Go back to Blog

Jennifer Edidiong

Marketing

9 min read

Share to

How Marketplace Platforms Can Stop Fake Merchant Onboarding

Every day, marketplace platforms onboard new vendors, sellers, and service providers to keep their apps active and growing. But in many cases, merchant onboarding is treated like a simple signup process instead of a trust check. As long as basic details and documents are submitted, merchants can sometimes go live with very little verification.

This problem recently came into sharp focus after a recent investigation by Techpoint Africa into how Glovo and Chowdeck verify merchants. Reporters successfully impersonated a real restaurant and got fake stores live using falsified or mismatched business information. It highlights how weak onboarding checks can quietly create trust risks before customers or platforms notice anything is wrong.

And this is not limited to food delivery platforms alone. E-commerce marketplaces, logistics apps, and online vendor platforms can face similar problems when they cannot properly verify who they are onboarding. This article breaks down how fake merchants bypass onboarding checks, what platforms often fail to verify, and how stronger verification can help marketplaces build trust.

How Fake Merchants Slip Through Marketplace Onboarding

Fake merchants don’t usually break into marketplace systems; they move through onboarding steps that don’t ask enough questions or verify deeply enough.

- Onboarding designed more for speed than security

Most marketplace platforms prioritise getting vendors live quickly so they can start selling as soon as possible. This focus on speed means deeper verification steps are reduced or delayed.

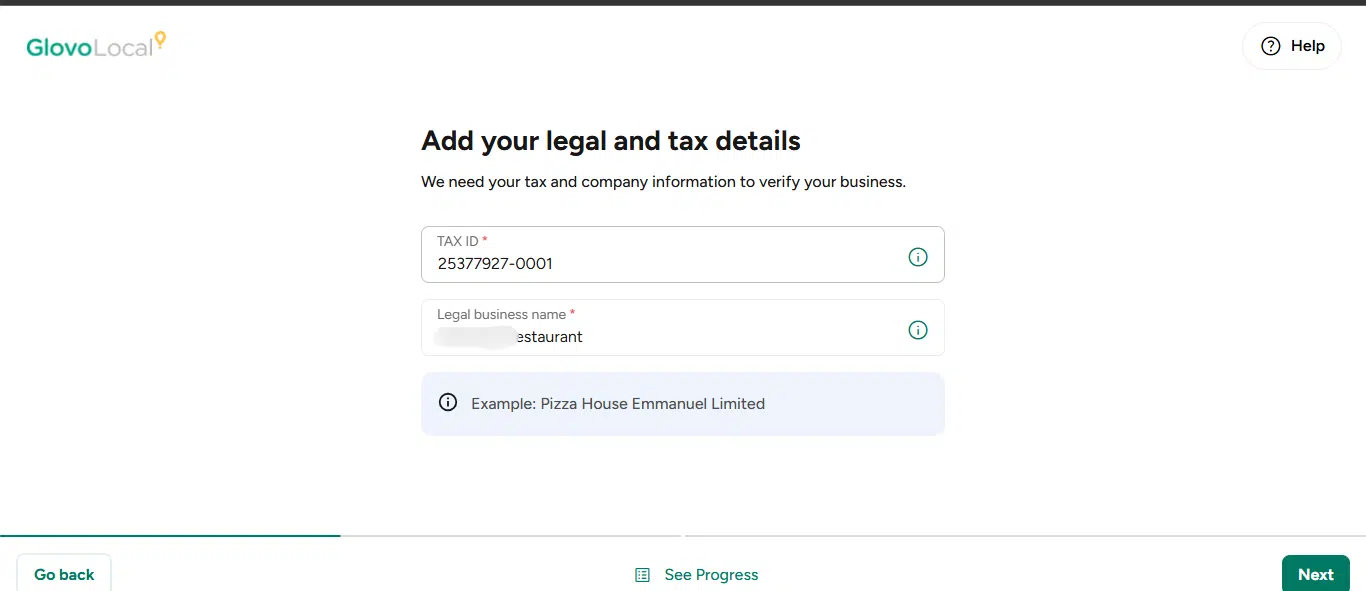

This approach allowed a merchant to move from signup to approval on Chowdeck after submitting basic business details, including a manually generated tax ID, without upfront validation.

2. Weak checks on business identity and ownership details

Marketplace onboarding often accepts business and banking details without fully confirming ownership or legitimacy.

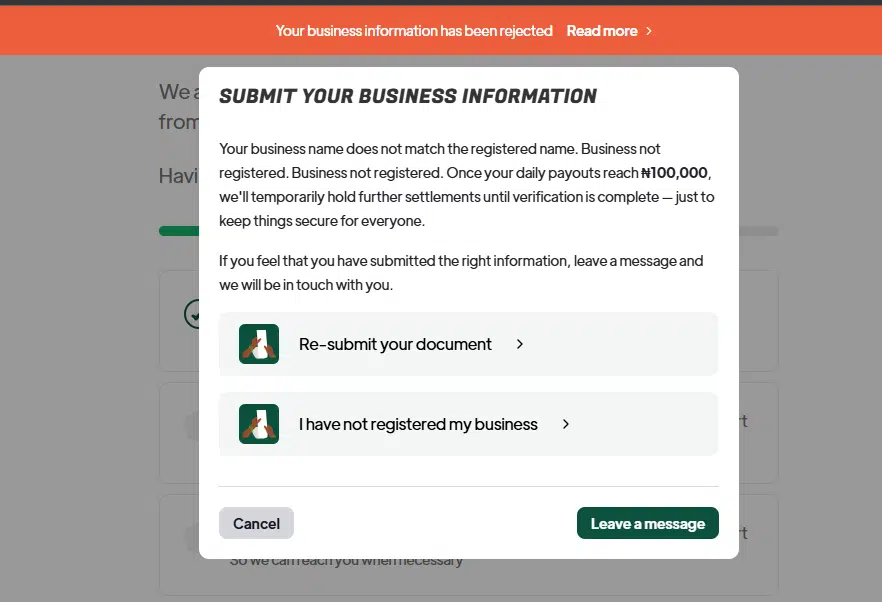

On Glovo, supporting documents were submitted along with a fake CAC registration document and RC number, but they were not properly validated before approval, allowing a fake merchant identity to pass through.

3. Limited validation of registration and tax information

Many platforms rely on submitted registration or tax details without consistently verifying them against official databases.

During the investigation, a fake TIN and business registration details were accepted during onboarding, showing how weak cross-checking can let unverified businesses move forward without detection.

4. Document checks treated as a formality step

Even when documents are requested, they are often only reviewed at a surface level.

In the Glovo case, submitted business documents were accepted during onboarding despite inconsistencies, showing that document review can become procedural rather than a strong verification step.

5. Restricted access still allows early activity

Some platforms allow merchants to operate under limited or restricted access while verification is still pending.

On Chowdeck, even when a mismatch in business details was flagged, the merchant was still allowed to continue under restricted access and begin receiving orders before full verification was completed.

Each of these gaps points to the same underlying problem: verification is being treated as a formality rather than a condition for approval.

What Happens When Merchant Verification Is Weak

Without proper checks before merchants go live, fake vendors can create trust problems and customer complaints that are much harder to manage later.

- Fake stores and ghost listings can appear on marketplaces

When platforms do not properly verify business registration details, fake merchants can create listings using stolen business identities, copied product images, or unavailable products. This was reflected in the Glovo and Chowdeck cases, where impersonated restaurant profiles were able to appear as legitimate stores on the platforms.

2. Refund abuse and fake order activity become easier

Weak onboarding checks make it easier for fake merchants to manipulate orders, disputes, and refunds. Once an unverified seller is allowed onto a platform, it becomes harder to tell whether fulfilment issues are genuine mistakes or coordinated abuse.

3. Fraudsters can reuse identities to return to platforms

Without strong owner verification and account validation, fraudsters can repeatedly create new merchant accounts using slightly modified business details, recycled documents, or different phone numbers. This allows the same bad actors to keep re-entering platforms even after previous accounts are removed.

4. Platforms struggle to confirm who is actually behind a business

Creating a seller account is not the same as verifying a real business owner. Proper merchant verification should include checks like CAC verification, TIN validation, account ownership checks, and confirming who controls the business before approval is completed.

5. Customer trust starts to break down over time

Most customers assume stores listed on a marketplace have already been properly vetted. When fake merchants slip through, complaints, failed deliveries, payment disputes, and impersonation issues can slowly damage trust in the platform itself, not just the individual seller.

The earlier platforms can identify risky or unverifiable merchants, the easier it becomes to prevent trust issues before they affect customers and legitimate businesses on the platform.

Compliance vs Trust: Why Proper KYB Matters for Merchant Onboarding

Unlike fintech and banking platforms, marketplace businesses like food delivery apps, logistics platforms, and e-commerce marketplaces are not as tightly regulated when it comes to merchant onboarding. In the financial sector, regulators like the Central Bank of Nigeria enforce strict KYC and KYB requirements because of the risks tied to money movement and financial crime.

For marketplaces and vendor-based platforms, the picture is less defined. Agencies like the Federal Competition and Consumer Protection Commission and the National Agency for Food and Drug Administration and Control have roles around consumer protection and food safety, but there is still no clear, unified framework that focuses specifically on verifying merchants before they go live on platforms.

So if regulation isn't forcing the issue, why does it still matter?

The answer comes down to trust.

Trust is what makes users feel safe ordering from a new restaurant, buying from an unknown seller, or booking a service through a platform. Most customers do not think about onboarding processes; they simply assume the platform has already done the work. When fake merchants slip through, that assumption is broken. And once trust erodes, it is very difficult to rebuild.

This is also a commercial risk, not just a reputational one. Chargebacks, dispute resolution costs, customer churn, and brand damage all carry real financial weight. Platforms that invest in proper verification early avoid a much more expensive problem later.

Building a Strong Verification Flow for Merchant Onboarding

Building a stronger verification flow for merchant onboarding simply means putting the right checks in place before merchants are allowed to start selling products or services.

Here are a few steps your platform can take:

- Verify business and owner details properly

Collecting business details is not enough if they are not verified against trusted records. Marketplace platforms should confirm CAC registration details, tax information, and also verify the identity of the business owner or director before merchants are approved to operate publicly.

2. Validate account ownership before payouts begin

Many fake merchant problems start when platforms cannot confidently link payout accounts to verified businesses. Account ownership checks help marketplaces confirm that the person receiving payments is genuinely connected to the business being onboarded.

3. Use onboarding flows based on risk levels

Not every merchant carries the same level of risk. A large restaurant chain, online electronics seller, logistics partner, or newly created vendor account may require different levels of verification before approval.

Risk-based onboarding helps platforms apply stronger checks where necessary without making onboarding difficult for every merchant.

4. Combine automated checks with manual review where necessary

Automated KYB and identity verification checks can help marketplaces review merchants faster and more consistently. But for high-risk cases or suspicious activity, additional manual review steps are still important before merchants go live.

5. Work with verification platforms built for merchant onboarding

Many marketplaces are not built to handle deep verification internally. Identity and merchant verification platforms can help automate checks like CAC verification, account validation, owner identity verification, and onboarding risk screening without turning the process into a long manual review.

Identity verification platforms like Dojah help marketplaces verify merchants properly before they go live, reducing the chances of fake businesses slipping through onboarding unnoticed.

How Dojah Helps Platforms Verify Merchants Before They Go Live

At the centre of everything discussed in this article is one simple expectation: users want to trust the platforms they use. Whether it is ordering food, buying from an online store, or booking a service, that trust depends on knowing that the businesses behind those listings have been properly checked before they go live.

CheckIn by Dojah helps platforms do this during merchant onboarding by making verification simple, structured, and reliable. It supports key checks such as:

- Business verification (CAC lookup): Helps platforms confirm that a business is properly registered and matches official records before it goes live.

- Account ownership validation: Ensures the bank account linked to a merchant actually belongs to the business being onboarded.

- Director and identity checks: Helps confirm the real individuals behind a business to reduce impersonation and fake merchant setups.

- Onboarding risk visibility: Flags potentially risky or inconsistent merchant information early, before they start transacting on the platform.

For marketplaces, this means fewer unknown merchants slipping through onboarding and a stronger foundation of trust between platforms, sellers, and customers.

Marketplace trust is built long before the first transaction happens. It starts with who gets approved in the first place.

Start using Dojah for all your business needs