Go back to Blog

Jennifer Edidiong

Marketing

10 min read

Share to

KYC in Senegal: A Guide to User Verification and Compliance

A major challenge you’ll face when expanding your fintech or digital product into Senegal is keeping your platform secure from fraud.

And it’s not a hypothetical concern. Consumer reports show 43% of mobile financial service users experienced fraud or scams last year, and 32% suffered financial loss. Poor digital literacy and unclear verification processes only make it easier for fraudsters to slip through.

KYC, or Know Your Customer, is how you verify users, stay compliant, and protect your business from fraud risks. KYC in Senegal goes beyond fraud prevention; it plays a critical role in preventing money laundering and avoiding regulatory penalties that could delay your go-to-market plan.

In this article, I’ll guide you on:

- What the KYC process looks like in Senegal

- How to stay compliant under AML rules

- What you need to onboard users safely

- Key challenges with KYC in Senegal

- Biometric tools to scale eKYC

KYC Requirements and AML Compliance in Senegal

KYC processes in Senegal are regulated and enforced through the Anti-Money Laundering Law of 2024, the Beneficial Ownership Decree of 2020, and the Financial Sanctions Decree of 2023.

This AML law forms the core of Senegal’s anti-money laundering (AML) and counter-terrorist financing (CTF) framework. It mandates all regulated entities to implement effective customer due diligence measures to identify and prevent financial crimes.

Who Must Comply With Senegal’s AML Laws?

Senegal’s KYC and AML requirements apply to a broad range of regulated industries. If your business operates in any of the categories below, compliance is mandatory:

- Banks and other financial institutions

- Fintech companies and digital payment providers

- Insurance firms and brokers

- Telecom operators offering mobile money or financial services

- Forex bureaus and remittance service providers

- Accountants, legal practitioners, casinos, real estate agents, and other designated non‑financial businesses and professions (DNFBPs)

What Happens If You Don’t Comply?

Failure to comply with KYC and AML laws in Senegal can come with major consequences like:

- Regulatory sanctions, including fines up to CFA 100 million and potential suspension or revocation of operating licenses by BCEAO or CENTIF

- Criminal liability, including imprisonment or prosecution for willful non‑compliance under the AML law

- Loss of reputation and customer trust, leading to reduced partnerships and investor interest

Non-compliance can slow down your growth and expose your business to regulatory risks. With tools like Dojah, you can simplify compliance checks and verify your customers in Senegal faster.

Requirements for KYC in Senegal and Accepted Documents

KYC requirements in Senegal depend on the type of customer and service. To meet Senegal’s AML regulations and onboarding standards, these are the right documents to ask for:

Proof of Identity

You must require valid, government‑issued identification. Commonly accepted forms are:

- Senegal National ID Card (ANSD issue)

- Senegal Passport

- Senegal Driver’s License

- Voter ID card

Proof of Residential Address

To confirm a customer’s residence, request recent documents such as:

- Utility bills or bank statements

- Residence permit card (for foreigners)

Business Verification Documents (for corporate customers)

When onboarding a company, ask for:

- Certificate of incorporation or business registration

- Tax Identification Number (TIN)

- Proof of business address (e.g., utility bill or lease agreement)

- Names of directors and company representatives

Additional Supporting Information

For foreign nationals or non‑residents, also request:

- Valid residence permit or non‑citizen ID

- Passport details and date of entry into Senegal

Ongoing KYC and Record‑Keeping

All collected documents must be verified for legitimacy. Customer details such as address, occupation, and risk profile must be updated regularly. Institutions must retain documents for at least ten years from the date of account closure or relationship termination. Biometric or e‑KYC tools like liveness checks are often used to cross‑verify identity records.

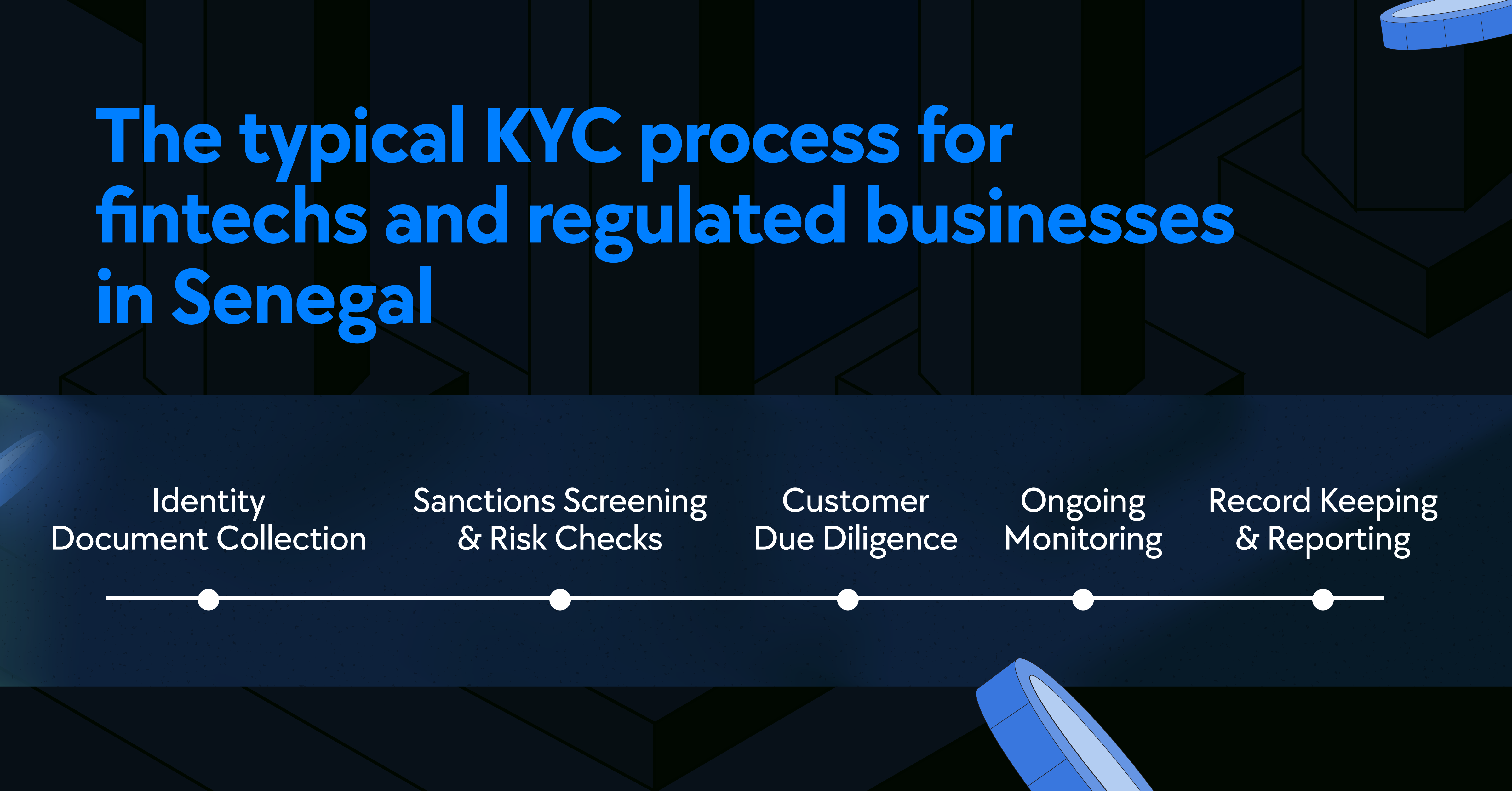

How KYC Works in Senegal: A Step‑by‑Step Guide

These are the key steps to stay compliant and safely onboard customers if you’re operating a fintech or digital business in Senegal:

Step 1: Identity Capture

Begin by collecting the customer’s Senegal National ID Card or Senegal passport. Record key details like full name, date of birth, and address. These documents are the primary KYC proof accepted by banks and digital platforms in Senegal.

Step 2: Biometric Verification

Verify the customer’s identity using biometrics such as facial recognition (selfie) or fingerprint. This confirms that the person matches official ID records and reduces the risk of identity fraud.

Step 3: Profile Update

Automatically fill in the customer profile with data from their ID document. If their address, phone number, or name details differ, prompt them to correct these via official channels before proceeding.

Step 4: Customer Due Diligence (CDD)

Screen each customer against international and national watchlists, including UN sanctions lists, Politically Exposed Persons (PEP) registers, and CENTIF alerts. If someone is flagged high‑risk, conduct enhanced due diligence; collect extra info like source of funds, occupation, or business type.

Step 5: Ongoing Monitoring

Continuously monitor transactions and review user profiles. Set up automated alerts for suspicious behavior. If any red flags emerge, promptly report Suspicious Transaction Reports (STRs) to CENTIF within the mandated timeframe.

Step 6: Special Cases

Apply simplified or tiered KYC for low‑value accounts or digital wallets. For non‑residents, onboard with passport data and verify date of entry or visa status. Agents managing mobile money may also follow lighter KYC flows for low‑risk users.

Want to make your KYC process easier? Use Dojah for seamless verification and faster onboarding. Learn more about how to get started.

Digital/eKYC Trends in Senegal

Senegal’s government has launched the “New Deal Technologique” strategy to modernize public services and build a biometric-based national digital ID system from 2025 to 2034. The goal is to secure digital access across sectors, including finance, health, business registration, and education.

Paper-based ID checks and manual onboarding are being phased out in favor of automated digital verification. Senegal introduced biometric ECOWAS-compliant eID cards in 2016 and is now building on that foundation with a national database of fingerprints and facial data.

This shift means onboarding with passports or ID cards can soon be verified digitally in real-time. Identity capture, biometric matching, and risk screening are becoming standard at mobile or web check-in, offering a faster and safer process.

With Senegal’s move toward a unified digital identity and eKYC ecosystem, now is the time to integrate with this national digital identity infrastructure. You’ll need to explore tools that will help you onboard customers securely, reduce fraud risk, and align with future AML compliance trends.

Common KYC Challenges When Expanding into Senegal

Here are some of the KYC challenges you’re likely to face when entering the Senegalese market:

- Limited digital access and inconsistent IDs

While Senegal has issued ECOWAS biometric ID cards, internet access is inconsistent, with 60% of the population using the internet, and rural areas often facing connectivity issues. This makes digital ID verification more technical in some regions and slows down onboarding.

2. Poor Data Sharing Across Institutions

Banks, fintechs, and mobile money providers often operate separately. Your team might find themselves collecting the same customer information multiple times or discovering conflicting data across systems. Without seamless data sharing between institutions, KYC and AML workflows become time-consuming.

3. Cross-border Regulatory Issues

Senegal is a member of the West African Economic and Monetary Union (WAEMU), so your KYC policies must align with national law, regional directives, and global sanctions. This multi-layered structure can create extra friction, especially when verifying beneficial ownership or monitoring transactions across borders.

4. Compliance Pressure as You Scale

Keeping up with KYC regulations in Senegal takes more than just ticking boxes. You’ll likely need to invest in new tools, train local staff, and keep up with changes in ID systems or onboarding policies. As an early-stage or growing business, staying compliant can quickly become a resource-heavy task.

Simplify KYC in Senegal and Save Time with Dojah

KYC in Senegal can be a hassle without the right setup or clear process. You might face manual reviews, delayed approvals, or repeated ID requests that slow down onboarding and frustrate your users. All this while trying to keep up with Senegal’s evolving KYC and compliance standards.

That’s where Dojah steps in. Dojah helps you stay compliant without losing speed, users, or sleep.

With Dojah, you can:

- Verify Senegal IDs instantly, using facial recognition and liveness checks connected directly to the government database.

- Make onboarding faster with AI-powered document checks and automated AML screening.

- Get started quickly with easy-to-use APIs and low-code tools, so your developers don’t get stuck setting everything up.

Our KYC solutions are fast, localized, easy to integrate, and trusted by top African businesses.

👉 See how Dojah helped Cleva power safe international payments across Africa.

Dojah offered us a seamless verification service via phone number data extraction that made our customer onboarding and verification process effortless. We’ve seen a clear boost in productivity since partnering with them.

— Joseph Okoroafor, Head of Marketing & Communications, WellaHealth

👉 Book a demo to get started today.

Frequently Asked Questions About KYC in Senegal

What is the KYC process in Senegal?

You’ll need to collect a customer’s government-issued ID (like a national ID or passport), verify it, run AML checks, and store the data securely in line with local and WAEMU regulations.

Can I run KYC checks online in Senegal?

Yes, but it depends on your setup. Some tools let you verify users online using facial recognition, document uploads, or biometric matching. However, access to real-time government data is still limited.

How long does KYC onboarding usually take?

If you're using digital tools, onboarding can be completed in seconds. Manual verification or missing documents can delay the process.

What are the biggest KYC challenges for fintechs in Senegal?

Fintechs often face regulatory complexity, slow licensing timelines, and limited access to centralized digital identity data. Many users also operate in the informal sector, which makes verification harder.

Do I need a local license to onboard users in Senegal?

Yes. You must be licensed by the BCEAO (Central Bank of West African States) or other relevant Senegalese authorities, and follow both national and WAEMU KYC/AML guidelines.

How can I verify a Senegalese national ID online?

There’s no public verification portal, but certain KYC tools offer integrations with official databases or perform biometric and document-based verification.

Is there a central KYC portal in Senegal?

Not at the moment. KYC is handled through a mix of manual checks and private integrations. Some providers help bridge this gap with all-in-one verification APIs.

How can Dojah help with KYC in Senegal?

Dojah allows you to verify IDs, run biometric checks, screen for AML risks, and onboard users faster using a single API built for West African markets.

Start using Dojah for all your business needs