Go back to Blog

Jennifer Edidiong

Marketing

9 min read

Share to

Nigerian KYC Laws and Requirements You Should Know

One major challenge you’re likely to face when operating in Nigeria is protecting your business from digital fraud. According to a NIBSS report, Nigeria lost ₦52.26 billion to fraud in 2024 alone. With fraud this widespread, your digital business is at risk the moment a user signs up.

KYC, or Know Your Customer, means verifying a customer’s identity to help your business prevent fraud, stay compliant, and build trust. In Nigeria, KYC also helps prevent money laundering, terrorism financing, and other forms of financial crime. Non-compliance with KYC rules can lead to penalties, fines, or even a shutdown.

In this article, I’ll guide you through:

- KYC requirements in Nigeria

- How KYC and AML compliance work in 2025

- Common KYC challenges in Nigeria

- How to scale eKYC in Nigeria with real-time, biometric tools like Dojah

KYC Requirements and AML Compliance in Nigeria

KYC and AML processes in Nigeria are primarily governed by the Money Laundering (Prevention and Prohibition) Act, 2022, and regulatory guidelines issued by bodies like the Central Bank of Nigeria (CBN), the Securities and Exchange Commission (SEC), and the Nigerian Financial Intelligence Unit (NFIU).

These laws are designed to strengthen Nigeria’s defenses against financial crimes. It mandates all regulated entities to implement effective customer due diligence measures to identify and prevent financial crimes.

Who Must Comply With Nigeria’s AML Laws?

KYC and AML obligations apply to all regulated entities in Nigeria. This includes:

- Banks and microfinance institutions

- Fintech companies and digital lenders

- Mobile money operators and payment service providers

- Capital market operators (e.g., brokers, fund managers)

- Insurance firms and pension fund administrators

- Law firms, accountants, casinos, and other designated non-financial institutions (DNFIs)

If your business handles financial transactions, you’re required by law to verify your customers' identities and monitor activity to prevent fraud and money laundering.

What Happens If You Don’t Comply?

Failing to meet KYC and AML obligations in Nigeria comes with serious consequences:

- Regulatory sanctions such as license suspension, revocation, or restrictions by the CBN, SEC, or NFIU

- Financial penalties up to hundreds of millions of naira

- Exposure to fraud, money laundering schemes, and reputational risk

Non-compliance can slow down your growth and expose your business to regulatory risks. With tools like Dojah, you can simplify compliance checks and verify your customers in Nigeria faster.

Requirements for KYC in Nigeria and Accepted Documents

KYC requirements in Nigeria may differ depending on the customer type, whether individual or business. But to stay compliant with Nigeria’s AML laws and CBN guidelines, here’s a simple guide to help you collect the right documents during onboarding:

1. Proof of Identity

Customers must present valid government-issued identification. Commonly accepted IDs in Nigeria include:

- National Identity Number (NIN) or National e-ID Card — now widely used for identity verification

- Permanent Voter’s Card (PVC) — often accepted, especially where NIN is unavailable

- International Passport — suitable for foreign nationals and Nigerians abroad

- Driver’s License — accepted as a secondary form of ID

- Bank Verification Number (BVN) — useful for linking customer identities across services

2. Proof of Residential Address

To verify a customer’s address, you can request recent copies of:

- Utility bills, such as electricity or water bills

- Tenancy or lease agreements

- Bank or credit card statements

- An official letter from an employer or community leader

3. Business Verification Documents (for corporate customers)

When onboarding a business or corporate entity, you should collect the following:

- Certificate of Incorporation from the Corporate Affairs Commission (CAC)

- Tax Identification Number (TIN)

- CAC Form CO7 or Form 1.1 listing directors and shareholders

- Proof of business address, such as a utility bill

- Valid ID for company directors or authorized signatories

4. Additional Supporting Information

In some cases, you may also need to request:

- Source of funds or income information

- Purpose of the account or business relationship

- Next-of-kin or emergency contact details

- Visa or passport page for foreign nationals

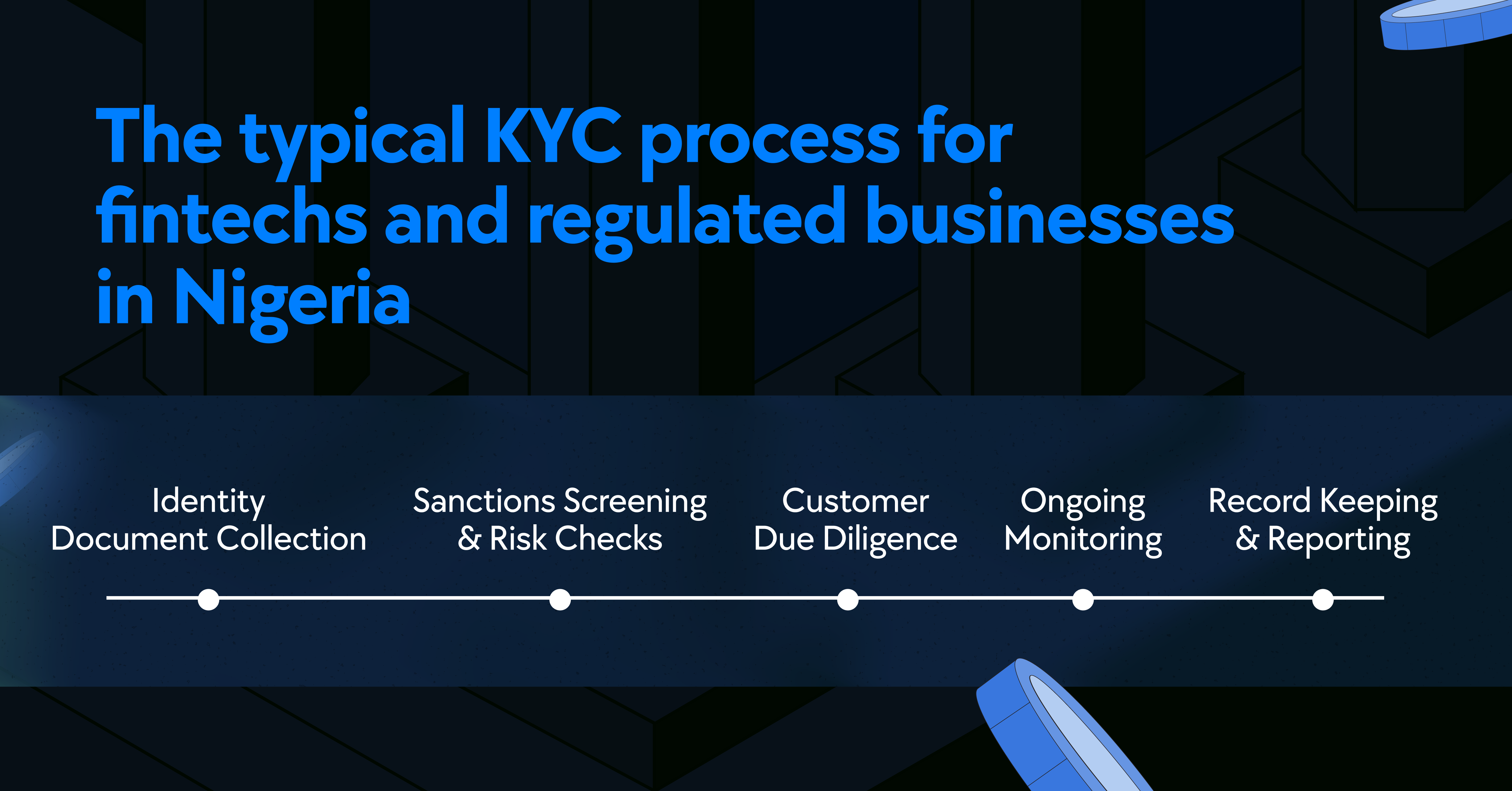

5. Ongoing KYC and Record-Keeping

All documents collected must be verified for authenticity and cross-checked with records from the National Identity Management Commission (NIMC). You should also update customer records regularly to reflect any changes and ensure continuous compliance.

How KYC Works in Nigeria: A Step-by-Step Guide

Here’s what the KYC process typically looks like for businesses operating in Nigeria:

Step 1: Identity Collection

Start by collecting a valid, government-approved ID. This could be the National Identity Number (NIN), Bank Verification Number (BVN), international passport, permanent voter’s card, or driver’s license. You should also collect basic details like full name, date of birth, gender, and address.

Step 2: Identity Verification

Verify the identity documents by matching them against official databases such as NIMC for NIN or NIBSS for BVN. Verification can be done using biometric matching, facial recognition, or document scanning. For remote users, ensure electronic copies are authentic and valid.

Step 3: Data Updates

Update the customer’s KYC profile using verified data pulled from national databases. If there are mismatches in dynamic information like phone number or address, these should be corrected. For mismatches in static information like name or date of birth, the customer should be referred back to the appropriate issuing agency for corrections.

Step 4: Customer Due Diligence (CDD)

Screen the customer against Politically Exposed Persons (PEP) databases, international sanctions lists, and adverse media. You may also need to collect additional information such as employment status, source of funds, or next of kin to complete your risk profiling.

Step 5: Ongoing Monitoring

Once onboarded, monitor the customer’s transactions regularly to detect suspicious or unusual behavior. Periodically review and update customer records, especially when there are changes in risk level or personal data.

Step 6: Special Scenarios

For customers who fail to provide a NIN or BVN, no financial transaction should be allowed beyond basic Tier-1 limits. According to the CBN’s 2024 directive, Tier-1 accounts must now be linked to either NIN or BVN. For foreign nationals, a valid international passport and visa documentation may be used to support identity verification for limited or one-off transactions.

Digital KYC and AML Trends in Nigeria

Nigeria is gradually shifting toward smarter digital KYC processes, backed by updates from the Central Bank. In May 2025, the CBN released a new circular on automated AML standards. This new regulation requires businesses to monitor transactions in real-time and screen users against watchlists like PEP and sanctions databases.

While a fully centralized eKYC system is still in development, many platforms already use tools like biometric verification, facial recognition, and liveness detection to reduce fraud and meet compliance needs. These digital methods are especially popular among fintech, lending platforms, and digital service providers.

The CBN now expects businesses to create risk profiles for each user, track ongoing activity for red flags, and submit suspicious transaction reports to the Nigerian Financial Intelligence Unit (NFIU). These rules apply not just during onboarding but throughout the entire customer lifecycle.

With compliance standards getting stricter, now is the time to explore tools like Dojah that simplify digital KYC and transaction monitoring.

Common KYC Challenges When Expanding into Nigeria

Here are some of the KYC challenges you’re likely to face when entering the Nigerian market:

1. Dealing with Multiple Regulatory Bodies

Nigeria’s KYC regulations are regulated by multiple bodies, including the CBN, EFCC, and NIMC. Each authority operates with its own standards and timelines. This overlap often makes it challenging to keep up with shifting compliance requirements.

2. No Unified National KYC Repository

While systems like the NIN are improving identity access, Nigeria still lacks a centralized KYC database. This means customers may need to upload the same documents across different platforms. It could slow down onboarding and lead to friction.

3. High Risk of Fraud and Forged Documents

Fraudulent IDs, utility bills, and fake biometrics are still common. Many institutions struggle to spot manipulated documents or synthetic identities, especially when verifying users at scale. This increases compliance risk and weakens your onboarding pipeline.

4. Reliance on Manual Verification Processes

A large portion of records, including business registration or address documents, are not digitized. This forces teams to rely on manual checks, which delay onboarding and create room for human error.

5. Weak Tech Infrastructure in Rural Areas

If your product targets users in rural or semi-urban areas, you may face slow internet, poor device access, or low digital literacy. These challenges can limit the success of biometric or video KYC, making onboarding longer and less efficient.

Simplify KYC and Save Time with Dojah

KYC compliance in Nigeria comes with its own set of challenges. From overlapping regulations to manual verification processes, and pressure to onboard users fast without exposing your platform to fraud. Managing all of this manually can slow you down and leave your platform exposed to fraud risks.

This is where Dojah comes in. Dojah helps you meet Nigeria’s KYC requirements without the usual hassle.

With Dojah, you can:

- Instantly verify BVNs, NINs, and phone numbers through reliable integrations with NIBSS and NIMC.

- Reduce fraud risks with biometric verification and AI-powered document checks.

- Automate AML screening and make onboarding faster with developer-friendly APIs.

Our verification tools are built for local needs, easy to integrate, and trusted by over 500 businesses across Nigeria and Africa.

Need to stay compliant while improving onboarding speed? Dojah helps you build fully compliant KYC workflows in minutes.

Frequently Asked Questions About KYC in Nigeria

What is the KYC process in Nigeria?

You need to verify users using their BVN, NIN, or valid ID, perform biometric checks, and screen against AML watchlists.

Can I run KYC checks digitally?

Yes. You can verify BVNs, NINs, and phone numbers in real time using digital tools like Dojah, which integrate with NIBSS and NIMC.

What are the biggest KYC challenges for fintech in Nigeria?

Overlapping regulations, fraud risks, and integration with local databases.

How long does KYC onboarding typically take?

Digital verification takes seconds. Manual reviews or incomplete data can take days.

Do I need local licensing to onboard users in Nigeria?

Yes. You must comply with regulations set by bodies like the CBN, NIBSS, and NIMC.

How can Dojah help with KYC in Nigeria?

Dojah offers instant BVN and NIN verification, AI-powered fraud checks, and easy API integration for fast, secure onboarding.

Start using Dojah for all your business needs