Go back to Blog

Jennifer Edidiong

Marketing

11 min read

Share to

Transaction Monitoring for Banks: A Complete Guide

Managing a bank today goes beyond processing deposits and transfers. Every transaction, whether it’s a card payment, wire transfer, or remittance, is an opportunity to serve customers. But it is also a potential doorway for fraud.

Across Africa, businesses lose an estimated $88 billion every year to fraud, with banks being the hardest hit. From insider schemes to money laundering, the risks are everywhere.

That is why as a bank founder or compliance lead, you must constantly scrutinize every transaction flowing through your institution. Ignoring this can allow fraudulent activity to slip through unnoticed and cause massive financial losses.

This is where a transaction monitoring tool becomes essential. It helps you detect unusual activity early, flag risks quickly, and stay ahead of fraudsters.

In this article, I’ll guide you through everything you need to know about transaction monitoring for banks: how it works, the challenges involved, and how to choose the right solution for your institution.

Why Banks Need Transaction Monitoring

First, let’s go into the essential reasons why transaction monitoring is important for your bank:

1. Regulatory Compliance

Your bank needs to meet AML, KYC, and government regulations. Transaction monitoring keeps every transaction aligned with these rules so you avoid fines or penalties. In practice, this means your compliance team can generate audit-ready reports quickly and prove your bank is following the law.

2. Fraud Prevention

Fraud takes many forms — from account takeovers to money laundering. With transaction monitoring, you can spot unusual patterns early, like repeated high-value transfers or sudden spikes in activity. This gives you a chance to act before fraud causes financial or reputational damage.

3.Operational Efficiency

Manual reviews can slow your team down and create backlogs. Monitoring transactions automatically reduces delays and prioritizes real risks, so your compliance team can respond to potential threats quickly.

4. Building Investor Trust

Investors want to know their money is safe and your bank is well-managed. Using transaction monitoring shows that you take security and compliance seriously. This makes it easier to attract investment and grow your business.

5. Protecting Your Bank’s Reputation

Your customers and partners notice when their money is safe. Transaction monitoring helps prevent fraud and regulatory breaches, keeping your reputation intact and your users confident in your platform.

Transaction Monitoring Use Cases

Practical ways you can use transaction monitoring in your bank:

- Suspicious Deposits/Withdrawals

If a customer suddenly makes large deposits or quick withdrawals outside their usual activity, you can use monitoring to flag it. This lets you review the transaction immediately before it becomes a bigger issue.

- Structuring/Smurfing Detection

Smurfing occurs when fraudsters split large sums into smaller transactions to avoid reporting thresholds. With monitoring in place, you can spot this pattern and flag it before it escalates into money laundering.

- Cross-Border Transactions

If your customers send or receive international transfers, monitoring helps you track unusual foreign activity. This way, you can ensure every transfer meets compliance standards.

- Ongoing Due Diligence for High-Risk Customers

For certain customers flagged as high-risk from the start due to profile or location, monitoring lets you track changes in their behavior over time. This way, your team can act quickly if something suspicious arises.

Related: Processes and tools for transaction monitoring

How Transaction Monitoring Works in Banks

Now that you know how transaction monitoring can be applied in your bank, let’s break down the step-by-step process and how it works in practice:

1. Data Collection

First, every transaction generates data, including the amount, type, customer information, and device details. Monitoring captures this data in real time for analysis. Having complete and accurate data ensures your system can detect suspicious patterns effectively.

2. Real-Time vs Post-Transaction Monitoring

Then, real-time monitoring reviews transactions as they occur, allowing you to flag unusual activity immediately. Post-transaction monitoring reviews transactions in batches, like hourly or daily, helping you spot trends and anomalies over time. Most banks use both to catch risks quickly while maintaining an overall view of activity.

3. Rule-Based Monitoring

Next, rule-based monitoring relies on predefined rules, such as transfers above a certain threshold or activity from high-risk regions. You can customize these rules to match your bank’s risk appetite and regulatory obligations. This ensures common fraud patterns are flagged without slowing down legitimate transactions.

4. Alerts, Risk Scoring & Escalation

Then, when suspicious activity is detected, the system generates an alert and assigns a risk score to prioritize investigation. Your compliance team can act quickly, pausing transactions, requesting verification, or escalating high-risk cases. With this approach, real threats are handled fast without interrupting normal banking activity.

5. Reporting & Documentation

Finally, every flagged transaction is logged and documented for audits and regulatory compliance. Advanced monitoring systems can generate reports automatically, making it easier for your compliance team to stay audit-ready.

See: How to choose a fraud detection software for your bank

Challenges Banks Face with Transaction Monitoring

When you put transaction monitoring into practice for your bank, you’re likely to face a few challenges. Some of them are:

1. High False Positives

Sometimes legitimate transactions get flagged as suspicious, creating a flood of alerts. Sifting through too many false positives slows your team and diverts attention from real risks. Studies show false positives can reach up to 95% of alerts in banking, highlighting a major challenge for compliance teams.

2. Manual Review Fatigue

Even with automated monitoring, your team still needs to review flagged transactions to confirm whether they’re truly risky. When alerts keep increasing, constantly checking each one can become overwhelming if proper support or processes aren’t in place.

3. Evolving Fraud Patterns

Fraudsters constantly change tactics to bypass monitoring systems. If your bank relies on static rules, new methods like layered smurfing or synthetic identities can easily slip through. This means that without updated systems, keeping up with emerging fraud becomes a challenge.

4. Legacy System Limitations

Older banking systems often struggle to integrate with modern monitoring tools. This can slow down data processing and make alerts less accurate. Without flexible systems, your bank may not fully leverage real-time monitoring or AI-driven detection

5. Data Integration & Visibility

Monitoring works best when you have a complete view of all transactions and customer behavior. If your systems are disconnected or data is incomplete, spotting anomalies becomes harder. With a lack of integration across payments, KYC checks, and internal systems, your team may miss suspicious activity.

How to Choose the Right Transaction Monitoring Solution

Knowing these challenges, it’s important to check certain factors when choosing a transaction monitoring tool for your bank. Here’s what to look for:

1. Accuracy & Real-Time Detection

Your monitoring tool should provide precise, real-time data for every transaction. This ensures suspicious activity is flagged immediately, so you don’t waste time investigating harmless transactions. Accurate alerts also help your team respond quickly to real threats before they escalate.

2. Flexibility

Fraud tactics evolve constantly, and your transaction monitoring system should evolve too. Choose a tool with customizable rules so you can adjust thresholds, workflows, and alerts as your bank’s risk profile changes. This way, you can adapt quickly when new tactics emerge or regulatory requirements change.

3. Scalability

As your bank grows, transaction volumes can spike, and a system that can’t keep up creates bottlenecks. Choose a solution that processes large volumes smoothly, so no transaction goes unchecked. This ensures your compliance team can maintain accuracy and respond quickly, even during high-traffic periods.

4. Coverage

If your bank operates in multiple regions, your tool should cover all relevant markets and regulations. This ensures cross-border transfers are tracked and flagged according to local rules. Comprehensive coverage prevents gaps that could leave your bank exposed to risk or penalties.

5. Technical Support

When issues arise, your team needs timely guidance to resolve them without disrupting operations. A solution with strong support provides expert assistance, training, and troubleshooting resources. This ensures your transaction monitoring system stays effective and your team confident in handling alerts.

Also see: How to choose a transaction monitoring tool for your fintech

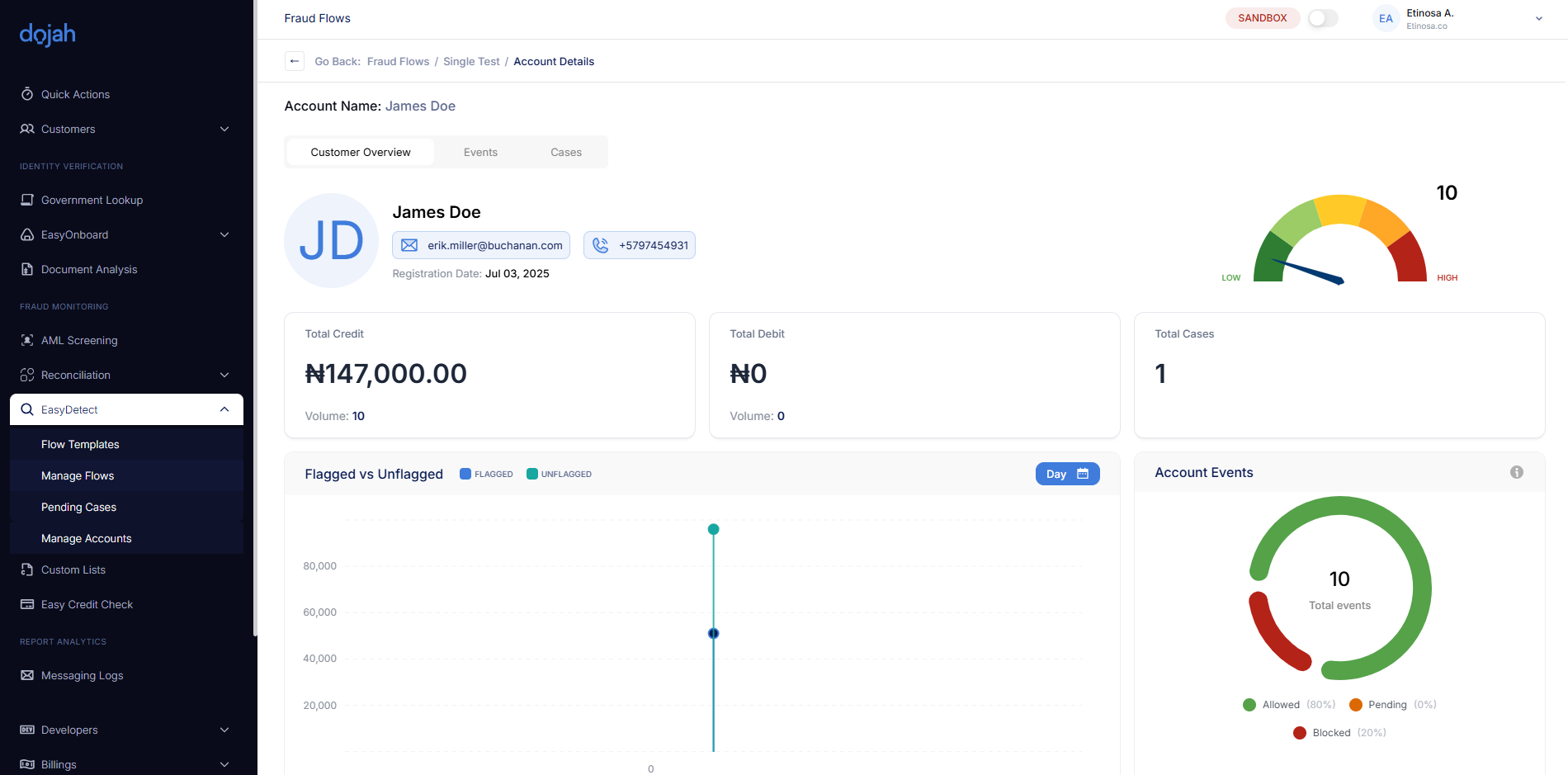

Dojah’s Transaction Monitoring Solution

The points above highlight what to look for in a monitoring tool. Dojah’s EasyDetect brings them all together in a unified fraud prevention solution built for banks. With it, you get:

1. Accuracy You Can Trust

Banks handle thousands of transactions daily, and accuracy isn’t negotiable. EasyDetect delivers 99.9% data and verification accuracy, ensuring alerts are based on clean, reliable data, not guesswork. This means your compliance team can spend less time chasing false alarms and more time tackling real risks.

2. Real-Time Detection

Delays in fraud detection can cost your bank millions. EasyDetect works in real time, flagging suspicious activity as transactions happen. With immediate results, your team can act quickly before risks turn into financial or reputational damage.

3. Flexible Rule Management

No two banks face the exact same risks. EasyDetect allows you to create and adjust monitoring rules to fit your institution’s needs: whether it’s tracking high-value transfers, repeated suspicious activity, or region-specific red flags. You get full control without overhauling existing systems.

4. Pre-Built Flow Templates

Compliance teams don’t always have time to start from scratch. EasyDetect comes with pre-built templates for common monitoring scenarios, helping your team start strong from day one. These templates make fraud detection easier to set up and more efficient to manage.

5. Seamless Integration with KYC Tools

Effective monitoring goes hand in hand with identity verification. EasyDetect integrates directly with Dojah’s KYC tools, giving you a 360° view of customers and their behavior. This unified approach strengthens fraud detection and compliance efforts across your bank.

6. Smarter Reporting

Regulators demand precision, and reporting errors can be costly. EasyDetect helps you prepare mandatory reports such as Suspicious Transaction Reports (STRs), with less effort and more accuracy. That means faster audits, fewer compliance headaches, and stronger trust with regulators.

Prevent Fraud and Stay Ahead with Dojah

For banks, transaction monitoring isn’t optional; it’s essential for protecting customers, revenue, and compliance. Choosing the wrong tool can leave gaps that expose you to fraud and costly setbacks. With the right system, you can spot unusual activity early, reduce risks, and stay ahead of regulators.

That’s where Dojah comes in.

EasyDetect combines real-time monitoring, automated alerts, and advanced risk detection in a way that fits the realities of modern banking.

It’s built to help compliance teams work smarter, reduce fraud, and keep your bank resilient as transaction volumes grow.

👉 Book a demo today to see how Dojah protects your bank.

Frequently Asked Questions on Transaction Monitoring for Banks

1. Why do I need transaction monitoring for my bank?

Transaction monitoring helps your bank detect suspicious activity, prevent fraud, and stay compliant with regulatory requirements. Without it, you risk financial loss, reputational damage, and regulatory penalties.

2. How does transaction monitoring help my bank?

It gives your compliance team real-time visibility into customer transactions, so you can flag unusual patterns before they escalate into serious risks. This keeps your customers and institution safe.

3. What challenges would my bank face with transaction monitoring?

Common challenges include high false positives, manual review fatigue, evolving fraud tactics, and poor system integration. Addressing these early ensures your monitoring system runs smoothly.

4. How do I choose the right monitoring tool for my bank?

Look for a solution that offers real-time accuracy, flexible rule management, scalability, broad coverage, and reliable technical support. These factors make the difference between effective monitoring and wasted effort.

5. How does Dojah’s EasyDetect help banks with transaction monitoring?

EasyDetect delivers real-time monitoring, automated alerts, and advanced risk detection tailored for banking. It helps compliance teams focus on real threats while reducing false alarms.

6. How long does real-time transaction monitoring take to detect risks?

With EasyDetect, suspicious activity is flagged instantly as transactions occur. This gives your team immediate insight and enough time to act before risks become costly problems.

Start using Dojah for all your business needs