Go back to Blog

Jennifer Edidiong

Marketing

7 min read

Share to

Mule Account Fraud: How Fintechs Can Detect Money Mule Networks

A business signs up on your platform and passes onboarding without issues. Transactions start small and steady, nothing that raises concern. Over time, the account blends in with thousands of others operating normally.

Weeks later, activity shifts. Funds begin moving faster, across multiple accounts, sometimes in small amounts, sometimes out of the country. Each transaction looks harmless on its own, but together they form a pattern that’s easy to miss until the risk has already spread.

This is how money mule networks often operate inside fintech platforms. By using legitimate-looking accounts to move illicit funds, they exploit gaps after onboarding. Globally, 42 percent of first-party current account fraud is tied to the shadowy world of money mule networks.

This article breaks down what mule account fraud looks like in practice, the warning signs to watch for, and how to prevent mule networks before they scale across your platform.

What Money Mule Networks Look Like in African Fintechs

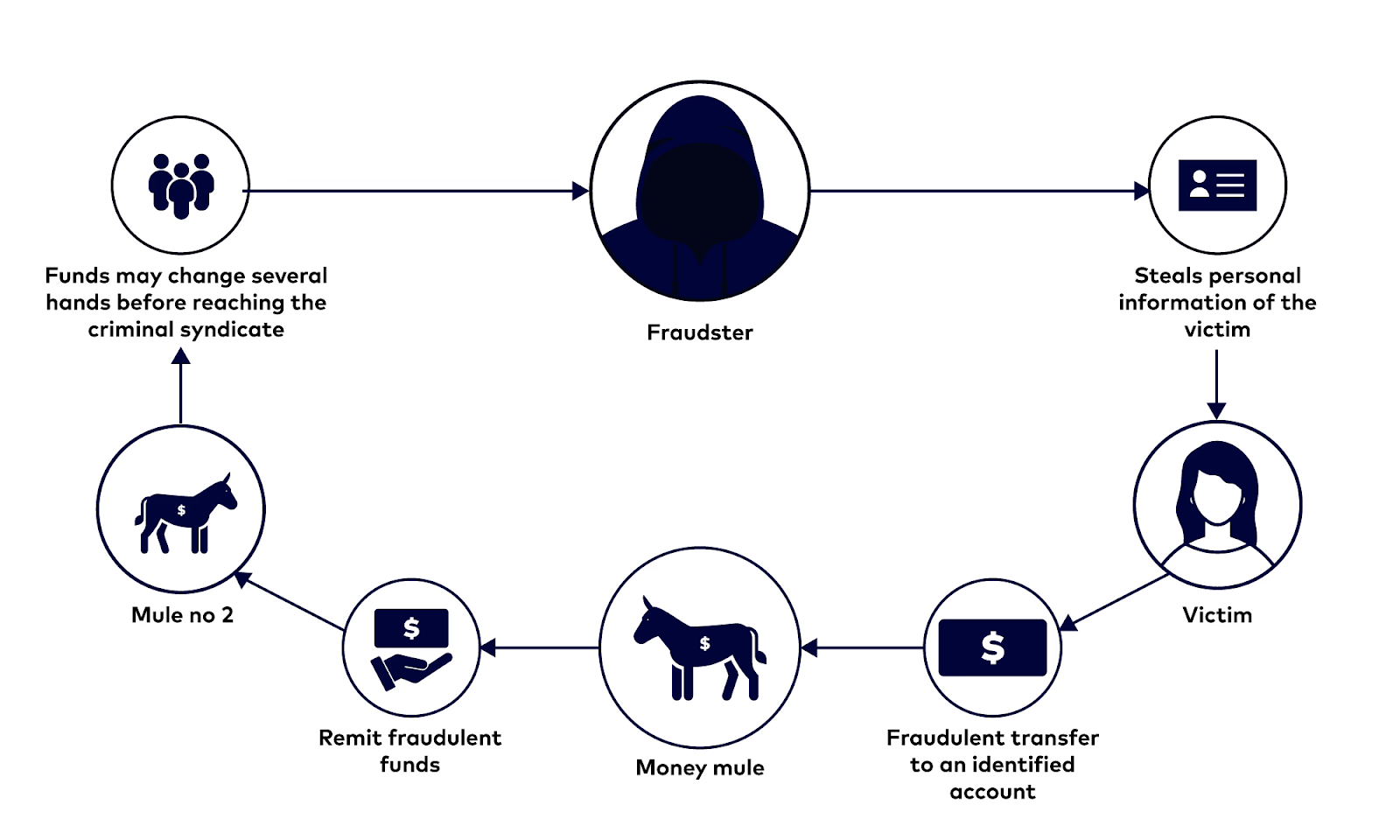

Money mule networks are organized groups that exploit seemingly legitimate accounts to move stolen funds, launder money, or bypass regulations. For fintechs and banking partners in Africa, these networks pose a growing risk because they leverage multiple accounts and transaction types to hide illicit activity.

Here are practical scenario-based examples of how mule account fraud works:

- Rapid micro-transactions (Smurfing):

A seemingly normal customer account in Lagos suddenly receives multiple small deposits throughout the day, each under regulatory reporting thresholds, then quickly withdraws them across multiple accounts. This layering of small amounts to avoid detection is a classic smurfing tactic. - Cross-border fund movement:

In Nairobi, a new account begins sending small but frequent transfers to accounts in neighboring countries of Uganda and Rwanda. While each transaction seems legitimate, collectively they form a pattern to move money quickly and obscure its origin. - Dormant accounts activated for coordinated activity:

A previously inactive account in Abuja suddenly receives deposits of ₦500,000 from several unrelated users, then transfers the funds in rapid succession to other local accounts. This is often part of a larger mule network, where dormant accounts are reused to mask the true source of stolen funds. - Device and identity reuse across accounts:

Fraudsters use one smartphone or ID to control multiple accounts in a Kenyan fintech. Transactions may appear normal individually, but monitoring shows identical patterns across accounts, revealing a coordinated mule network.

Mule account fraud is hardly ever a one-person job; it is an organised group activity, usually combining smurfing, dormant account fraud, and account takeover fraud to carry out large-scale money laundering across multiple accounts within a given period.

Download the Dojah Fraud Insight Report to see emerging fraud trends across Africa

Common Fintech Fraud Types Compared

Fraud Type | What It Involves | Typical Pattern | Where Risk Shows Up |

| Money Mule Account Fraud | Legitimate accounts used to move illicit funds | Rapid fund movement, coordinated transfers, device or identity reuse | Post-onboarding, transaction flows |

| Account Takeover Fraud | Fraudster gains control of a real user account | New device login, sudden behavior change, fast withdrawals | Post-onboarding, user activity |

| Synthetic Identity Fraud | Fake identities built from real and fabricated data | Inconsistent data and delayed fraud behavior | Onboarding and credit exposure |

Practical scenario of a mule network

Common Red Flags of Mule Account Fraud

Money mule account fraud can be detected when you know the warning signs and suspicious patterns to monitor on your platform. Here are the most common red flags to watch out for:

- Multiple accounts linked to the same device or identity:

If you notice that several accounts share the same phone, IP, or ID details, this could indicate a coordinated mule network. Fraudsters often control multiple accounts from a single device to move funds undetected. Early detection of these links helps prevent layering and rapid fund movement. - Unusual transaction patterns inconsistent with historical behavior:

When an account suddenly starts sending or receiving funds in ways that don’t match its usual activity, this is a warning sign. For instance, if a typically inactive account begins high-volume transfers, you need to investigate further. These anomalies often signal attempts to launder money or bypass regulatory checks. - Rapid deposits and withdrawals across accounts:

Accounts that receive multiple deposits and immediately transfer them elsewhere may be part of smurfing or layering schemes. If you see this happening across several accounts, it’s a pattern consistent with mule networks. Promptly flagging these transactions helps limit exposure to fraud. - Frequent cross-border or unusual payment destinations:

An account sending repeated payments to countries or locations not consistent with the user’s profile is a red flag. For example, a Lagos-based account transferring funds regularly to high-risk regions like Somalia or South Sudan warrants review. Cross-border activity can indicate attempts to obscure the origin or destination of illicit funds. - Coordinated activity across multiple accounts:

When several accounts act in concert, it signals organized fraud. For example, one user transfers funds at 7:15 a.m., and another related account sends a similar amount to the same Lagos destination by 7:17 a.m. Even if each account looks legitimate individually, this mirrored activity reveals a mule network.

Knowing the warning signs to watch for is essential, but not enough. To prevent mule account fraud completely, you need to understand the strategies for detecting it before it occurs on your platform.

Strategies to Detect and Prevent Mule Account Fraud Early

Here are practical strategies designed to detect suspicious activity early that your fraud team can implement to stay ahead:

1. Identity & Device Intelligence

Track devices and reused identities across multiple accounts. When the same phone, IP address, or ID appears across several accounts on your platform, it can indicate a coordinated mule network. Device and identity intelligence helps your team flag suspicious clusters early and prevent rapid fund movement before it escalates.

2. Ongoing Transaction Risk Scoring

Assign real-time risk scores to transactions based on behavior, history, and contextual signals. Proactive risk scoring reduces fraud exposure by ensuring suspicious activity is addressed immediately. Tools like Dojah’s Easy Detect support real-time scoring and alerting at scale.

3. Behavioral Monitoring

Monitor user behavior for anomalies that deviate from normal patterns, such as rapid micro-transactions or repeated deposits and withdrawals across accounts. Behavioral monitoring helps surface risks that may look normal in isolation but suspicious when viewed together. In the Dojah Fraud Insight Report, Japhet Gana, Head of Fraud at Yellow Card, shared how his team used behavioral signals to detect and contain a reactivated crypto mule network within an hour, preventing multi-country losses.

4. Continuous Post-Onboarding Monitoring

Integrate identity, device, behavioral, and transaction signals into continuous post-onboarding monitoring. This helps uncover emerging mule activity that one-time or manual checks often miss. Solutions like Dojah’s Profiled Risk bring these signals into a single view, giving your team clearer visibility and faster response.

By implementing these tools together, fraud teams can detect mule activity earlier, move faster than organized fraud networks, and stop money laundering in real time.

Detecting Mule Account Fraud with Dojah

Staying ahead of mule account fraud requires more than reacting after losses occur. As fraud networks become more coordinated and harder to spot, fintechs need visibility into how accounts behave long after onboarding.

Dojah helps you connect identity, behavioral, and transaction signals to detect mule activity early and reduce exposure across your platform. With continuous monitoring built for African fintech realities, your team can spot coordinated fraud patterns faster and respond with confidence.

If coordinated mule activity is getting harder to track as your platform grows, it’s time to upgrade your fraud monitoring systems.

Reach out to our team to have a conversation about how Dojah can help you detect it early.

Start using Dojah for all your business needs