Go back to Blog

Jennifer Edidiong

Marketing

9 min read

Share to

KYC in Kenya: A Guide to User Verification and Compliance

Digital fraud and financial crimes are a growing threat to businesses in Kenya. Interpol lists financial crime as one of Kenya’s most pressing threats. For fintech founders, product leads, and compliance teams looking to grow or enter the Kenyan market, understanding how to implement KYC in Kenya effectively is non-negotiable.

KYC, or Know Your Customer, is the process of verifying a customer’s identity to protect your business from fraud, build user trust, and stay compliant with regulations. Beyond fraud prevention, KYC in Kenya plays a critical role in combating money laundering, terrorist financing, and other financial crimes. Failure to comply with the proper KYC measures could lead to hefty fines or even being shut down by the regulatory agencies.

In this guide, I will walk you through:

- KYC in Kenya,

- Requirements needed,

- Key steps to compliance,

- Common challenges, and

- How to set up a system that works at scale with solutions like Dojah that suit your needs for KYC in Kenya.

KYC Requirements and POCAMLA Compliance in Kenya

In Kenya, KYC processes are governed and enforced through the Proceeds of Crime and Anti-Money Laundering Act (POCAMLA 2009, Revised 2022). KYC typically requires collecting government-issued IDs, proof of address, and biometric data to confirm that users are who they say they are.

POCAMLA is the foundation of the country’s anti-money laundering (AML) and counter-terrorist financing (CTF) regime. It mandates that all regulated entities implement strict customer due diligence procedures to identify and manage financial crimes.

Who Must Comply With POCAMLA?

POCAMLA applies to a broad range of industries. If you operate in any of the sectors below, compliance is not optional:

- Banks and fintech companies

- Fintech and digital lenders

- Insurance providers

- Telecoms offering mobile money or financial services

- Real estate and legal professionals

- Casinos and gambling operators

Any business handling financial transactions or personal data involving Kenyan customers must implement customer due diligence in Kenya.

This means collecting and verifying key information such as:

- Government-issued identification (e.g., ID book, passport)

- Proof of residential address

- Biometric data (in some cases)

These steps ensure that customers are who they claim to be and that businesses can identify and report suspicious activity before it becomes a legal or financial risk.

What Happens If You Don’t Comply?

Non-compliance with KYC and AML laws in Kenya can trigger serious consequences:

- Penalties, suspensions, or license revocation by the CBK and FRC

- Fines under POCAMLA up to KES 10 million

- Reputational damage and loss of customer trust

Requirements for KYC in Kenya and Accepted Documents

Before you can onboard customers or launch financial services in Kenya, you need to understand the KYC requirements outlined under POCAMLA. This includes knowing exactly what identity and address documents are accepted during verification.

Here’s a breakdown of what your compliance team should request:

- Proof of Identity

A valid, government-issued ID is mandatory for every customer.- Kenyan National ID Card – primary ID for citizens, required during all KYC checks.

- Passport – valid passports accepted for non-citizens or Kenyans lacking other forms.

- Proof of Residential Address

To verify where a customer lives, documents must be recent (typically within 3 months).- Utility bills (electricity, water)

- Bank statements

- Lease or rental agreements

- KRA PIN Certificate

Confirms tax compliance and is needed for most financial activities.- Individuals: KRA PIN + national ID or passport

- Businesses: company PIN + directors’ PINs

- Business Verification Documents (for corporate accounts)

Required when onboarding entities rather than individuals.- Certificate of Incorporation + CR12 form (business ownership/directors info)

- Business KRA PIN certificate

- Memorandum and Articles of Association

Optional/Extended Checks: Depending on sector and risk, additional documents may apply:

- Electronic verification (e.g., scanning MRZ or holograms on IDs)

- Biometric checks (face-match or liveness detection)

- For minors: birth certificate + guardian’s ID

These steps cover mandatory KYC documents in Kenya, aligning with both the Central Bank of Kenya KYC guidelines and POCAMLA Regulations

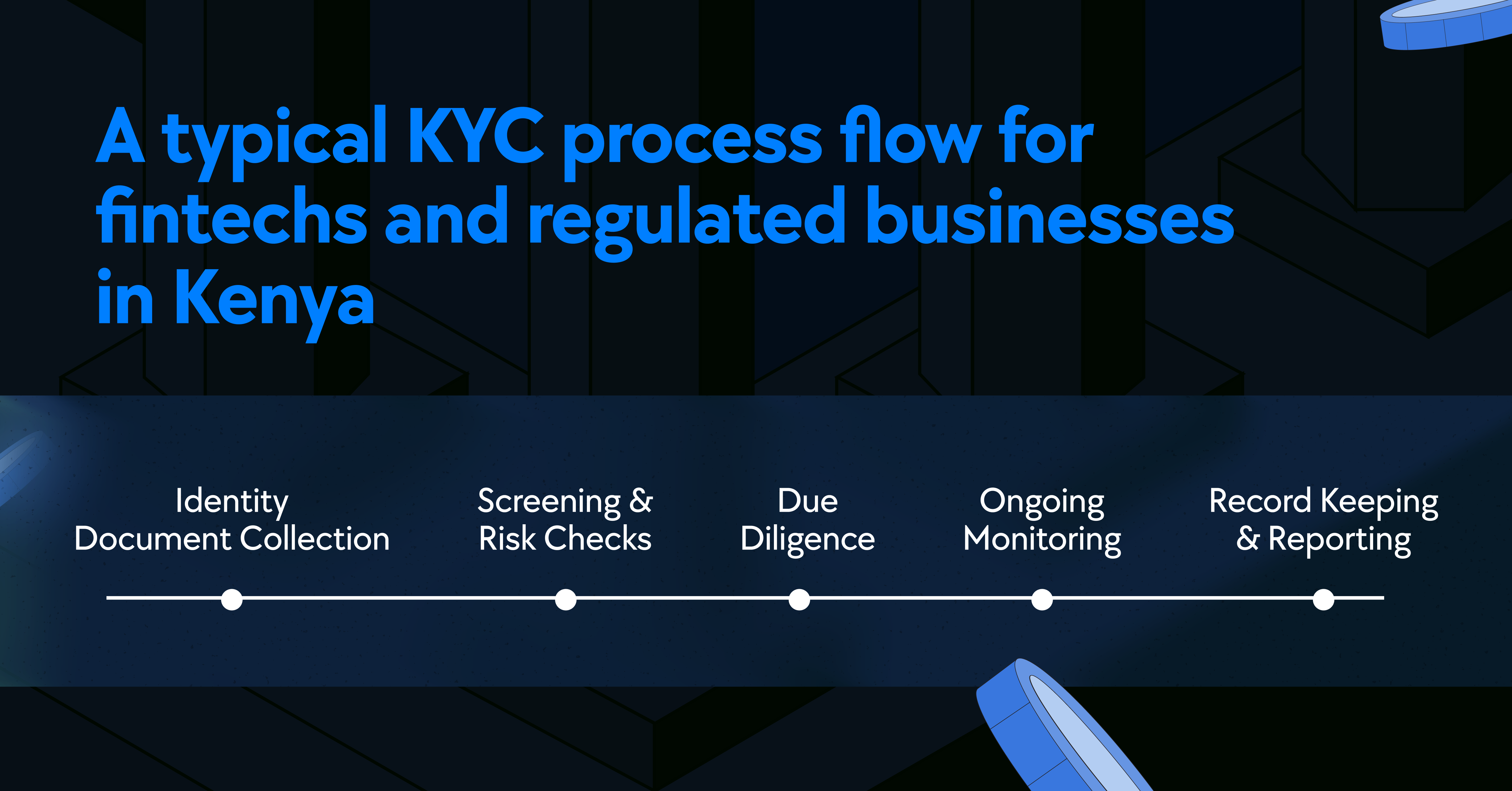

How KYC Works in Kenya: Step-by-Step Guide

Here’s what the KYC process typically looks like for fintech, banks, and other regulated businesses operating in Kenya. These steps help you stay compliant, onboard users smoothly, and reduce your exposure to fraud and financial crime.

Step 1: Customer Identification

Start by collecting valid ID documents such as a National ID for Kenyans or a passport for non-citizens. You’ll also need a recent proof of address and, for businesses, official company registration documents and KRA PINs.

Step 2: Sanctions and Risk Screening

Screen each customer against watchlists, sanctions databases, and politically exposed persons (PEP) lists. This helps you detect red flags early and assign the right risk category from the beginning.

Step 3: Customer Due Diligence (CDD)

Collect more background information such as the customer’s occupation, source of funds, and business purpose. Use this to classify them as low, medium, or high risk depending on the profile.

Step 4: Enhanced Due Diligence (EDD)

For high-risk customers, go deeper by verifying beneficial ownership and reviewing multiple information sources. Be sure to document every step of this enhanced review process.

Step 5: Ongoing Monitoring

Monitor customer transactions over time to spot unusual activity that may indicate risk. Update their risk levels whenever their behavior or situation changes.

Step 6: Record-Keeping and Reporting

Maintain complete and updated KYC records for at least seven years, as required by POCAMLA. Report any suspicious activity promptly to the Financial Reporting Centre (FRC).

Digital/eKYC Trends in Kenya

In early 2023, Kenya became one of the highest-risk countries for online ID fraud, with attempts rising from 10% in January to 17% by June. This sharp increase highlights the urgent need for modern, reliable identity verification systems.

eKYC systems powered by biometric checks and AI document scanners are now reducing fraud significantly. In fact, fintech platforms using SDK-based onboarding detect nearly twice as much fraud as those relying on standard APIs.

These tools don’t just improve security, they also speed up customer onboarding considerably. On average, ID verification in Kenya and across several African markets now takes less time.

As Kenya prepares to roll out a national digital ID, eKYC will become even more essential for regulated businesses. Implementing it now or early gives you a head start in compliance, user experience, and fraud prevention.

Common Challenges with KYC Compliance in Kenya

From high compliance costs to slow onboarding, here are the key challenges Kenyan businesses are facing when it comes to KYC:

1. Fake or Stolen Documents

Many businesses still struggle with forged documents and stolen IDs. Fraudsters now use high-quality fakes and even deepfake videos to trick verification systems. In early 2023, about 26% of ID attempts in Kenya were flagged as fake or stolen, the highest in East Africa.

2. Poor Internet and Low-Quality Devices

Even though many people use mobile phones, reliable internet isn’t always available, especially in rural areas. Some phones also can’t handle things like biometric capture. This may lead to combining manual and digital methods, which slows things down.

3. Complex and Changing Regulations

There are several regulations to keep up with, from the Central Bank’s AML rules to FRC reporting and data protection guidelines from the Data Commissioner. If you’re a fintech or a business operating across sectors, juggling all of these at once can be a lot. It often takes extra time and effort to stay on the right side of compliance.

4. Slow Onboarding Process

Manual checks and system issues can delay onboarding for hours or more. Generally, 68% of users abandon the process when verification takes too long or asks for too many documents. This affects your growth and makes you look less reliable.

5. Infrastructure and Trust Barriers

Power issues and a lack of trust in digital systems make things harder, especially in remote areas. Some people still prefer in-person processes, which means digital KYC adoption takes more time and effort.

How Dojah Simplifies KYC Compliance in Kenya

KYC compliance is a major bottleneck for startups in Kenya. Manual checks, high costs, and rigid document rules can slow you down and frustrate users. The majority of users tend to abandon onboarding when it’s sluggish or complex. And with fines like the recent Sh392 million CBK penalty on banks for weak due diligence, the consequences of non-compliance are real.

When you’re buried in paperwork and manual follow-ups, your team gets stuck and your growth stalls. That’s where Dojah steps in. Dojah helps you stay compliant without losing speed, users, or sleep.

With Dojah, you can:

- Verify Kenya IDs in real-time with facial recognition and liveness detection that stops impersonation fraud.

- Speed up onboarding with AI-powered document checks and automated AML screening.

- Easy developer integration means you can get started quickly without spending heavily on engineering resources.

Kenya’s regulatory landscape can be demanding, but Dojah makes it easier with automated AML checks and detailed verification logs. This helps startups stay compliant with POCAMLA, CBK, and FRC.

Choosing Dojah has been a game-changer for our company. Their technology is easy to use and secure. Their team is always helpful and quick to respond. Highly recommend their services to anyone looking to enhance their identity management system.

— Tomisin Adeshiyan, Co-founder & Head of Product Expansion, Vesicash

Whether you're a fintech, crypto exchange, or digital service provider, our all-in-one KYC infrastructure is built for teams that want faster onboarding, better fraud detection, and regulatory peace of mind.

Save Time and Reduce Churn with Dojah

If you’re a fintech startup or growing digital business in Kenya, looking to simplify your onboarding process, cut down fraud, and meet compliance without the friction, Dojah is built for you.

Our KYC solutions are fast, localized, easy to integrate, and trusted by top African businesses.

👉 Book a demo to get started today.

Frequently Asked Questions About KYC in Kenya

What documents can I use for KYC?

National ID, passport, or Alien ID, plus proof of address like a utility or bank statement.

How do KYC laws affect my business?

They require you to verify identities and report suspicious activity to stay compliant.

Can KYC be done fully online?

Yes. Tools like Dojah make it easy to verify users remotely.

What happens if I don’t comply?

You risk fines up to KES 10 million.

Start using Dojah for all your business needs