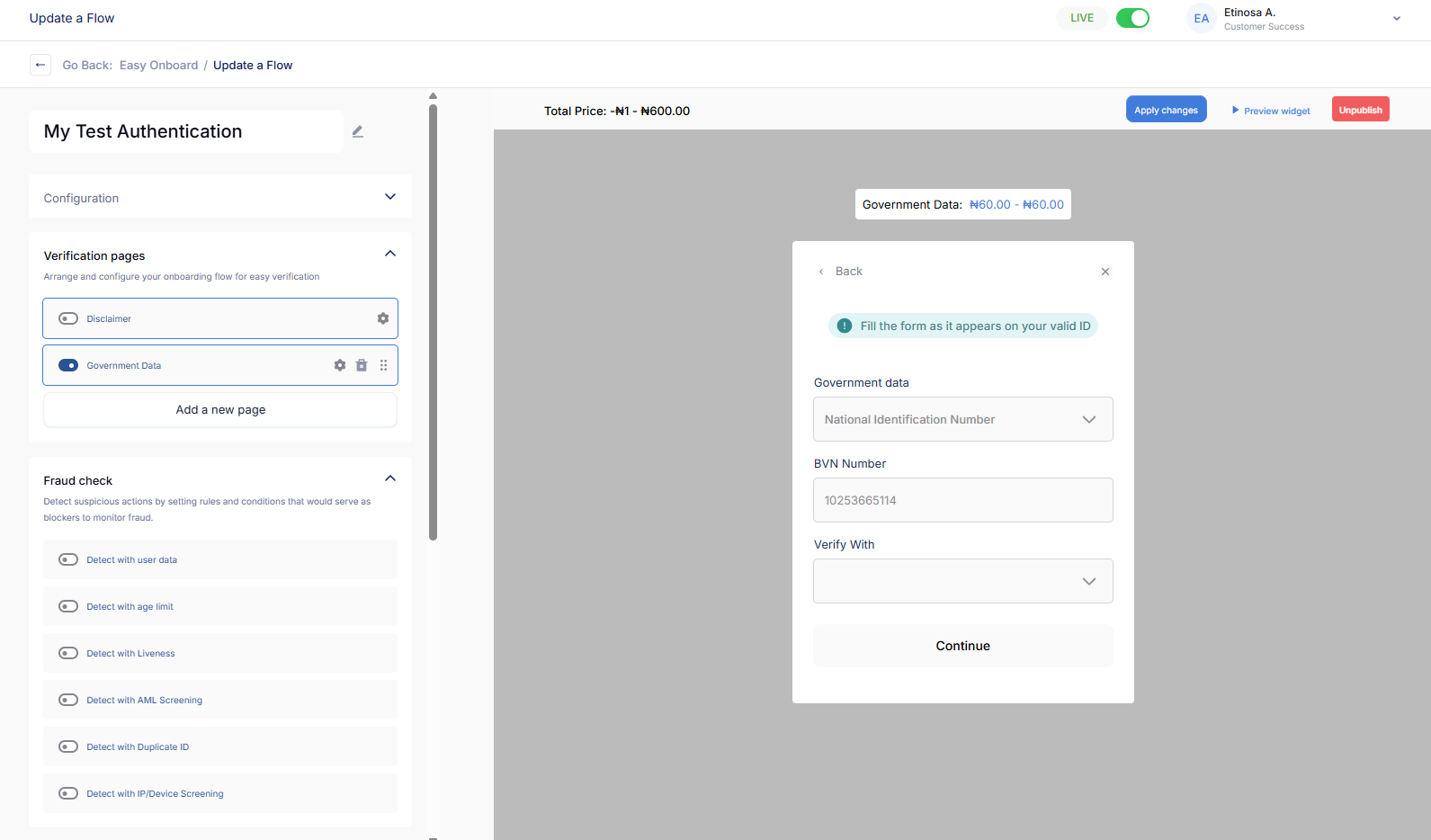

2. Verify identity and documents using automation

After gathering data, verify it using automated tools that check IDs, selfies, and documents in real time. This step speeds up onboarding and detects fake or tampered documents early. It also helps you reduce churn and avoid compromising compliance or accuracy.

3. Assign risk ratings to customers

Next, you assess each customer based on factors such as source of funds or transaction behavior. For example, users dealing with high transaction volumes or operating in high-risk regions should undergo enhanced checks. Assigning risk scores helps you focus on the right profiles.

4. Monitor transactions continuously

Compliance goes beyond onboarding. Regularly monitor user activities to detect unusual behavior or suspicious transactions early. High-risk customers should be reviewed more frequently to ensure their activities remain consistent with their profiles.

5. Report suspicious activity to regulators

When you identify potentially fraudulent accounts or irregular transactions, report them promptly through Suspicious Activity Reports (SARs) or Suspicious Transaction Reports (STRs). Timely reporting helps your fintech stay compliant and prevents association with financial crimes.

6. Maintain audit trails and compliance logs

Finally, keep detailed records of every verification, report, and compliance decision. Proper documentation proves your fintech has followed due process and supports the auditing process. It also helps your team track customer risk profiles over time.

See: The complete guide to KYC in Crypto

Want to simplify compliance? Book a 15-minute demo and see how top fintechs verify users faster with EasyOnboard.

Challenges Fintechs Face With KYC & CDD

In the process of implementing KYC and CDD for your fintech, there are challenges you’ll likely face. Here are some of the most common ones:

Manual onboarding and document reviews cause friction

If you still rely on manual KYC checks, your onboarding process can slow down and lead to errors. Your team may spend hours reviewing documents instead of focusing on more strategic work. This not only delays verification but can frustrate users who expect instant account access.

2. Complex regulatory expectations across countries

If your fintech operates across borders, you’ll notice how regulatory requirements differ from one country to another. A process that works in Nigeria may not meet the same standards in Ghana or Kenya. Keeping up with these changes and ensuring your systems comply with each market’s rules can be both time-consuming and costly.

3. Data accuracy and interoperability issues

Your KYC data often comes from different sources that don’t always integrate smoothly. This can lead to mismatched or incomplete customer records. When your systems don’t communicate properly, it becomes harder to maintain a single, accurate view of each customer.

4. Balancing user experience with security and compliance

It’s not always easy to balance fast onboarding with security checks. Too many verification steps can cause drop-offs, while too few open the door to fraud. To reduce churn, you’ll need to automate efficiently and keep your users informed at every step.

Simplify KYC & CDD with EasyOnboard

EasyOnboard is Dojah’s solution to the biggest KYC and CDD pain points fintechs face. It helps you prevent fraud while maintaining a seamless onboarding experience:

Accurate and real-time verification

Manual checks often cause delays and errors. With EasyOnboard, you can verify customer data and documents instantly using AI-powered identity checks and biometric validation. This improves accuracy and eliminates the friction that slows onboarding.

2. Liveness and biometric checks

Identity fraud remains a major issue for fintechs. EasyOnboard uses facial liveness detection and biometrics to ensure each user is genuinely present during verification. This reduces impersonation risks and helps you onboard only real users.

3. Automated compliance and risk scoring

Keeping up with AML regulations across markets can be overwhelming. EasyOnboard automates compliance workflows, applies risk scoring, and screens users against sanctions and PEP lists in real time. With this, your fintech can stay audit-ready and avoid regulatory penalties.

4. Seamless integration with your systems

Many teams struggle with disconnected verification processes. EasyOnboard integrates directly into your platform through a simple API, automating KYC and CDD flows end-to-end. This saves time, reduces manual errors, and ensures a smoother user experience.

5. Technical support and scalability

As your fintech grows, your verification needs evolve. EasyOnboard comes with ongoing technical support and flexibility to scale across regions. Whether you’re onboarding users in Nigeria, Ghana, or Kenya, you can maintain consistent compliance and performance.

See how Cleva reduced churn and simplified user verification across Africa with EasyOnboard

Prevent Fraud and Stay Ahead with Dojah

For fintech founders and compliance teams, KYC and CDD aren’t just about meeting regulations. They’re about protecting your platform, building trust, and scaling with confidence. Every verified user reduces your risk exposure and strengthens your reputation.

With EasyOnboard by Dojah, you can automate ID checks, liveness detection, and AML screening in one seamless flow. This makes the verification process faster, more accurate, and less stressful for your team.

Trusted by over 500 businesses and with more than 50 million verified identities, Dojah helps you prevent fraud and onboard users securely, no matter the market.

Book a demo today and see how EasyOnboard helps fintechs verify users, prevent fraud, and scale faster across markets.

FAQs on KYC and CDD for Fintechs

- What is the difference between KYC and CDD in fintech?

KYC verifies who a customer is, while CDD assesses their risk level and monitors ongoing activity to prevent fraud. - Why is CDD important for fintech compliance?

CDD helps fintechs identify high-risk users early, comply with AML regulations, and maintain trusted customer relationships. - What are the key steps in KYC and CDD for fintechs?

Key steps include data collection, ID verification, risk scoring, transaction monitoring, and reporting suspicious activity. - How can fintechs automate KYC and CDD processes?

Using tools like EasyOnboard, fintechs can automate ID checks, liveness detection, and risk scoring for faster, accurate verification. - What challenges do fintechs face in implementing KYC and CDD?

Common challenges include manual onboarding, changing regulations across countries, and balancing speed with compliance. - How does Dojah’s EasyOnboard help fintechs stay compliant?

EasyOnboard automates KYC, CDD, and AML screening in real time, reducing fraud risk and improving onboarding efficiency

Start using Dojah for all your business needs