Go back to Blog

Jennifer Edidiong

Marketing

9 min read

Share to

KYC vs KYB for AML Compliance: What You Need to Know

Fintech founders spend hours chasing incomplete KYC data and verifying shell companies manually. These aren’t just delays, they’re compliance risks that can cost millions in lost trust and regulatory penalties.

With the global fintech market projected to reach $395 billion in 2025, fintechs are scaling faster than ever, driven by rapid adoption across industries. But this growth also brings greater exposure to fraud and money laundering risks. Financial institutions lose billions each year to identity fraud and shell company schemes that slip through weak verification processes.

To combat these threats, strong identity and business verification measures are essential. KYC confirms who your customers are, while KYB ensures the businesses you onboard are legitimate and compliant. Together, they form the foundation of effective AML controls and sustainable growth.

In this guide, you’ll learn the core differences between KYC and KYB, why both are critical for AML compliance, and how to avoid common challenges fintechs face when implementing them.

What Is KYC (Know Your Customer)?

KYC, or Know Your Customer, is the process of verifying your users before granting them access to your platform. It confirms that each customer is genuine by validating the personal details they provide during onboarding. Regulators such as the CBN and FATF recommendations, require financial institutions to verify customers under AML/CFT rules.

Here’s what a typical KYC process involves for fintechs:

- ID verification: Checking valid, government-issued IDs such as NIN, BVN, passport, or driver’s licence.

- Address verification: Confirming the customer’s residential address using utility bills, bank statements, or tenancy documents.

- Biometric and liveness checks: Ensuring the person behind the camera matches the ID submitted and is physically present during verification.

- Database screening: Cross-checking user information against watchlists, sanctions lists, and politically exposed persons (PEP) databases.

- Ongoing monitoring: Continuously reviewing customer activity to detect suspicious transactions or changes in personal data.

In practice, this means that when a user signs up on your fintech platform to open a digital wallet or access lending services, their identity is verified before any transaction happens.

What Is KYB (Know Your Business)?

KYB, or Know Your Business, is the process of verifying the identity and legitimacy of a business before allowing it to operate on your platform. While KYC focuses on individuals, KYB ensures that the companies they represent are legally registered and not involved in illicit activity. KYB is essential for ensuring that businesses on your platform are genuine and not being used to launder money or commit fraud.

How the KYB works:

- Business registration verification: Confirms that the company is officially registered with valid documentation.

- Ownership checks: Identifies the Ultimate Beneficial Owners (UBOs) who control or benefit from the business to ensure transparency.

- Director verification: Validates the identities of key directors and shareholders to prevent impersonation or fraudulent representation.

- Watchlist screening: Cross-checks the business and owners against global sanctions or fraud lists.

- Address and operational checks: Confirms the company’s physical address, business operations, and that it exists beyond just paper registration.

When KYB is implemented, it verifies a merchant or vendor’s legitimacy and prevents fake or shell businesses from exploiting your platform.

Related: Choosing a transaction monitoring tool for your fintech

Why KYC + KYB Matter for AML Compliance

Here are key reasons why both KYC and KYB are essential for maintaining AML compliance on your platform

1. Preventing financial crime and fraud

Without proper KYC and KYB checks, platforms risk exploitation by fraudsters or shell companies. Criminals can use fake identities or unregistered businesses to launder money or set up a money mule network. Implementing both processes helps platforms stop these schemes before they impact operations.

2. Ensuring regulatory compliance

AML laws and FATF guidelines require platforms to verify both customers and businesses. Failing to comply can result in fines, license suspensions, or restrictions in key markets. KYC and KYB together keep platforms aligned with local and global compliance requirements.

3. Building trust with users and partners

Thorough verification of users and businesses establishes credibility with customers and partners. Verified identities and legitimate companies foster confidence, attracting more users and institutional collaborations. This trust also strengthens long-term retention and platform growth.

4. Foundation for Customer Due Diligence (CDD)

KYC and KYB form the core of effective Customer Due Diligence (CDD) by providing verified data on both individuals and corporate clients. This combined insight allows platforms to monitor transactions, detect suspicious activity, and apply enhanced due diligence when needed.

See how Dojah automates KYC and KYB for financial institutions

Also see: How KYC in Crypto works

Challenges Fintechs Face with KYC & KYB (and How to Avoid Them)

Implementing KYC and KYB on your platform also comes with its own hurdles. Here are some common challenges fintechs face, including practical ways to overcome them.

1. Slow onboarding due to manual verification

One major challenge is relying on manual checks, which can slow down onboarding and frustrate users eager to access your platform. Automating identity and business verification allows you to approve users and merchants in minutes, providing a smooth onboarding experience.

2. Fragmented and hard-to-access data

Another hurdle is pulling information from multiple sources like CAC records, credit bureaus, and sanctions lists. This can be time-consuming and prone to errors. Using a unified verification system consolidates data in one place, making checks faster and easier to manage.

3. High compliance costs for early-stage startups

For early-stage fintechs, building thorough KYC and KYB processes can be costly. Manual verification, legal support, and infrastructure all add up. Leveraging scalable API solutions can provide robust compliance without heavy overheads, allowing your platform to grow sustainably.

4. False positives during verification

Sometimes, automated checks flag legitimate users or businesses incorrectly, causing friction in onboarding. Fine-tuning verification rules and relying on trusted data sources ensures accuracy while keeping the user experience smooth and efficient.

5. Staying ahead of evolving regulations

AML/CFT rules and business verification requirements change constantly, and missing updates can create compliance gaps. To comabt this, you need to partner with a provider that updates regulatory requirements in real time.

These challenges faced by fintechs show a need for a verification system that unites KYC and KYB seamlessly. This is where Dojah’s EasyOnboard comes in.

KYC + KYB for Fintechs with EasyOnboard

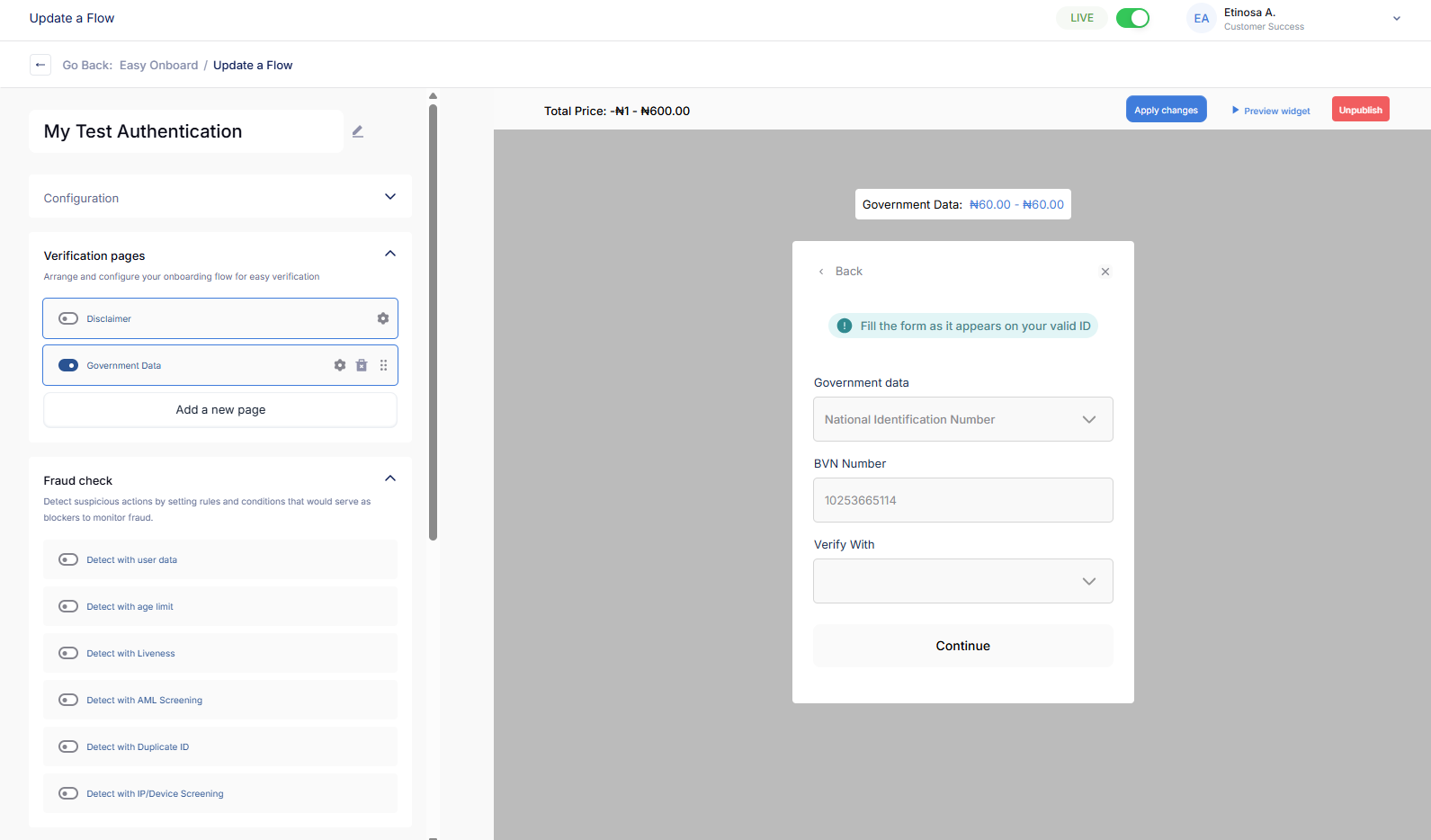

Dojah’s EasyOnboard is an all-in-one solution that simplifies identity and business verification. Here’s how it makes onboarding easier for your fintech:

1. Fast user verification

EasyOnboard verifies customers in seconds through document checks, liveness detection, and biometrics. This reduces onboarding drop-offs and helps real users access your platform instantly. Your fintech can verify new wallet users and let them start transacting in minutes, improving conversion and trust.

2. Business document validation

With KYB checks, EasyOnboard confirms business registration, ownership, and directors while screening against watchlists. This keeps fake or shell companies from accessing your platform and ensures each merchant onboarded is legitimate, thereby reducing fraud risk.

3. Global business checks

EasyOnboard supports verification of businesses across multiple regions, making international onboarding simple. This allows your platform to scale globally without extra compliance pressure. Whether onboarding a local startup or an overseas partner, your operations stay secure and audit-ready.

4. Ongoing AML screening

The platform continuously monitors users and businesses against PEP lists, sanctions, and other risk indicators. This ensures suspicious activity is detected even after onboarding. High-risk accounts can be flagged early, helping your fintech prevent financial crime before it escalates.

5. Seamless integration

EasyOnboard’s API connects directly with your platform and dashboards, automating verification flows and alerts. This simplifies your team’s workload, and leads tofaster onboarding with a smoother user experience.

Simplifying KYC and KYB with Dojah

For fintech founders and compliance leads, KYC and KYB go beyond regulatory checkboxes. They determine how securely and efficiently your platform runs. But managing verification across regions can get complex without the right tools.

With EasyOnboard, you can reduce onboarding time while meeting AML standards across multiple regions. This was the case of Wella Health, a healthtech startup, whose verification speed increased by 100%.

Our KYC solution automates ID checks, liveness detection, business validation, and AML screening in one unified API flow, improving accuracy, compliance, and user experience.

Trusted by 500+ businesses and with over 50 million verified identities, Dojah helps fintechs stay compliant, build trust, and scale faster.

Book a demo to get started today

FAQs: KYC vs KYB for AML Compliance

1. What’s the difference between KYC and KYB?

KYC verifies individuals to prevent identity fraud, while KYB checks a company’s structure and legitimacy. Together, they help fintechs confirm both users and the businesses behind them.

2. Why do fintechs need both KYC and KYB?

KYC alone can’t stop shell or fake businesses. KYB ensures that every merchant, vendor, or partner on your platform is authentic and compliant, reducing fraud and AML risks.

3. What are common KYB challenges?

Many fintechs struggle with incomplete business data, manual reviews, and slow onboarding. Using a unified solution like EasyOnboard helps automate checks and speed up verification.

4. How can fintechs stay compliant without slowing growth?

Automating KYC, KYB, and AML checks in one flow keeps onboarding fast while ensuring your platform meets regulatory standards.

5. What should you look for in a KYC/KYB provider?

Choose a solution that offers broad data coverage, real-time verification, and seamless API integration so your team can focus on growth, not manual compliance work.

Start using Dojah for all your business needs