Go back to Blog

Jennifer Edidiong

Marketing

10 min read

Share to

KYC in Ghana: A Guide to User Verification and Compliance

A major challenge you’ll most likely face when expanding into Ghana is keeping your business safe from digital fraud. In 2024, Ghana’s financial sector lost GH¢99 million to fraud, with mobile money platforms accounting for over GH¢18 million. With fraud this widespread, your platform is vulnerable the moment a user signs up.

KYC, or Know Your Customer, is verifying a customer’s identity to help your business avoid fraud, stay compliant, and build credibility. KYC in Ghana goes beyond fraud prevention; it helps prevent money laundering, terrorist activity, and other forms of financial misconduct. Ignoring KYC rules can lead to fines, penalties, or even being blocked from operating.

In this article, I’ll guide you through:

- KYC requirements in Ghana

- How KYC and AML compliance work in Ghana in 2025

- Steps to onboard customers successfully

- Common KYC challenges in the market

- How to scale eKYC in Ghana with real-time, biometric tools like Dojah

KYC Requirements and AML Compliance in Ghana

KYC processes in Ghana are regulated and enforced through the Anti-Money Laundering Act, 2020, and the Bank of Ghana’s AML/CFT guidelines.

This AML law forms the core of Ghana’s anti-money laundering (AML) and counter-terrorist financing (CTF) framework. It mandates all regulated entities to implement effective customer due diligence measures to identify and prevent financial crimes.

Who Must Comply With Ghana’s AML Laws?

Ghana’s KYC and AML requirements apply to a wide range of regulated industries. If your business operates in any of the categories below, compliance is vital:

- Banks and other financial institutions

- Fintech companies and digital payment providers

- Insurance firms and brokers

- Telecom operators offering mobile money services

- Forex bureaus and remittance service providers

- Accountants, legal practitioners, and other designated non-financial businesses and professions (DNFBPs)

What Happens If You Don’t Comply?

Ignoring KYC and AML laws in Ghana can come with major consequences:

- Regulatory actions such as penalties, suspensions, or loss of operating license by the Bank of Ghana or the Financial Intelligence Centre (FIC)

- Heavy fines up to 100%-500% of illicit funds

- Damage to your brand’s reputation and loss of customer confidence

Before diving into the documentation, tools like Dojah can already simplify most of the process. Explore how Dojah can help you verify customers faster in Ghana and stay compliant from day one.

Requirements for KYC in Ghana and Accepted Documents

KYC requirements in Ghana may vary slightly based on the type of customer or service. To stay compliant with Ghana’s AML laws and regulatory guidelines, you should know what’s typically required. Here’s a simple guide to help you collect the right documents during onboarding:

1. Proof of Identity

You must request valid, government-issued identification. These are the most commonly accepted:

- Ghana Card – the primary and mandatory ID for all Ghanaians and residents

- Non-Citizen Card – required for foreigners who reside in Ghana

- Passport – often used by foreign non-residents, especially for one-time transactions

- Driver’s License – can be used as a supporting ID, but not as a substitute for the Ghana Card when it’s required

2. Proof of Residential Address

To verify where a customer lives, you should ask for recent documents like:

- Utility bills (electricity, water, etc.)

- Tenancy or lease agreements

- Any official document confirming a residential address

3. Business Verification Documents (for corporate customers)

If you’re onboarding a company or registered business, request the following:

- Certificate of business registration

- Tax Identification Number (TIN)

- Proof of business address (e.g., utility bill or lease)

- Any other relevant company incorporation documents

4. Additional Supporting Information

For foreign nationals or non-residents, you may also need:

- Visa or permit details

- Entry date into Ghana

- Local contact address

5. Ongoing KYC and Record-Keeping

All documents collected must be verified for authenticity and cross-checked with records from the National Identification Authority (NIA). You should also update customer records regularly to reflect any changes.

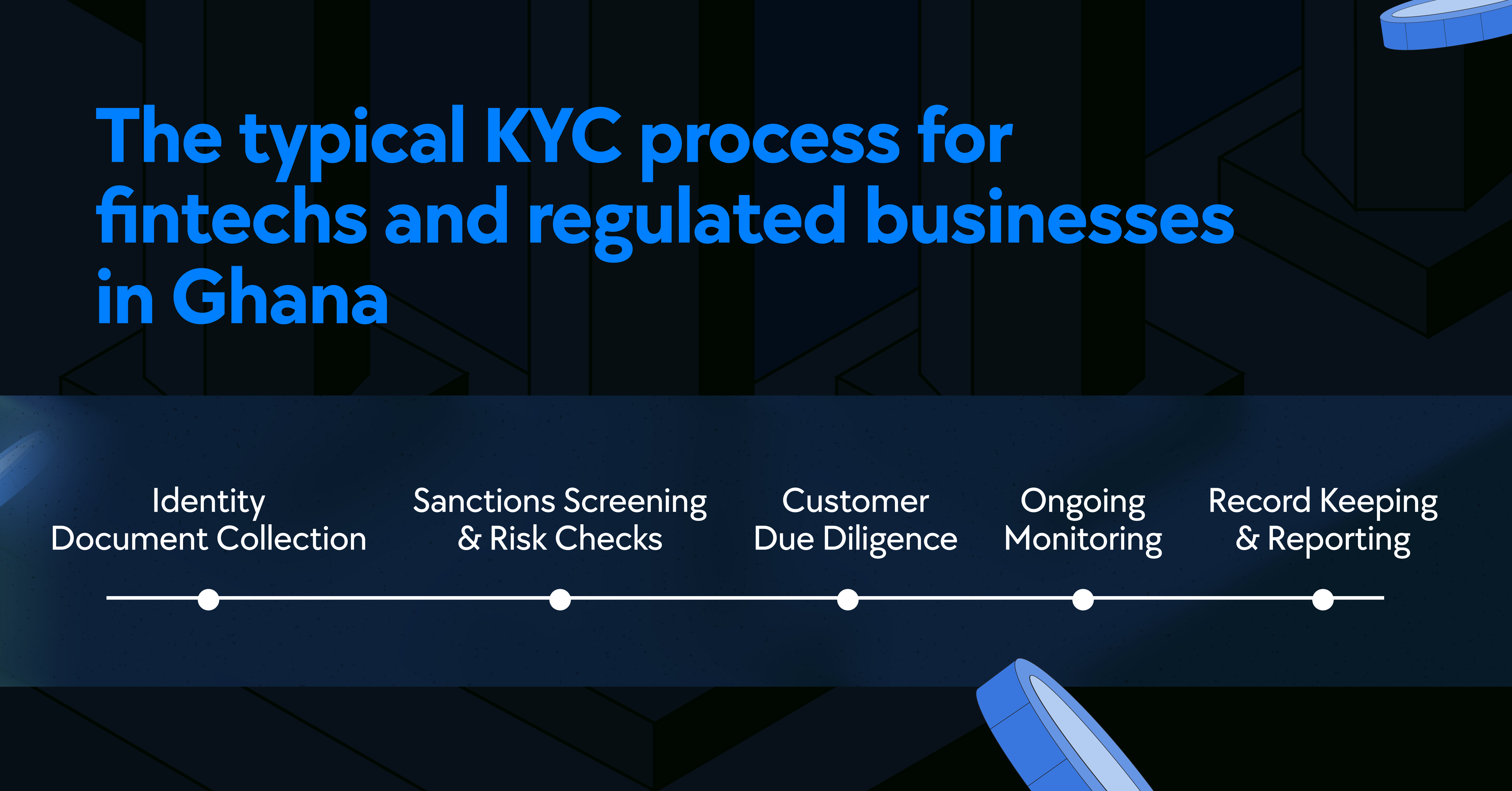

How KYC Works in Ghana: A Step-by-Step Guide

Here’s what the KYC process typically looks like for businesses operating in Ghana. By applying each step, you can maintain compliance and protect your platform from fraud.

Step 1: Identity Collection

Begin by collecting the customer’s Ghana Card (for citizens and residents) or Non-Citizen Card (for foreigners). For non-residents in Ghana for short periods, a valid international passport may be used for one-off transactions. Basic personal details such as full name, date of birth, and address should also be captured.

Step 2: Biometric Verification

Next, confirm the customer’s identity using biometric checks such as fingerprint or facial recognition, linked to the Ghana Card or Non-Citizen Card. This is done through real-time verification with the NIA database. Biometric data alone can still be used to complete the verification if the physical card isn’t present.

Step 3: Data Updates

Update the customer’s KYC profile using verified data pulled from the NIA. If there are mismatches in dynamic data, like phone number or address, they should be updated accordingly. If static data, such as name or date of birth, doesn’t match, the customer must be referred back to the NIA for corrections.

Step 4: Customer Due Diligence (CDD)

Screen the customer against global sanctions lists, Politically Exposed Persons (PEP) databases, and other high-risk watchlists. You may also need to collect additional information such as occupation, source of funds, or next of kin to complete the risk assessment.

Step 5: Ongoing Monitoring

After onboarding, your institution must monitor customer transactions continuously for unusual or suspicious activity. You’ll also need to periodically review and update customer records to ensure they remain compliant and reflect any changes in risk profile.

Step 6: Special Scenarios

For customers who haven’t registered for the Ghana Card or Non-Citizen Card, no financial transaction is permitted under current regulations. For non-residents staying in Ghana for fewer than 90 days, only one-off transactions are allowed using an international passport and supporting documents like visa details and entry date.

Digital/eKYC Trends in Ghana

Ghana is moving quickly toward a fully digital KYC system, led by stricter enforcement from the NIA. As of February 2025, all regulated transactions must now undergo real-time biometric verification using the Ghana Card.

Older methods, such as manual ID checks or document lookups, are no longer acceptable, as they leave room for errors and fraud. The NIA’s Identity Verification System Platform (IVSP) now supports secure biometric checks that are time-stamped and traceable.

Today, tools like facial recognition, video KYC, and liveness detection have become common among fintech, banks, and mobile money operators. These digital methods help reduce the risk of fraud and keep businesses in line with Ghana’s updated AML rules.

By September 2025, Ghana also plans to roll out a new crypto compliance framework. This will require Virtual Asset Service Providers (VASPs) and crypto exchanges to register with the Bank of Ghana and follow full AML and KYC procedures.

As eKYC becomes the standard across the country, now is the time to explore digital verification tools that help you stay compliant and onboard users with confidence.

👉 Want to stay compliant while scaling fast in Ghana? Learn more about how to get started.

Common KYC Challenges When Expanding into Ghana

Here are some of the KYC challenges you’re likely to face when entering the Ghanaian market:

1. Navigating Regulatory Overlaps

In Ghana, multiple regulators are involved in AML and KYC enforcement. This includes the Bank of Ghana, the FIC, and sector-specific bodies. Each of these regulators may issue updates at different times. This creates a constantly shifting compliance environment that can be difficult to track, especially if you're new to the market.

2. Limited Access to Centralized KYC Data

Even though the Ghana Card is the official ID for financial transactions, there's currently no unified KYC repository that all institutions can access. This means your customers may need to resubmit the same documents across different platforms, leading to delays and friction during onboarding.

3. Verifying Business Ownership Can Be Tough

When onboarding corporate clients, identifying who owns or controls a business isn’t always straightforward. Beneficial ownership and limited transparency often make it difficult to identify the business, especially in high-risk sectors like finance and crypto. This makes enhanced due diligence more challenging and time-consuming for your compliance team.

4. Manual Document Checks Are Still Common

Government records, like business registration or utility bills, aren't always digitized or easily verifiable. That makes it harder to confirm if submitted documents are genuine, increasing the risk of fraud and forcing you to rely on slow, manual review processes.

5. Tech Infrastructure Gaps in Some Regions

If you're planning to reach users outside urban centers, you may run into connectivity issues. Limited access to smartphones or stable internet can affect real-time biometric verification and video KYC, slowing down the entire onboarding process.

6. Meeting Ghana’s High Compliance Standards

Ghana’s AML laws require regular transaction monitoring, prompt reporting of suspicious activity, and robust recordkeeping. Setting up the right systems to meet these obligations can be resource-heavy, especially if you're still growing your compliance stack.

How Dojah Simplifies KYC Compliance in Ghana

KYC in Ghana can be complicated without the right setup or clear steps. You could end up dealing with manual reviews, slow approvals, or repeated ID requests that delay onboarding and frustrate users. All this while trying to keep up with Ghana’s changing compliance rules and requirements.

That’s where Dojah steps in. Dojah helps you stay compliant without losing speed, users, or sleep.

With Dojah, you can:

- Verify Ghana IDs instantly, using facial recognition and liveness checks connected directly to the NIA database.

- Make onboarding faster with AI-powered document checks and automated AML screening.

- Get started quickly with easy-to-use APIs and low-code tools, so your developers don’t get stuck setting everything up.

Our KYC solutions are fast, localized, easy to integrate, and trusted by top African businesses.

👉 See how Dojah helped Cleva power safe international payments across Africa.

Dojah offered us a seamless verification service via phone number data extraction that made our customer onboarding and verification process effortless. We’ve seen a clear boost in productivity since partnering with them.

— Joseph Okoroafor, Head of Marketing & Communications, WellaHealth

👉 Book a demo to get started today.

Frequently Asked Questions About KYC in Ghana

What is the KYC process in Ghana?

You have to verify users with the Ghana Card, run biometric checks, and screen for AML risks.

Can I run KYC checks digitally?

Yes. Real-time biometric verification and digital onboarding are supported in Ghana. Tools like Dojah integrate directly with the NIA’s system.

What are the biggest KYC challenges for fintech in Ghana?

Changing rules, identity verification gaps, and infrastructure issues.

How long does KYC onboarding typically take?

With digital tools, you can verify users in seconds. Manual processes may take longer.

Do I need local licensing to onboard users in Ghana?

Yes. Your business must be licensed and follow Ghana’s KYC and AML laws.

How can Dojah help with KYC in Ghana?

Dojah offers fast Ghana Card verification, AML screening, and simple API setup.

Start using Dojah for all your business needs